Actuarial Report (19th) on the Pension Plan for the Public Service of Canada as at 31 March 2020

Accessibility statement

The Web Content Accessibility Guidelines (WCAG) defines requirements for designers and developers to improve accessibility for people with disabilities. It defines three levels of conformance: Level A, Level AA, and Level AAA. This report is partially conformant with WCAG 2.0 level AA. If you require a compliant version, please contact webmaster@osfi-bsif.gc.ca.

The Honourable Jean-Yves Duclos, P.C., M.P.

President of the Treasury Board

Ottawa, Canada

K1A 0R5

Dear Minister:

Pursuant to Section 6 of the Public Pensions Reporting Act, I am pleased to submit the report on the actuarial review as at 31 March 2020 of the pension plan for the Public Service of Canada. This actuarial review is in respect of pension benefits and contributions which are defined by Parts I, III and IV of the Public Service Superannuation Act, the Special Retirement Arrangements Act and the Pension Benefits Division Act.

Yours sincerely,

Assia Billig, FCIA, FSA, PhD

Chief Actuary

Table of contents

Tables

- Table 1 - Main Results as at 31 March 2020

- Table 2 - PSSA Current Service Cost on a Calendar Year Basis

- Table 3 - PSSA Current Service Cost on a Calendar Year Basis - Group 1

- Table 4 - PSSA Current Service Cost on a Calendar Year Basis - Group 2

- Table 5 - Member Contribution Rates

- Table 6 - RCA No. 1 Current Service Cost on a Calendar Year Basis

- Table 7 - Ultimate Best-Estimate Economic Assumptions

- Table 8 - Demographic Assumptions

- Table 9 - State of the Superannuation Account

- Table 10 - Balance Sheet - Pension Fund

- Table 11 - Reconciliation of PSSA Financial Position

- Table 12 - Experience Gains and (Losses)

- Table 13 - Gains and (Losses) due to Revision of Actuarial Assumptions

- Table 14 - Current Service Cost for Plan Year 2022

- Table 15 - Reconciliation of PSSA Current Service Cost

- Table 16 - Projection of Current Service Cost on a Plan Year Basis

- Table 17 - Pension Fund Administrative Expenses

- Table 18 - Estimated Contributions for Prior Service BuyBack

- Table 19 - Sensitivity of Valuation Results to Variations in Mortality Improvement Rates

- Table 20 - Sensitivity of Valuation Results to Variations in Key Economic Assumptions

- Table 21 - State of the RCA No. 1 Account

- Table 22 - State of the RCA No. 2 Account

- Table 23 - RCA No. 1 - Current Service Cost

- Table 24 - Estimated Government Credits

- Table 25 - Estimated Government Cost - Pension Fund

- Table 26 - Member Contribution Rates

- Table 27 - Reconciliation of Balances in Superannuation Account

- Table 28 - Reconciliation of Balances in Pension Fund

- Table 29 - Reconciliation of Balances in RCA No. 1 Account

- Table 30 - Reconciliation of Balances in RCA No. 2 Account

- Table 31 - Rates of Interest (Return)

- Table 32 - Summary of Membership Data

- Table 33 - Reconciliation of Group 1 Contributors

- Table 34 - Reconciliation of Group 2 Contributors

- Table 35 - Reconciliation of Pensioners

- Table 36 - Reconciliation of Surviving Spouses

- Table 37 - Reconciliation of Children Survivors

- Table 38 - Reconciliation of Pensioners with ERI Benefits

- Table 39 - Actuarial Value of Pension Fund Assets

- Table 40 - Asset Mix

- Table 41 - Real Rate of Return by Asset Type

- Table 42 - Overall Rate of Return on Assets of the Pension Fund

- Table 43 - Rates of Return on Assets in Respect of the Pension Fund

- Table 44 - Transfer Value Real Interest Rates

- Table 45 - Economic Assumptions

- Table 46 - Sample of Assumed Seniority and Promotional Salary Increases

- Table 47 - Assumed Annual Increases in Number of Contributors

- Table 48 - Sample of Assumed Rates of Retirement - Main Group 1 - Male

- Table 49 - Sample of Assumed Rates of Retirement - Main Group 1 - Female

- Table 50 - Sample of Assumed Rates of Retirement - Main Group 2 - Male

- Table 51 - Sample of Assumed Rates of Retirement - Main Group 2 - Female

- Table 52 - Sample of Assumed Rates of Retirement - Operational Service

- Table 53 - Sample of Assumed Rates of Pensionable Disability

- Table 54 - Sample of Assumed Rates of Withdrawal - Main Group - Male

- Table 55 - Sample of Assumed Rates of Withdrawal - Main Group - Female

- Table 56 - Sample of Assumed Rates of Withdrawal - Operational Group

- Table 57 - Sample of Proportions Opting for a Deferred Annuity - Main Group - Male

- Table 58 - Sample of Proportions Opting for a Deferred Annuity - Main Group - Female

- Table 59 - Sample of Proportions Opting for a Deferred Annuity - Operational Service Group

- Table 60 - Sample of Assumed Rates of Mortality Weighted by Salary

- Table 61 - Sample of Assumed Mortality Improvement Rates

- Table 62 - Cohort Life Expectancy of Contributors and Retirement Pensioners

- Table 63 - Sensitivity of Life Expectancy to Variations in Mortality Improvement Rates

- Table 64 - Assumptions for Survivor Spouse Allowances

- Table 65 - Sample of Assumed Proportion Eligible Spouse at Termination of Member

- Table 66 - Sample of Assumed Divorce Rates

- Table 67 - Financial Positions at Tail-Events of Best-Estimate Portfolio as at 31 March 2023

- Table 68 - Male Contributors (Main Group)

- Table 69 - Main Male - Summary

- Table 70 - Female Contributors (Main Group)

- Table 71 - Main Female - Summary

- Table 72 - Male Contributors (Operational Group)

- Table 73 - CSC Male - Summary

- Table 74 - Female Contributors (Operational Group)

- Table 75 - CSC Female - Summary

- Table 76 - Contributors on Leave Without Pay and Non-active Contributors

- Table 77 - LWOP - Summary

- Table 78 - Male Retired Pensioners

- Table 79 - Pensioner Male - Summary

- Table 80 - Female Retired Pensioners

- Table 81 - Pensioner Female - Summary

- Table 82 - Male Disabled Pensioners

- Table 83 - Male Disabled Pensioner- Summary

- Table 84 - Female Disabled Pensioners

- Table 85 - Female Disabled Pensioner - Summary

- Table 86 - Surviving Spouses

- Table 87 - Survivor - Summary

Charts

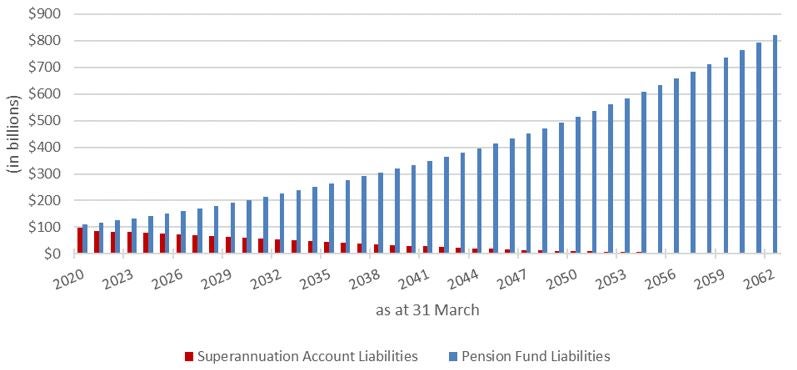

- Chart 1 - Evolution of Liabilities of Superannuation Account and Pension Fund over Time

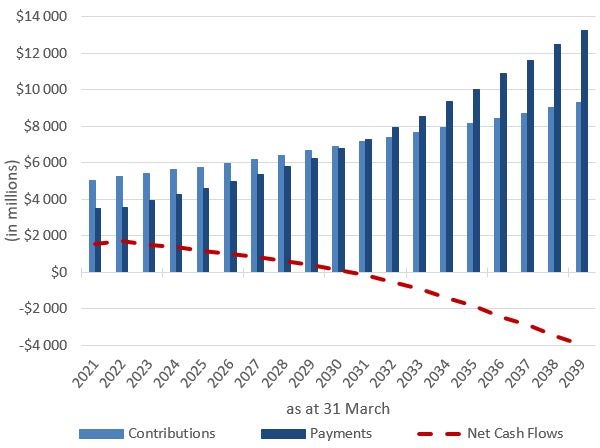

- Chart 2 - Evolution of Cash Flows over Time

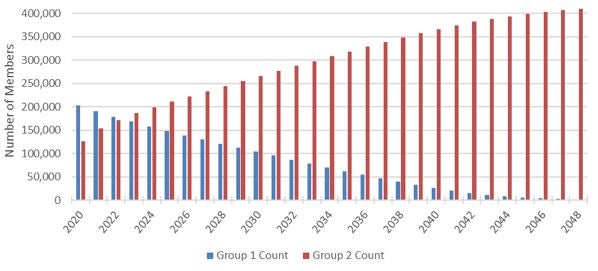

- Chart 3 - Evolution of Group 1 and Group 2 Active Membership

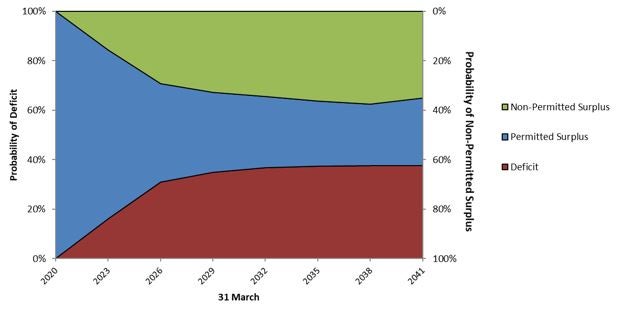

- Chart 4 - Range of Potential Funding Ratio for the Best-Estimate Portfolio - PS Pension Fund

- Chart 5 - Likelihood of Deficit, Permitted and Non-Permitted Surplus due to Investment Experience

1. Executive Summary

This actuarial report on the pension plan for the Public Service of Canada (PSPP) was made pursuant to the Public Pensions Reporting Act (PPRA).

This actuarial valuation is as at 31 March 2020 and is in respect of pension benefits and contributions defined by Parts I, III and IV of the Public Service Superannuation Act (PSSA), the Special Retirement Arrangements Act (SRAA), which covers the Retirement Compensation Arrangements Regulations No. 1 and No. 2 (RCA), and the Pension Benefits Division Act (PBDA).

The previous actuarial report was prepared as at 31 March 2017. The next periodic review is scheduled to occur no later than 31 March 2023.

1.1 Purpose of Actuarial Report

The purposes of this actuarial valuation are to determine the state of the Public Service Superannuation Account (Superannuation Account), the Public Service Pension Fund (Pension Fund) and the RCA Accounts, to determine the projected current service costs for the Pension Fund and the RCA Accounts as well as to assist the President of the Treasury Board in making informed decisions regarding the financing of the government’s pension benefit obligations. This report may not be suitable for another purpose.

1.2 Main Findings

| Superannuation Account |

Pension Fund |

RCA No. 1 Account |

RCA No. 2 Account |

|

|---|---|---|---|---|

| Financial Position | ||||

| Recorded Balance/Actuarial Value of Assets | 91,537 | 125,409 | 2,615 | 1,272 |

| Actuarial Liability | 98,837 | 110,909 | 2,192 | 1,142 |

| Actuarial Excess(Shortfall)/Surplus(Deficit) | (7,300) | 14,500 | 423 | 130 |

| Current Service Costs for Calendar Year 2022 | ||||

| Member Contributions | - | 2,754 | 6.6 | - |

| Government Current Service Cost | - | 2,783 | 39.0 | - |

| Total Current Service Cost/Credit | - | 5,537 | 45.6 | - |

| Special Credits/Payments in Plan Year 2022 | 7,805 | - | - | - |

Table 1 Footnote

|

||||

The proposed amounts to be credited to (or debited from) the Accounts and the Pension Fund are shown on a calendar year basis in this section, beginning with calendar year 2022, which is the first calendar year that follows the expected tabling of this report. Valuation results on a plan yearFootnote 1 basis are shown in Section II.

1.2.1 Superannuation Account (Service prior to 1 April 2000) as at 31 March 2020

- The balance of the Superannuation Account is $91,537 million;

- the actuarial liability for service prior to 1 April 2000Footnote 2 is $98,837 million;

- the resulting actuarial shortfall is $7,300 million;

- it is expected that the government will make a one-time credit of $7,805 million as at 31 March 2022 to eliminate the actuarial shortfall.

The time, manner and amount of such credits are to be determined by the President of the Treasury Board.

1.2.2 Pension Fund (Service since 1 April 2000)

1.2.2.1 Financial Position as at 31 March 2020

- The actuarial value of the assets in respect of the Pension Fund is $125,409 million;

- the actuarial liability is $110,909 million;

- the resulting actuarial surplus is $14,500 million;

- the funding ratio is 113.1%.

1.2.2.2 Current Service CostFootnote 3

Table 2 shows the projected current service cost expressed in millions of dollars and as a percentage of the expected pensionable payrollFootnote 4 for the three calendar years following the expected tabling of this report. The ratio of government current service cost to contributor current service cost is also shown. Tables 3 and 4 show the same results for Group 1Footnote 5 and Group 2Footnote 6, respectively.

Projected current service costs shown in these tables are based on the memberFootnote 7 contribution rates presented in Table 5.

| Calendar Year | Current Service Cost ($ millions) |

Current Service Cost (% of pensionable payroll) |

Ratio of Government to Contributor Current Service Cost |

||||

|---|---|---|---|---|---|---|---|

| Contributors | Government | Total | Contributors | Government | Total | ||

| 2022 | 2,754 | 2,783 | 5,537 | 9.74% | 9.84% | 19.58% | 1.01 |

| 2023 | 2,850 | 2,880 | 5,730 | 9.68% | 9.79% | 19.47% | 1.01 |

| 2024 | 2,945 | 2,977 | 5,921 | 9.64% | 9.74% | 19.38% | 1.01 |

| Calendar Year | Current Service Cost ($ millions) |

Current Service Cost (% of pensionable payroll) |

Ratio of Government to Contributor Current Service Cost |

||||

|---|---|---|---|---|---|---|---|

| Contributors | Government | Total | Contributors | Government | Total | ||

| 2022 | 1,717 | 1,746 | 3,463 | 10.47% | 10.64% | 21.11% | 1.02 |

| 2023 | 1,675 | 1,705 | 3,380 | 10.47% | 10.65% | 21.12% | 1.02 |

| 2024 | 1,632 | 1,664 | 3,296 | 10.46% | 10.66% | 21.12% | 1.02 |

| Calendar Year | Current Service Cost ($ millions) |

Current Service Cost (% of pensionable payroll) |

Ratio of Government to Contributor Current Service Cost |

||||

|---|---|---|---|---|---|---|---|

| Contributors | Government | Total | Contributors | Government | Total | ||

| 2022 | 1,037 | 1,037 | 2,074 | 8.73% | 8.73% | 17.46% | 1.00 |

| 2023 | 1,175 | 1,175 | 2,350 | 8.75% | 8.75% | 17.50% | 1.00 |

| 2024 | 1,313 | 1,313 | 2,626 | 8.78% | 8.78% | 17.56% | 1.00 |

1.2.2.3 Member Contribution Rates

The current service cost is borne jointly by the plan members and the government. Group 1 and Group 2 member contribution rates are determined such that the government share of the current service cost contribution is 50%. Table 5 shows the member contribution rates for the three calendar years following the expected tabling of this report.

| Calendar year | Group 1 | Group 2 | ||

|---|---|---|---|---|

| Below YMPE | Above YMPE | Below YMPE | Above YMPE | |

| 2022 | 9.36% | 12.48% | 7.95% | 11.82% |

| 2023 | 9.35% | 12.37% | 7.93% | 11.72% |

| 2024 | 9.35% | 12.25% | 7.94% | 11.54% |

1.2.3 RCA No. 1 Account as at 31 March 2020

- The balance of the RCA No. 1 Account is $2,615 million;

- the actuarial liability is $2,192 million;

- the resulting actuarial excess is $423 million.

Table 6 shows the projected current service cost in millions of dollars and as a percentage of the expected pensionable payroll for the three calendar years following the expected tabling of this report. The ratio of government current service cost to contributor current service cost is also shown.

| Calendar Year | Current Service Cost ($ millions) |

Current Service Cost (% of pensionable payroll) |

Ratio of Government to Contributor Current Service Cost |

||||

|---|---|---|---|---|---|---|---|

| Contributors | Government | Total | Contributors | Government | Total | ||

| 2022 | 6.6 | 39.0 | 45.6 | 0.03% | 0.15% | 0.18% | 5.91 |

| 2023 | 7.2 | 38.1 | 45.3 | 0.03% | 0.15% | 0.18% | 5.29 |

| 2024 | 7.9 | 36.6 | 44.5 | 0.03% | 0.15% | 0.18% | 4.63 |

1.2.4 RCA No. 2 Account as at 31 March 2020

- The balance of the RCA No. 2 Account is $1,272 million;

- the actuarial liability is $1,142 million;

- the resulting actuarial excess is $130 million.

1.3 Valuation Basis

This report is based on pension benefit provisions enacted by the legislation, summarized in Appendices A and B.

The Public Service Superannuation Act was amended by Bill C-97 which received Royal Assent on 21 June 2019. The amendment modified the rule regarding the non-permitted surplus, increasing the permitted surplus from 10% to 25% of liabilities.

Other minor amendments applied to the PSSA and the Public Service Superannuation Regulations since the previous valuation. Those modifications did not have any impact on the actuarial valuation of the plan.

The Funding Policy for the Public Sector Pension Plans (Funding Policy) was approved by the Treasury Board in 2018. The policy provides guidance and rules to support prudent governance of the plansFootnote 8 and ensures that sufficient assets are accumulated to meet the cost of the accrued pension benefits. The methods, assumptions and results of this actuarial valuation are consistent with the provisions of the Funding Policy.

The financial data on which this valuation is based on are composed of:

- The Pension Fund invested assets that the government has earmarked for the payment of benefits for service since 1 April 2000;

- the Superannuation Account established to track the government’s pension benefit obligations for service prior to 1 April 2000.

- the RCA Accounts established to track the benefit obligations in excess of those that can be provided under the Income Tax Act limits for registered pension plans.

These pension assets and account balances are summarized in Appendix C.

The membership data are provided by the Department of Public Services and Procurement Canada (PSPC). Membership data and tests performed on them are summarized in Appendix D.

The valuation was prepared using accepted actuarial practices, methods and assumptions, which are summarized in Appendices E to I.

All actuarial assumptions used in this report are best-estimate assumptions and do not include any margin for adverse deviations. They are independently reasonable and appropriate in aggregate for the purposes of the valuation at the date of this report.

Actuarial assumptions used in the previous report were revised based on economic trends and demographic experience. A complete description of the assumptions is detailed in Appendices F to I.

Table 7 presents a summary of the ultimate economic assumptions used in this report and those used in the previous report.

| 31 March 2020 | 31 March 2017 | |

|---|---|---|

| Assumed level of inflation | 2.0% | 2.0% |

| Real increase in average pensionable earnings | 0.7% | 0.8% |

| Real rate of return on the Pension Fund | 3.9% | 4.0% |

| Real projected yield on the Superannuation Account | 2.1% | 2.7% |

| Real projected yield on the RCA No. 1 and No. 2 Accounts | 2.1% | 2.7% |

Table 8 presents a summary of the demographic assumptions used in this report and those used in the previous report.

| 31 March 2020 | 31 March 2017 | |

|---|---|---|

| Promotional and seniority rate of increase | ||

| Male | 0.6 - 5.9% | 0.6 - 5.6% |

| Female | 0.7 - 6.1% | 0.7 - 5.7% |

| Life expectancy at age 65Table 8 footnote 1 | ||

| Male | 22.9 years | 21.9 years |

| Female | 24.6 years | 23.7 years |

| Average retirement age | ||

| Group 1 | 60.1 years | 59.3 years |

| Group 2 | 62.1 years | 61.6 years |

Table 8 footnote

|

||

We have reflected the impacts of the COVID-19 pandemic on the economic assumptions used in this report. Notable examples are assumptions for plan years 2020 to 2024 for the Year’s Maximum Pensionable Earnings (YMPE) and the Maximum Pensionable Earnings (MPE). The impact of COVID-19 on the economic assumptions is explained in Appendix F. It is important to note that the pandemic is a very fluid situation that will likely continue to evolve for some time. We have estimated the impacts based on the information known at the time the report was prepared. The final impacts of this health and economic crisis will likely generate some differences in the future.

2. Valuation Results

This report is based on the pension benefit provisions enacted by the legislation, summarized in Appendices A and B, and the financial and membership data, summarized in Appendices C and D, respectively. The valuation was prepared using accepted actuarial practices, methods and assumptions summarized in Appendices E to I. Emerging experience that differs from the corresponding assumptions will result in gains or (losses), which will be revealed in subsequent reports.

2.1 PSSA - Financial Position

Since 1 April 2000, member and government contributions to the PSPP are credited to the Pension Fund, and the total amount of contributions net of benefits paid and administrative expenses is transferred to the Public Sector Pension Investment Board (PSPIB) and invested in the financial markets.

This section presents the financial positions for both PSSA financing arrangements as at 31 March 2020. The results of the previous valuation are also shown for comparison.

| 31 March 2020 | 31 March 2017 | |

|---|---|---|

| Recorded Account balance | 91,516 | 94,209 |

| Present value of prior service contributions | 21 | 61 |

| Total | 91,537 | 94,270 |

| Actuarial Liability | ||

| Active contributors | 12,422 | 17,142 |

| Non-active contributors | 111 | 80 |

| Retirement pensioners | 76,266 | 69,978 |

| Disability pensioners | 2,523 | 2,617 |

| Surviving dependents | 6,985 | 6,526 |

| Outstanding payments | 7 | 12 |

| Administrative expenses | 523 | 782 |

| Total Actuarial Liability | 98,837 | 97,137 |

| Actuarial Excess/(Shortfall) | (7,300) | (2,867) |

In accordance with the PSSA, the actuarial shortfall of $7,300 million could be amortized over a maximum period of 15 years beginning on 31 March 2022. If the shortfall is amortized over the maximum period, 15 equal annual credits of $626 million could be made to the Superannuation Account. The time, manner and amount of such credits are to be determined by the President of the Treasury Board.

It is expected that the government will eliminate the actuarial shortfall of the Superannuation Account by making a one-time credit of $7,805 million as at 31 March 2022 to take into account the interest on the shortfall accumulated from 31 March 2020 to 31 March 2022.

| 31 March 2020 | 31 March 2017 | |

|---|---|---|

| Assets | ||

| Market value of assets | 123,433 | 98,770 |

| Actuarial smoothing adjustmentTable 10 footnote 1 | 1,248 | (6,672) |

| Present value of prior service contributions | 728 | 858 |

| Total actuarial value of assets | 125,409 | 92,956 |

| Actuarial Liability | ||

| Active contributors | 68,398 | 57,387 |

| Non-active contributors | 210 | 114 |

| Retirement pensioners | 39,237 | 27,617 |

| Disability pensioners | 1,929 | 1,435 |

| Surviving dependents | 963 | 624 |

| Outstanding payments | 172 | 136 |

| Total Actuarial Liability | 110,909 | 87,313 |

| Actuarial Surplus/(Deficit) | 14,500 | 5,643 |

Table 10 footnote

|

||

As at 31 March 2020, the Pension Fund has a surplus of $14,500 million and the funding ratio is 113.1%. As such, no special payments are required and there is no non-permitted surplusFootnote 9.

2.2 PSSA - Reconciliation of the Changes in Financial Position

Table 11 shows the reconciliation of the changes in the financial positions of the Superannuation Account and the Pension Fund. Explanations of the items largely responsible for the changes follow the table.

| Superannuation Account Actuarial Excess/(Shortfall) |

Pension Fund Actuarial Surplus/(Deficit) |

|

|---|---|---|

| As at 31 March 2017 | (2,867) | 5,643 |

| Recognized investment gains as at 31 March 2017 | - | 6,672 |

| Change in methodology | (57) | 1,235 |

| Retroactive changes to the population data | (129) | (895) |

| Revised Initial Financial Position as at 31 March 2017 | (3,053) | 12,655 |

| Expected interest on initial financial position | (381) | 2,036 |

| Special credits / payments | 3,225 | 377 |

| Net experience gains and (losses) | 327 | 1,479 |

| Revision of actuarial assumptions | (7,598) | (3,400) |

| Change in the present value of administrative expenses | 181 | - |

| Change in the present value of prior service contributions | (1) | 105 |

| Unrecognized investment losses as at 31 March 2020 | - | 1,248 |

| As at 31 March 2020 | (7,300) | 14,500 |

2.2.1 Recognized Investment Gains as at 31 March 2017

An actuarial asset valuation method that minimizes the impact of short-term fluctuations in the market value of assets was used in the previous valuation report, causing the actuarial value of the Pension Fund assets to be $6,672 million less than its market value.

2.2.2 Change in Methodology

Two changes occurred since the last valuation:

- A new actuarial valuation software was used to complete the valuation.

- As a result of the change in actuarial valuation software, the Age Last approach was replaced by an Age Nearest approach. These two methodologies are detailed in Appendix E.2.4.

The combined changes increased the Superannuation Account liability by $57 million and decreased the Pension Fund liability by $1,235 million.

2.2.3 Retroactive Changes to the Population Data

The population data maintained by PSPC is constantly subject to retroactive changes such as new collective agreements. The impacts of these changes increased the Superannuation Account liability as at 31 March 2017 by $129 million and the initial Pension Fund liability as at the same date by $895 million.

2.2.4 Expected Interest on Revised Initial Financial Position

The amount of interest expected to accrue during the intervaluation period increased the shortfall by $381 million for the Superannuation Account and increased the surplus by $2,036 million for the Pension Fund.

These amounts of interest were based on the Superannuation Account yields and the Pension Fund returns projected in the previous report for the three-year intervaluation period.

2.2.5 Special Credits and Payments Made in the Intervaluation Period

The government made a one-time special credit to eliminate the $2,867 million shortfall reported in the Superannuation Account as at 31 March 2017. After factoring the expected interest, this credit resulted in an increase of $3,225 million in the recorded balance of the Superannuation Account as at 31 March 2020.

A deficit was reported in the Pension Fund as at 31 March 2014 which were to be amortized over a period of 15 years in accordance with the legislation. A special paymenf of $340 million was made to the Pension Fund during the intervaluation period that resulted in an increase of $377 million in the assets of the Pension Fund after factoring the expected interest to 31 March 2020.

2.2.6 Experience Gains and (Losses)

Since the previous valuation, experience gains and losses decreased the Superannuation Account shortfall by $327 million and increased the Pension Fund surplus by $1,479 million. The main experience gain and loss items are shown in Table 12.

| Superannuation Account | Pension Fund | |

|---|---|---|

| Demographic experience (i) | ||

| New members | $30 | $140 |

| Rehired pensioner members | 0 | (35) |

| Terminations | (5) | (262) |

| Retirements | (382) | (599) |

| Disabilities with an annuity | (13) | (62) |

| Active deaths | 8 | (133) |

| Retired pensioner mortality | (216) | (70) |

| Disabled pensioner mortality | (23) | (55) |

| Widow(er) mortality | 8 | 0 |

| Total | (593) | (1,076) |

| Investment earnings (ii) | (56) | 583 |

| Service/contributions difference (iii) | 2 | 571 |

| Expected/actual disbursements (iv) | (39) | 172 |

| Pension indexation (v) | 381 | 218 |

| Promotional and seniority increases (vi) | 223 | 999 |

| Economic salary increases (vii) | 43 | 321 |

| YMPE and MPE increases | 0 | 16 |

| Outstanding payments | 5 | (36) |

| Pension benefit division | 6 | 52 |

| Administrative expenses | 17 | (13) |

| Miscellaneous | 338 | (329) |

| Experience Gains and (Losses) | 327 | 1,479 |

-

The net impact of the demographic experience increased the Superannuation Account liability by $593 million and the Pension Fund liability by $1,076 million. The increases in liability were largely due to

- higher than expected number of retirements;

- higher transfer values paid upon termination of active members;

- mortality experience was different than expected, resulting in a loss.

-

The rates of interest credited to the Superannuation Account were in aggregate smaller than the corresponding projected Account yields in the previous valuation resulting in an experience loss of $56 million.

The return realized on the Pension Fund for plan years 2018 to 2020 were 9.8%, 7.1% and -0.6% versus the expected returns of 4.7%, 5.1%, and 5.5%, respectively. Consequently, the Pension Fund experienced an investment gain of $583 million over the three‑year intervaluation period.

-

Unexpected revised credited service resulted in a decrease of $2 million in the Superannuation Account shortfall. Lower than anticipated part-time service and service buyback contributions resulted in an increase of $571 million in the Pension Fund surplus.

-

Higher than anticipated pension payments resulted in an increase of $39 million in the Superannuation Account shortfall, while lower than anticipated pension payments resulted in an increase of $172 million in the Pension Fund surplus.

-

The pension benefit indexation rates for the period from January 2018 to January 2020 were, in aggregate, 0.6% lower than the projected pension indexation, resulting in a $381 million decrease in the Superannuation Account liability and a $218 million decrease in the Pension Fund liability.

-

Lower than expected promotional salary increases resulted in a decrease of $223 million in the Superannuation Account liability and a decrease of $999 million in the Pension Fund liability.

-

Lower than anticipated economic salary increases resulted in a decrease of $43 million in the Superannuation Account liability and a decrease of $321 million in the Pension Fund liability.

2.2.7 Revision of Actuarial Assumptions

Actuarial assumptions were revised based on economic trends and demographic experience as described in Appendices F to I. These revisions have increased the Superannuation Account shortfall by $7,598 million and decreased the Pension Fund surplus by $3,400 million. The impact of these revisions is shown in Table 13 with the most significant items discussed thereafter.

| Assumptions | Superannuation Account |

Pension Fund |

|---|---|---|

| Economic assumptions | ||

| Yields and Rates of return | (7,304) | (4,921) |

| Increase in average pensionable earnings | 108 | 2,120 |

| Pension indexation | (56) | (48) |

| Total | (7,252) | (2,849) |

| Demographic assumptions | ||

| Withdrawals | (8) | (91) |

| Pensionable retirements | (45) | (20) |

| Disabled retirements | (3) | 11 |

| Healthy pensioner and contributor mortality rates | (656) | (718) |

| Disabled pensioner mortality rates | 26 | 15 |

| Spouse mortality rates | (56) | (42) |

| Proportion married at death of member | 163 | 105 |

| Promotional salary increases | 8 | 104 |

| Spouse Age difference | 225 | 49 |

| Proportion of Member Electing for deferred pension | 0 | 11 |

| Other items | 0 | 25 |

| Total | (346) | (551) |

| Net impact of revision | (7,598) | (3,400) |

The net impact of the revision of the assumptions is largely attributable to the changes in economic assumptions.

The following revisions were made to the economic assumptions used in the previous report:

- ultimate real rate of return on the Pension Fund decreased from 4.0% to 3.9%;

- ultimate real projected yield on the Superannuation Account was decreased from 2.7% to 2.1%;

- ultimate real increases in YMPE and MPE were decreased from 1.1% to 1.0%; and

- ultimate real increase in average pensionable earnings decreased from 0.8% to 0.7%.

Details of the changes in economic assumptions are described in Appendix F.

The main revision to the demographic assumptions is a change to the mortality improvement rates. Details of the changes in demographic assumptions are described in Appendix G.

2.2.8 Change in the Present Value of Administrative Expenses

The previous report annual administrative expense assumption of 0.45% of total pensionable payroll decreased to 0.40% in this report. This decrease is based on an analysis of the trend in administrative expenses charged to both the Superannuation Account and the Pension Fund over the last three years.

For plan year 2021, 44% of total administrative expenses are being charged to the Superannuation Account; it is assumed that the proportion charged to the Superannuation Account will reduce at the rate of 2.0% per year as in the previous report. These changes in the annual administrative expenses resulted in an decrease of $181 million of the Superannuation Account shortfall as at 31 March 2020.

2.2.9 Change in the Present Value of Prior Service Contributions

New members’ prior service election paid through instalments since the last report and changes to payment schedules for some members resulted in a change in the present value of prior service contributions. This change increased the Superannuation Account shortfall by $1 million and the Pension Fund surplus by $105 million.

2.2.10 Unrecognized Investment Gains

An actuarial asset valuation method that minimizes the impact of short-term fluctuations in the market value of assets was also used for this valuation. This method, which is described in Section E.1, resulted in an actuarial value of assets that is $1,248 million more than the market value of the Pension Fund assets as at 31 March 2020.

2.3 PSSA - Cost Certificate

2.3.1 Current Service Cost

The details of the current service cost for plan year 2022 and reconciliation with the 2019 current service cost are shown below.

| Member required contributions | 2,675 |

|---|---|

| Government current service cost | 2,701 |

| Total current service cost | 5,376 |

| Expected pensionable payroll | 27,332 |

| Total current service cost as % of expected pensionable payroll | 19.67% |

| For plan year 2019 | 20.16 |

|---|---|

| Expected current service cost change | (0.47) |

| Change in methodology | (0.20) |

| Change in demographics | (0.47) |

| Changes in assumptions | |

| Economic assumptions | 0.47 |

| Demographic assumptions | 0.18 |

| For plan year 2022 | 19.67 |

2.3.2 Projection of Current Service Costs

The current service cost is borne jointly by the plan members and the government. Group 1 and Group 2 member contribution rates are determined such that the government share of the current service cost contribution is 50%. They are determined on a calendar year basis and are shown in Table 2.

Current service costs on a plan year basis, expressed in dollar amount as well as in percentage of the projected pensionable payroll, are shown in Table 16.

| Plan Year | $ Millions | Percentage of Pensionable Payroll | Portion Borne by the GovernmentTable 16 footnote 1 |

||||

|---|---|---|---|---|---|---|---|

| Contributors | Government | Total | Contributors | Government | Total | ||

| 2022 | 2,675 | 2,701 | 5,376 | 9.79% | 9.88% | 19.67% | 50.23% |

| 2023 | 2,778 | 2,807 | 5,585 | 9.73% | 9.83% | 19.56% | 50.26% |

| 2024 | 2,874 | 2,904 | 5,778 | 9.67% | 9.77% | 19.44% | 50.26% |

| 2025 | 2,971 | 3,003 | 5,974 | 9.63% | 9.74% | 19.37% | 50.28% |

Table 16 footnote

|

|||||||

2.3.3 Administrative Expenses

The Pension Fund administrative expenses are included in the total current service costs and are estimated to be as follows.

| Plan Year | ($ millions) |

|---|---|

| 2022 | 68 |

| 2023 | 74 |

| 2024 | 79 |

| 2025 | 84 |

The Superannuation Account administrative expenses have been capitalized and are shown as a liability in the balance sheet.

2.3.4 Contributions for Prior Service Elections

Member and government contributions for prior service elections were estimated as follows:

| Plan Year | Superannuation Account | Pension Fund | ||

|---|---|---|---|---|

| Contributors | Government | Contributors | Government | |

| 2022 | 2 | 2 | 97 | 71 |

| 2023 | 2 | 1 | 95 | 67 |

| 2024 | 1 | 1 | 93 | 63 |

| 2025 | 1 | 1 | 92 | 59 |

2.4 Sensitivity of Valuation Results to Assumptions

The information required by statute, which is presented in the main report, has been derived using best‑estimate assumptions regarding future demographic and economic trends. The key best‑estimate assumptions, i.e. those for which changes within a reasonable range have the most significant impact on the long-term financial results, are described in Appendices F and G. Given the length of the projection period and the number of assumptions required, it is unlikely that the actual experience will develop precisely in accordance with the best‑estimate assumptions. Individual sensitivity tests have been performed, projecting the pension plan’s financial status using alternative assumptions.

This valuation assumes that the current mortality rates applicable to members of the PSPP will improve over time in line with the mortality improvement assumption contained in the 30th Actuarial Report on the Canada Pension Plan. Table 19 presents the effect of varying the mortality improvement assumption on the plan year 2021 current service cost and the liabilities for the Superannuation Account and the Pension Fund. The best-estimate mortality improvement assumption is described in Table 61 of Appendix G.

| Mortality Improvement Rates | Current Service Cost as a percentage of pensionable payroll |

Actuarial Liability ($ millions) | Age 65 Life Expectancy in 2020 | |||||

|---|---|---|---|---|---|---|---|---|

| Superannuation Account |

Pension Fund | |||||||

| Male | Female | |||||||

| 2022 | Effect | Effect | Effect | |||||

| Best-estimate basis | 19.67 | None | 98,837 | None | 110,909 | None | 22.9 | 24.6 |

| - if 0% | 18.94 | (0.73) | 95,606 | (3,231) | 107,313 | (3,596) | 21.5 | 23.3 |

| - if ultimate 50% higher | 19.82 | 0.15 | 99,126 | 289 | 111,503 | 594 | 23.1 | 24.8 |

| - if ultimate 50% lower | 19.51 | (0.16) | 98,551 | (286) | 110,313 | (596) | 22.6 | 24.5 |

| - if kept at 2021 level | 20.23 | 0.56 | 100,677 | 1,840 | 113,413 | 2,504 | 23.9 | 25.4 |

Table 20 shows the effect on the plan year 2022 current service cost and the liabilities for the Superannuation Account and the Pension Fund when key economic assumptions are varied by one percentage point per annum.

| Assumption(s) Varied | Current Service Cost (%) | Actuarial Liability ($ millions) | ||||

|---|---|---|---|---|---|---|

| Superannuation Account | Pension Fund | |||||

| 2022 | Effect | Effect | Effect | |||

| None (i.e. current basis) | 19.67 | None | 98,837 | None | 110,909 | None |

| Investment yield/return | ||||||

| - if 1% higher | 15.80 | (3.87) | 88,204 | (10,633) | 93,866 | (17,043) |

| - if 1% lower | 25.03 | 5.36 | 111,769 | 12,932 | 133,072 | 22,163 |

| Pension indexation | ||||||

| - if 1% higher | 21.97 | 2.30 | 110,989 | 12,152 | 124,634 | 13,725 |

| - if 1% lower | 17.71 | (1.96) | 88,599 | (10,238) | 99,267 | (11,642) |

| Salary, YMPE and MPE | ||||||

| - if 1% higher | 21.53 | 1.86 | 98,990 | 153 | 115,933 | 5,024 |

| - if 1% lower | 18.10 | (1.57) | 98,703 | (134) | 106,523 | (4,386) |

| InflationTable 20 footnote 1 | ||||||

| - if 1% higher | 19.21 | (0.46) | 98,433 | (404) | 109,463 | (1,446) |

| - if 1% lower | 20.15 | 0.48 | 99,263 | 426 | 112,410 | 1,501 |

Table 20 footnote

|

||||||

The differences between the results above and those shown in the valuation can also serve as a basis for approximating the effect of other numerical variations in one of a key assumptions to the extent that such effects are assumed to be linear.

2.5 RCA - Financial Position

This section shows the financial position of the RCA accounts as at 31 March 2020. The results of the previous valuation are also shown for comparison.

| 31 March 2020 | 31 March 2017 | |

|---|---|---|

| RCA No. 1 recorded account balance | 1,315 | 1,193 |

| Refundable tax | 1,297 | 1,184 |

| Present value of prior service contributions | 3 | 2 |

| Total | 2,615 | 2,379 |

| Actuarial Liability | ||

| Pensionable excess earnings | ||

| • Active contributors | 689 | 592 |

| • Pensioners | 1,003 | 666 |

| Survivor Allowance | ||

| • Active contributors | 99 | 97 |

| • Pensioners | 363 | 228 |

| Former deputy heads | 38 | 35 |

| Total Actuarial Liability | 2,192 | 1,618 |

| Actuarial Excess/(Shortfall) | 423 | 761 |

The sum of the recorded balance of the RCA No. 1 Account, the refundable tax and the present value of prior service cost contributions as at 31 March 2020 is $2,615 million, which exceeds the actuarial liability of $2,192 million by $423 million.

| 31 March 2020 | 31 March 2017 | |

|---|---|---|

| RCA No. 2 Recorded Account Balance | 628 | 718 |

| Refundable tax | 644 | 731 |

| Total | 1,272 | 1,449 |

| Actuarial Liability | 1,142 | 1,208 |

| Actuarial Excess/(Shortfall) | 130 | 241 |

Since the previous valuation, the actuarial excess of the RCA No. 2 Account reduced from $241 million to $130 million.

2.6 RCA No. 1 Current Service Cost

The projected current service cost, which is borne jointly by the members and the government, decreased by 0.05% to 0.18% of pensionable payroll in this valuation for plan year 2022 from 0.23% of pensionable payroll calculated in the previous actuarial report.

The RCA No. 1 current service cost is estimated to be 0.18% of pensionable payroll for plan year 2022 to 2025.

Table 23 shows the estimated RCA No. 1 current service cost for the next four plan years.

| Plan Year | ||||

|---|---|---|---|---|

| 2022 | 2023 | 2024 | 2025 | |

| Total current service cost | ||||

| Pensionable excess earnings | 34.1 | 33.3 | 32.2 | 30.8 |

| Survivor allowance | 11.5 | 12.3 | 12.9 | 13.6 |

| Total | 45.7 | 45.7 | 45.2 | 44.4 |

| Member contributions | ||||

| Pensionable excess earnings | 7.9 | 6.8 | 7.4 | 8.0 |

| Total | 7.9 | 6.8 | 7.4 | 8.0 |

| Government current service cost | 37.8 | 38.9 | 37.8 | 36.4 |

The current service cost for former deputy heads is negligeable for years 2022 to 2025, due to the very low number of active members.

2.7 Summary of Estimated Government Costs

Table 24 summarizes the estimated total government credits for the RCA No. 1 and the Superannuation Account on a plan year basis. Table 25 summarizes the estimated total government costs for the Pension Fund on a plan year basis.

| Plan Year | RCA No. 1 | Superannuation Account | Total Government Credits | |

|---|---|---|---|---|

| Current Service Cost | Total Prior Service Contributions | Expected Special Credits | ||

| 2022 | 38 | 2 | 7,805 | 7,845 |

| 2023 | 39 | 1 | 0 | 40 |

| 2024 | 38 | 1 | 0 | 39 |

| 2025 | 36 | 1 | 0 | 37 |

| Plan Year | Current Service Cost | Total Prior Service Contributions | Total Government Cost |

|---|---|---|---|

| 2022 | 2,701 | 71 | 2,772 |

| 2023 | 2,807 | 95 | 2,902 |

| 2024 | 2,904 | 93 | 2,997 |

| 2025 | 3,003 | 92 | 3,095 |

3. Actuarial Opinion

In our opinion, considering that this report was prepared pursuant to the Public Pensions Reporting Act,

- the valuation data on which the valuation is based are sufficient and reliable for the purposes of the valuation;

- the assumptions used are individually reasonable and appropriate in aggregate for the purposes of the valuation; and

- the methods employed are appropriate for the purposes of the valuation.

This report has been prepared, and our opinion given, in accordance with accepted actuarial practice in Canada. In particular, this report was prepared in accordance with the Standards of Practice (General Standards and Practice - Practice-Specific Standards for Pension Plans) published by the Canadian Institute of Actuaries.

We have reflected the impacts of the COVID-19 pandemic on the economic assumptions used in this report. It is important to note that the pandemic is a very fluid situation that will likely continue to evolve for some time. We have estimated the impacts based on the information known at the time the report was prepared. The final impacts of this health and economic crisis will likely generate some differences in the future.

To the best of our knowledge, after discussion with Public Services and Procurement Canada and the Treasury Board of Canada Secretariat, there were no subsequent events between the valuation date and the date of this report that would have a material impact on the results of this valuation.

Assia Billig, FCIA, FSA

Chief Actuary

Laurence Frappier, FCIA, FSA

Véronique Ménard, FCIA, FSA

Ottawa (Canada)

29 September 2021

Appendix A - Summary of Pension Benefit Provisions

The government has been providing its employees with a pension plan since 1870. Pensions for members of the Public Service are provided primarily under the Public Service Superannuation Act (PSSA) as enacted in 1954 and modified thereafter. Benefits are also provided to public servants under the Special Retirement Arrangements Act. Benefits may be modified in accordance with the Pension Benefits Division Act if there is a breakdown of a spousal union.

Changes Since the Last Valuation

The Public Service Superannuation Actwas amended by Bill C-97 which received Royal Assent on 21 June 2019. The amendment modified the rule regarding the non-permitted surplus, increasing the permitted surplus from 10% to 25% of liabilities.

Other minor amendments applied to the PSSA and the Public Service Superannuation Regulations since the previous valuation. Those modifications did not have any impact on the actuarial valuation of the plan.

Summary of Pension Benefit Provisions

Summarized in this Appendix are the pension benefits provided under the PSSA registered provisions, which are in compliance with the Income Tax Act. The portion of the benefits in excess of the Income Tax Act limits for registered pension plans is provided under the retirement compensation arrangements described in Appendix B.

In case of any discrepancy between this summary and the legislation, the legislation shall prevail.

A.1 Membership

Subject to the exceptions mentioned in the next paragraph, membership in the plan is compulsory for all full‑time and part-time employees working 12 or more hours per week (except those who were grandfathered as at 4 July 1994) in the Public Service. This includes all positions in any department or portion of:

- the Executive Government of Canada;

- the Senate and the House of Commons;

- the Library of Parliament; and

- any board, commission or corporation listed in a Schedule to the Act, as well as those designated as contributors by the President of the Treasury Board either individually or as members of a class for persons engaged as seasonal employees and some others.

The main groups of persons employed in the Public Service to which the Act does not apply are:

- part-time employees working less than 12 hours per week;

- persons locally engaged outside Canada;

- employees of some Crown corporations, boards or commissions covered by their own pension plans; and

- seasonal employees, and some others, unless designated as contributors by the President of the Treasury Board.

Since the previous valuation, no entities have left the plan.

A.2 Contributions

A.2.1 Members

Different contribution rates apply to Group 1Footnote 10 and Group 2Footnote 11 contributors. The expected rates are consistent with the government objective of maintaining a 50:50 employer to employee current service cost sharing ratio.

During the first 35 years of pensionable service, members contribute according to the rates shown in the following table.

| Calendar year | Group 1 | Group 2 | ||

|---|---|---|---|---|

| Below YMPE | Above YMPE | Below YMPE | Above YMPE | |

| 2020Table 26 footnote 1 | 9.53% | 11.72% | 8.69% | 10.15% |

| 2021Table 26 footnote 2 | 9.83% | 12.26% | 8.89% | 10.59% |

| 2022 | 9.36% | 12.48% | 7.95% | 11.82% |

| 2023 | 9.35% | 12.37% | 7.93% | 11.72% |

| 2024 | 9.35% | 12.25% | 7.94% | 11.54% |

Table 26 footnotes

|

||||

The contribution rates shown after calendar year 2022 are estimates and subject to change.

After 35 years of pensionable service, members contribute only 1% of pensionable earnings.

In order to keep their rights to an early retirement benefit, deemed operational members of Correctional Service Canada (CSC) contribute 0.62% of total earnings during a calendar year in addition to the above contribution rates.

A.2.2 Government

A.2.2.1 Current Service

The government determines the normal monthly contribution as the amount which, when combined with the required contributions by members in respect of current service and expected interest earnings, is sufficient to cover the cost, as estimated by the President of the Treasury Board, of all future payable benefits that have accrued in respect of pensionable service during that month and the Pension Fund administrative expenses incurred during that month.

A.2.2.2 Elected Prior Service

The government matches member contributions made to the Superannuation Account for prior service elections; however, it makes no contributions if the member is paying the double rate.

Government contributions to the Pension Fund in respect of elected prior service are calculated using the same ratio of Government contributions to employee contributions as for the current service cost. For member paying the double rate, the government contributes only the excess of the ratio of Government contributions to employee contributions over 1.

A.2.2.3 Actuarial Excess and Surplus

The PSSA gives the government the authority to:

- debit the excess of the Superannuation Account over the actuarial liability subject to limitations, and

- deal with any actuarial surplus, subject to limitations, in the Pension Fund as they occur, either by

- reducing employer contributions or

- reducing employer and employee contributions or

- by making withdrawals.

A.2.2.4 Actuarial Shortfall and Deficit

In accordance with the PSSA, if either a Superannuation Account actuarial shortfall or a Pension Fund actuarial deficit is identified through a triennial statutory actuarial valuation, the actuarial shortfall/deficit can be amortized over a period of up to 15 years.

The President of the Treasury Board will determine the time, the manner and the amount of credits to be made. The shortfall/deficit must be fully paid by the end of the fifteenth fiscal year following the tabling of that report at the latest.

A.3 Summary Description of Benefits

The objective of the PSPP is to provide an employment earnings-related lifetime retirement pension to eligible members. Benefits to members in case of disability and to the spouse and children in case of death are also provided.

Subject to coordination with the pensions paid by the Canada Pension Plan (CPP) or the Québec Pension Plan (QPP), the initial rate of retirement pension is equal to 2% of the highest average of annual pensionable earnings over any period of five consecutive years, multiplied by the number of years of pensionable service not exceeding 35. Once in pay, the pension is indexed annually with the Consumer Price Index. Such indexation also applies to deferred pensions during the deferral period. Detailed notes on the following overview are provided in the following section.

| Contributor’s Type of Termination | Benefit |

|---|---|

| With less than two years of serviceTable footnote 1 | Return of contributions |

| With two or more years of serviceTable footnote 1; and | |

| Disability | Immediate annuity |

| Death leaving no surviving spouse or eligible children | Minimum benefit |

| Death leaving surviving spouse and/or eligible children | Survivor allowance(s) |

| Leaving prior to age 45, except for death or disability | |

| Actual operational service between 20 and 25 years | Actual operational service annual allowanceTable footnote 2 |

| Actual operational service 25 years or more | Immediate annuity |

| Otherwise | Deferred annuity or transfer value |

| Leaving at ages 45 to 49, except for death or disability, and | |

| Deemed operational service 20 years or more | Deemed operational service annual allowanceTable footnote 3 |

| Actual operational service between 20 and 25 years | Actual operational service annual allowanceTable footnote 2 |

| Actual operational service 25 years or more | Immediate annuity |

| Otherwise | Deferred annuity or transfer value |

| Leaving at age 50 or over, except for death or disability, and | |

| Deemed operational service between 20 and 25 years | Deemed operational service annual allowanceTable footnote 3 |

| Deemed operational service 25 years or more | Immediate annuity |

| Actual operational service between 20 and 25 years | Actual operational service annual allowanceTable footnote 2 |

| Actual operational service 25 years or more | Immediate annuity |

| Otherwise, but Group 1, age 60 or over, or age 55 or over and service 30 years or more | Immediate annuity |

| Otherwise, but Group 2, age 65 or over, or age 60 or over and service 30 years or more | Immediate annuity |

| Otherwise | Deferred annuity or annual allowance |

| Deferred and Immediate Pensioner’s Type of Termination | Benefit |

| Group 1 disability before age 60 while entitled to a deferred annuity or an annual allowance | Immediate annuity |

| Group 2 disability before age 65 while entitled to a deferred annuity or an annual allowance | Immediate annuity |

| Death leaving no eligible survivor | Minimum benefit |

| Death leaving eligible survivor(s) | Survivor allowance(s) |

Table footnotes

|

|

A.4 Explanatory Notes

A.4.1 Pensionable Earnings

Pensionable earnings means the annual employment earnings (excluding overtime but including pensionable allowances such as bilingual bonuses) of a contributor.

Pensionable payroll means the aggregate pensionable earnings of all contributors with less than 35 years of pensionable service.

A.4.2 Indexation

A.4.2.1 Level of Indexation Adjustments

All immediate and deferred annuities (pensions and allowances) are adjusted every January to the extent warranted by the increase, as at 30 September of the previous year, in the 12-month average Consumer Price Index relative to the corresponding figure one year earlier. If the indicated adjustment is negative, annuities are not decreased for that year; however, it is carried-forward and the next positive adjustment is diminished accordingly.

A.4.2.2 First Indexation Adjustment

Indexation adjustments accrue from the end of the month in which employment terminates. The first annual adjustment following termination of employment is prorated accordingly.

A.4.2.3 Commencement of Indexation Payments

The indexation portion of a retirement, disability or survivor pension normally starts being paid when the pension is put into pay. However, regarding an operational service retirement pension, indexation payments start only when the pensioner is either

- at least 55 years old, provided the sum of age and pensionable service is at least 85; or

- at least 60 years old.

A.4.3 Pensionable Service, Actual Operational Service and Deemed Operational Service

Pensionable service of a contributor includes any period of service in the Public Service for which the contributor has been required to contribute or has elected to contribute, if eligible to do so, and such other types of service for which the contributor has elected to make the required special contributions to the SuperannuationAccount or the Pension Fund. Pensionable service is limited to 35 years.

Actual operational service refers to CSC employees working in federal correctional facilities, parole offices and community correctional centres. More specifically, operational service is defined as service by a person employed by CSC whose principal place of work is not: the national headquarters or a regional headquarters of CSC; the offices of the CSC Commissioner; or a regional CSC Staff College or any other institution that provides similar training to CSC employees.

Deemed operational service refers to CSC employees in operational service for one or more periods totalling at least 10 years, who then cease to be engaged in operational service but continue to be employed by CSC and elect to continue to accumulate operational service and contribute an additional 0.62% of earnings.

A.4.4 Return of Contributions

Return of contributions means the payment of an amount equal to the accumulated current and prior service contributions paid or transferred by the contributor into the plan. Interest is credited quarterly on returned contributions in accordance with the investment return on the Pension Fund.

A.4.5 Immediate Annuity

Immediate annuity means an unreduced pension that becomes payable immediately upon a pensionable retirement or pensionable disability. The annual amount is equal to 2% of the highest average of annual pensionable earnings of the contributor over any period of fiveFootnote 12 consecutive years, multiplied by the number of years of pensionable service not exceeding 35. For contributors with periods of part-time pensionable service, earnings used in the five-year average are based on a full 37.5‑hour workweek but the resulting average is multiplied by the proportion of the actual workweek over a full workweek averaged by the contributor over the entire period of pensionable service.

When a pensioner attains age 65 or becomes entitled to a disability pension from the CPP or the QPP, the annual pension amount is reduced by a percentage of the indexed CPP annual pensionable earningsFootnote 13 (or, if lesser, the indexed five-yearFootnote 12 pensionable earnings average on which the immediate annuity is based), multiplied by the years of CPP pensionable serviceFootnote 14. The applicable percentage is 0.625%.

Annuities are payable at the end of month until the month in which the pensioner dies or until the disabled pensioner recovers from disability (the last payment would then be pro-rated). Upon the death of the pensioner, either a survivor allowance (Note A.4.13) or a residual death benefit (Note A.4.14) may be payable.

A.4.6 Deferred Annuity

Deferred annuity means an annuity that normally becomes payable to a former Group 1 contributor who reaches age 60 or a former Group 2 contributor who reaches age 65. The annual payment is determined as for an immediate annuity (Note A.4.5) but is also adjusted to reflect the indexation (Note A.4.2) from the date of termination to the commencement of benefit payments.

The deferred annuity of a former Group 1 contributor becomes an immediate annuity during any period of disability beginning before age 60. If the disability ceases before age 60, the immediate annuity reverts to the original deferred annuity unless the pensioner elects an annual allowance (Notes A.4.8, A.4.9, and A.4.10) that is the prescribed actuarial equivalent to the deferred annuity. Similarly, the deferred annuity of a former Group 2 contributor becomes an immediate annuity during any period of disability beginning before age 65, and reverts back to the original deferred annuity if the disability ceases before age 65, unless the pensioner elects an annual allowance as described above.

A.4.7 Transfer Value

A contributor who has ceased to be employed in the public service and has to his credit two or more years of pensionable service, is a Group 1 contributor and is under age 50, or is a Group 2 contributor and is under age 55, and is eligible for a deferred annuity may elect to transfer the commuted value of his benefit, determined in accordance with the regulations, to

- a locked-in Registered Retirement Savings Plan of the prescribed kind; or

- another pension plan registered under the Income Tax Act; or

- a financial institution for the purchase of a locked-in immediate or deferred annuity of the prescribed kind.

A.4.8 Annual Allowance For Members

For a Group 1 member, annual allowance means an annuity payable immediately on retirement or upon attaining age 50, if later. The amount of the allowance is equal to the amount of the deferred annuity to which the member would otherwise be entitled, reduced by 5% for each year between 60 and the age when the allowance becomes payable. However, if the member is at least 50 years old at termination, and has at least 25 years of pensionable serviceFootnote 15, then the difference is reduced (subject to the above as a maximum) to the greater of

- 55 minus the age, and

- 30 minus the number of years of pensionable serviceFootnote 15.

For a Group 2 member, the eligibility age is increased by 5 years, so that annual allowance means an annuity payable immediately on retirement or upon attaining age 55 if later. The amount of the allowance is equal to the amount of the deferred annuity to which the member would otherwise be entitled, reduced by 5% for each year between 65 and the age when the allowance becomes payable. However, if the member is at least 55 years old at termination, and has at least 25 years of pensionable serviceFootnote 15, then the difference is reduced (subject to the above as a maximum) to the greater of

- 60 minus the age, and

- 30 minus the number of years of pensionable serviceFootnote 15.

The Treasury Board can waive all or part of the reduction for Group 1 contributors who are involuntarily retired at ages 55 and over with at least 10 years of Public Service employment, or for Group 2 contributors who are involuntarily retired at ages 60 and over with at least 10 years of Public Service employment.

When a Group 1 member in receipt of an annual allowance becomes disabled before reaching age 60, or a Group 2 member in receipt of an annual allowance becomes disabled before reaching age 65, the annual allowance becomes an immediate annuity adjusted in accordance with the regulations to take into account the amount of any annual allowance received prior to becoming disabled.

A.4.9 Deemed Operational Service - Immediate Annuity and Annual Allowance

A deemed operational service immediate annuitydiffers from an immediate annuity (Note A.4.5) only in that it is available as early as age 50 with 25 years of operational service.

A deemed operational service annual allowance differs from an annual allowance (Note A.4.8) in two ways. Firstly it is available as early as age 45 with 20 years of operational service. Secondly the reduction factor is 5% multiplied by the greater of

- 50 minus the age, and

- 25 minus the years of operational service.

The foregoing operational service-related benefits are calculated in relation to both deemed and actual operational service only. Additional non-operational service results in the applicable non-operational benefit where any thresholds or reductions are based on total pensionable service, including operational service.

A.4.10 Actual Operational Service - Immediate Annuity and Annual Allowance

An actual operational service immediate annuitydiffers from an immediate annuity (Note A.4.5 and Note A.4.9) only in that it is available when the member has accrued 25 years of actual operational service.

An actual operational service annual allowance differs from other annual allowances (Note A.4.8 and Note A.4.9) in two ways. Firstly it is available as soon as 20 years of actual operational service is accrued. Secondly the reduction factor is 5% multiplied by

- 25 minus the years of actual operational service.

The foregoing operational service-related benefits are calculated in relation to actual operational service only. Additional non-operational service results in the applicable non-operational benefit where any thresholds or reductions are based on total pensionable service, including operational service. Also, additional deemed operational service results in the applicable deemed operational benefit where any thresholds or reductions are based on operational pensionable service.

A.4.11 Eligible Surviving Spouse

Eligible surviving spouse means the surviving spouse (includes a common-law or same‑sex partner recognized under the plan) of a contributor or pensioner except if:

- the contributor or pensioner died within one year of commencement of the spousal union, unless the Treasury Board is satisfied that the health of the contributor or pensioner at the time of such commencement justified an expectation of surviving for at least one year; or

- the pensioner married after ceasing to be a contributor, unless after such marriage the pensioner either:

- became a contributor again, or

- made an optional survivor benefit election within 12 months following marriage to accept a reduced pension so that the new spouse would be eligible for a survivor benefit. This reduction is reversed if and when the new spouse predeceases the pensioner or the spousal union is terminated for reason other than death.

A.4.12 Eligible Surviving Children

Eligible surviving children includes all children of the contributor or pensioner who are under age 18, and any child of the contributor or pensioner who is age 18 or over but under 25, in full-time attendance at a school or university, having been in such attendance substantially without interruption since he or she reached age 18 or the contributor or pensioner died, whichever occurred later.

A.4.13 Annual Allowance for Eligible Survivor(s)

Annual allowance means, for the eligible surviving spouse and children of a contributor or pensioner, an annuity that becomes payable immediately upon the death of that individual. The amount of the allowance is determined with reference to a basic allowance that is equal to 1% of the highest average of annual pensionable earnings of the contributor over five consecutive years, multiplied by the number of years of pensionable service not exceeding 35.

The annual allowance for a spouse is equal to the basic allowance unless the spouse became eligible as a result of an optional survivor benefit election, in which case it is equal to the percentage of the basic allowance specified by the pensioner making the election.

The annual allowance for an eligible surviving child is equal to 20% of the basic allowance, subject to a reduction if there are more than four eligible surviving children in the same family. The allowance otherwise payable to an eligible surviving child is doubled if there is no eligible surviving spouse.

Survivor annual allowances are not integrated with the CPP or the QPP and are payable in equal monthly instalments in arrears until the end of the month in which the survivor dies or otherwise loses eligibility. If applicable, a residual benefit (Note A.4.14) is payable to the estate upon the death of the last survivor.

A.4.14 Minimum and Residual Death Benefits

If a contributor or a pensioner dies leaving no eligible survivor, the lump sum normally paid is the excess of five times the annual amount of the immediate annuity to which the contributor would have been entitled, or the pensioner was entitled, at the time of death, less any pension payments already received. Indexation adjustments are excluded from these calculations.

The same formula is used to determine the residual death benefit, which is the lump sum payable upon the death of an eligible survivor but also subtracting all amounts (excluding indexation adjustments) already paid to the survivor.

A.4.15 Division of Pension with Former Spouse

In accordance with the Pension Benefits Division Act, upon the breakdown of a spousal union (including common-law), a lump sum can be debited by court order or by mutual consent from the accounts and/or the Pension Fund, as the case may be, to the credit of the former spouse of a contributor or pensioner. The maximum transferable amount is half the value, calculated as at the transfer date, of the retirement pension accrued by the contributor or pensioner during the period of cohabitation. If the member’s benefits are not vested, the maximum transferable amount corresponds to half the member’s contributions made during the period subject to division, accumulated with interest at the rate applicable on a refund of contributions. The accrued benefits of the contributor or pensioner are then reduced accordingly.

Appendix B - Retirement Compensation Arrangement Benefit Provisions

Retirement compensation arrangements (RCAs) are arrangements for benefits in excess of benefit limitations of registered pension plans and therefore are less tax-advantageous as the fund must transfer a 50% refundable tax to the Canada Revenue Agency (CRA) immediately. Under the PSSA RCA a debit is made from the RCA Account such that in total roughly half the recorded balance in the RCA Account is held as a tax credit (CRA refundable tax). This Appendix describes the Public Service pension benefits financed through retirement compensation arrangements (RCA No. 1 and RCA No. 2) rather than through the registered PSSA provisions that have a material impact on this valuation

Effective 15 December 1994, RCA No. 1 was established pursuant to the Special Retirement Arrangements Act (SRAA) to provide for all pension benefits in excess of those that may, in accordance with the Income Tax Act (ITA) restrictions on registered pension plans, be paid under the PSSA registered provisions.

Effective 1 April 1995, RCA No. 2 was established by the RCA regulations as a program for certain Public Service employees declared surplus before 1 April 1998 as part of the downsizing initiative. Participation was limited to individuals between ages 50 and 54 who met the conditions specified in the regulations. RCA No. 2 pays the difference between a pension unreduced for early retirement and the reduced pension payable in accordance with the PSSA. It is financed entirely by the government.

The following benefits have been provided under RCA No. 1 since 20 November 1997, unless otherwise indicated, to the extent that they are in excess of the ITA limit.

| Benefit | PSSA Registered Provisions limit |

|---|---|

| Survivor allowance for service from 1 January 1992 onward (see Note A.4.13 of Appendix A) |

Pre‑retirement death

Post‑retirement death The amount of spouse allowance is limited in any year to a maximum of two-thirds the retirement benefit that would have been payable to the member in that year. |

| Minimum lump sum death benefit (see Note A.4.14 of Appendix A) |

Pre‑retirement death The amount of pre‑retirement death benefit if the member has no eligible dependants is limited to the greater of the member contributions with interest and the present value of the member’s accrued benefits on the day prior to death. Post‑retirement death If the member has no eligible dependants at retirement, then the minimum death benefit is limited to the member contributions with interest. |

| Continued benefit accrual for former deputy heads (provided since 15 December 1994 for service since then) |

This entire benefit is outside the registered plan limit. Deputy heads ceasing employment under age 60 may elect to be deemed full-time employees absent from the Public Service on leave without pay up to age 60. |

| Elective service for service prior to 1 January 1990 |

The amount of lifetime retirement benefits for each such year of service is limited to two-thirds of the defined benefit limit (i.e. $3,245.56 for calendar year 2021) for the year in which the lifetime retirement benefits commence to be paid. For years subsequent to the commencement year of lifetime retirement benefits, this amount can be adjusted to reflect increases in the Consumer Price Index. |

| Excess pensionable earnings (provided since 15 December 1994 for service since then) |

The highest average of pensionable earnings is subject to a prescribed yearly maximum that varies by calendar year and the registered plan’s benefit formula. The calendar year 2021 Maximum Pensionable Earnings is $181,600. |

Appendix C - Assets, Accounts and Rates of Return

C.1 Assets and Account Balances

The government has a statutory obligation to fulfill the pension promise enacted by legislation to members of the Public Service. Since 1 April 2000, the government has earmarked invested assets (the Pension Fund) to meet the cost of pension benefits.

With respect to the unfunded portion of the PSPP, accounts were established to track the government’s pension benefit obligations, such as the Superannuation Account for service prior to 1 April 2000, and the RCA No. 1 and No. 2 Accounts for benefits in excess of those that can be provided under the Income Tax Act limits for registered pension plans.

C.1.1 Public Service Superannuation Account

PSSA member contributions, government costs and benefits earned up to 31 March 2000 are tracked entirely through the Public Service Superannuation Account, which forms part of the Accounts of Canada.

The Superannuation Account is credited with all PSSA member contributions and government costs prior to 1 April 2000, as well as with prior service contributions and costs for elections made prior to 1 April 2000 and for periods before 1 April 2000 but credited after that date. It is charged with both the benefit payments made in respect of service earned under the Superannuation Account and the allocated portion of the plan administrative expenses.

The Superannuation Account is credited with interest earnings as though net cash flows were invested quarterly in 20‑year Government of Canada bonds issued at prescribedFootnote 16 interest rates and held to maturity. No formal debt instrument is issued to the Superannuation Account by the government in recognition of the amounts therein. Interest is credited every three months on the basis of the average yield for the same period on the combined Superannuation Accounts of the Public Service, Canadian Forces and RCMP pension plans.

| Plan Year | 2018 | 2019 | 2020 | 2018-2020 | |

|---|---|---|---|---|---|

| Opening balance as at 1 April of the previous year | 94,209 | 92,536 | 93,700 | 94,209 | |

| INCOME | |||||

| Interest earnings | 3,830 | 3,593 | 3,411 | 10,834 | |

| Employer contributions | 7 | 5 | 3 | 15 | |

| Member contributions | 8 | 6 | 4 | 18 | |

| Transfers received | - | 1 | - | 1 | |

| Actuarial liability adjustments | - | 3,107 | - | 3,107 | |

| Subtotal | 3,845 | 6,712 | 3,418 | 13,975 | |

| EXPENDITURES | |||||

| Annuities | 5,413 | 5,456 | 5,512 | 16,381 | |

| Pension divisions | 17 | 17 | 14 | 48 | |

| Return of contributions | - | - | - | - | |

| Pension transfer value payments | 13 | 10 | 12 | 35 | |

| Transfers to other pension plans | 4 | 4 | 3 | 11 | |

| Minimum benefits | 16 | 15 | 14 | 45 | |

| Administrative expenses | 55 | 46 | 47 | 148 | |

| Subtotal | 5,518 | 5,548 | 5,602 | 16,668 | |

| Closing balance as at 31 March of the plan year | 92,536 | 93,700 | 91,516 | 91,516 | |

Since the last valuation, the Account balance has decreased by $2.7 billion (a 2.9% reduction) to reach $91.5 billion as at 31 March 2020.

C.1.2 Public Service Pension Fund

Since 1 April 2000, PSSA contributions (except for prior service elections made prior to 1 April 2000) have been credited to the Pension Fund. The Pension Fund is invested in the financial markets with a view to achieving maximum rates of return without undue risk.

The Pension Fund has been credited with all PSSA contributions since 1 April 2000, as well as with prior service contributions in respect of elections made since that date. The Pension Fund is also credited with the net investment returns generated by the capital assets managed by PSPIB. It is debited with both the benefit payments made in respect of service earned and prior service elections made since 1 April 2000 and the allocated portion of the plan administrative expenses.

| Plan Year | 2018 | 2019 | 2020 | 2018-2020 |

|---|---|---|---|---|

| Opening balance as at 1 April of the previous year | 98,770 | 111,381 | 121,991 | 98,770 |

| INCOME | ||||

| Investment earnings | 9,805 | 8,070 | (763) | 17,112 |

| Employer contributions | 2,371 | 2,571 | 2,579 | 7,521 |

| Member contributions | 2,414 | 2,627 | 2,656 | 7,697 |

| Transfers received | 51 | 56 | 67 | 174 |

| Actuarial liability adjustments | 340 | - | - | 340 |

| Subtotal | 14,981 | 13,324 | 4,539 | 32,844 |

| EXPENDITURES | ||||

| Annuities | 2,002 | 2,255 | 2,529 | 6,786 |

| Pension divisions | 36 | 42 | 39 | 117 |

| Return of contributions | 15 | 16 | 19 | 50 |

| Pension transfer value payments | 219 | 288 | 388 | 895 |

| Transfers to other pension plans | 37 | 42 | 48 | 127 |

| Minimum benefits | 15 | 19 | 18 | 52 |

| Administrative expenses | 46 | 52 | 56 | 154 |

| Subtotal | 2,370 | 2,714 | 3,097 | 8,181 |

| Closing balance as at 31 March of the plan year | 111,381 | 121,991 | 123,433 | 123,433 |

Since the last valuation, the Pension Fund balance has increased by $24.7 billion (a 25.0% increase) to reach $123.4 billion as at 31 March 2020.

C.1.3 Public Service RCA No. 1 Account

The amount in the RCA No. 1 Account is composed of the recorded balance in the Retirement Compensation Arrangements Account, which forms part of the Accounts of Canada, and a tax credit (CRA refundable tax). Each calendar year, a debit/credit is made from the RCA Account such that in total roughly half the recorded balance in the RCA Account is held as a tax credit (CRA refundable tax).

No formal debt instrument is issued to the RCA No. 1 Account by the government in recognition of the amounts therein. Interest earnings are credited every three months on the basis of the average yield for the same period on the combined Superannuation Accounts of the Public Service, Canadian Forces and RCMP pension plans.

| Plan Year | 2018 | 2019 | 2020 | 2018-2020 |

|---|---|---|---|---|

| Opening balance as at 1 April of the previous year | 1,193 | 1,241 | 1,266 | 1,193 |

| INCOME | ||||

| Interest earnings | 0 | 0 | 0 | 0 |

| Employer contributions | 84 | 41 | 75 | 200 |

| Member contributions | 12 | 14 | 21 | 47 |

| Transfers received | 0 | 0 | 0 | 0 |

| Actuarial liability adjustments | 50 | 49 | 47 | 146 |

| Subtotal | 146 | 104 | 143 | 393 |

| EXPENDITURES | ||||

| Annuities | 45 | 49 | 57 | 151 |

| Pension divisions | 0 | 1 | 0 | 1 |

| Return of contributions | 0 | 0 | 0 | 0 |