Financial highlights for the period ended June 30, 2024

Introduction

Raison d'être

The Office of the Superintendent of Financial Institutions (OSFI) was established in 1987 by an Act of Parliament: the Office of the Superintendent of Financial Institutions Act (OSFI Act). It is an independent agency of the Government of Canada and reports to Parliament through the Minister of Finance.

OSFI supervises and regulates all banks in Canada and federal credit unions in Canada and all federally incorporated or registered trust and loan companies, insurance companies, fraternal benefit societies and private pension plans. Under the OSFI Act, the Superintendent is solely responsible for exercising OSFI's authorities and is required to report to the Minister of Finance from time to time on the administration of the financial institutions legislation.

The Office of the Chief Actuary, which is an independent unit within OSFI, provides actuarial valuation and advisory services for the Canada Pension Plan, the Old Age Security program, the Canada Student Loans and Employment Insurance Programs and other public sector pension and benefit plans.

Responsibilities

OSFI’s purpose is to contribute to public confidence in the Canadian financial system by regulating and supervising approximately 400 federally regulated financial institutions (FRFIs) and 1200 federally regulated pension plans (FRPPs).

OSFI’s mandate is to:

- ensure FRFIs and FRPPs remain in sound financial condition

- ensure FRFIs protect themselves against threats to their integrity and security

- act early when issues arise and require FRFIs and FRPPs to take necessary corrective measures without delay

- monitor and evaluate risks and promote sound risk-management by FRFIs and FRPPs

In exercising its mandate:

- for FRFIs, OSFI strives to protect the rights and interests of depositors and creditors while having due regard for the need to allow FRFIs to compete effectively and take reasonable risks

- for FRPPs, OSFI strives to protect the rights and interests of pension plan members, former members and entitled beneficiaries

OSFI also provides supervision services to the Canada Mortgage and Housing Corporation in accordance with the National Housing Act.

The OCA is an independent unit within OSFI that provides a range of actuarial valuation and advisory services to the Government of Canada.

Basis of Presentation

These quarterly financial statements have been prepared by management as required by Section 65.1 of the Financial Administration Act and in accordance with Public Sector Accounting Standards (PSAS), using the accrual basis of accounting.

These quarterly financial statements have not been subject to an external audit or review.

OSFI’s Funding Model

OSFI recovers its costs from several revenue sources. It is mainly funded through assessments on the financial institutions and private pension plans that it regulates and supervises, as well as through a user-pay program for legislative approvals and other selected services. OSFI also receives revenues for cost-recovered services. These include revenues from provinces on behalf of which OSFI supervises institutions on contract, and revenues from other federal organizations to which OSFI provides administrative support.

The accompanying quarterly financial statements reflect OSFI’s legislated authority to spend revenues from assessments and other sources as per Section 17(2) of the OSFI Act as well as any authorities granted by Parliament and used by OSFI. OSFI receives an annual parliamentary appropriation pursuant to Section 16 of the OSFI Act to support the operations of the Office of the Chief Actuary. Such funding is presented as Government Funding in the Statement of Operations and the amount is consistent with the Main and Supplementary Estimates per the Appropriation Act in effect for the reporting period.

Financial Review and Highlights - Fiscal Year to Date

Statement of Financial Position and Statement of Cash Flows

The majority of OSFI’s revenue is derived from base assessments on federally regulated financial institutions. Assessments are billed annually, usually in the second quarter of the fiscal year. As a result of this annual cycle, some accounts in OSFI’s Statement of Financial Position can vary significantly throughout the year. In between base assessment billings, OSFI’s cash entitlement balance decreases gradually as payments pertaining to operational costs and asset acquisitions are issued. Similarly, OSFI’s accrued base assessments balance increases, to reflect expenses incurred but not yet billed. After the base assessments are billed and collected, cash and accounts receivable increase, as do unearned base assessments. OSFI last invoiced its base assessments in July 2023.

During the three months ended June 30, 2024, OSFI’s cash entitlement balance decreased by $65.0 million, its trade and other receivables increased by $2.0 million, and its accrued base assessments increased by $66.9 million.

As explained in Note 2 (a) to the financial statements, OSFI has a revolving expenditure authority from the Treasury Board Secretariat to draw upon the Consolidated Revenue Fund to ensure the availability of funds prior to receipt of revenue. Additional information on OSFI’s sources and uses of cash can be found in its Statement of Cash Flows.

Statement of Operations

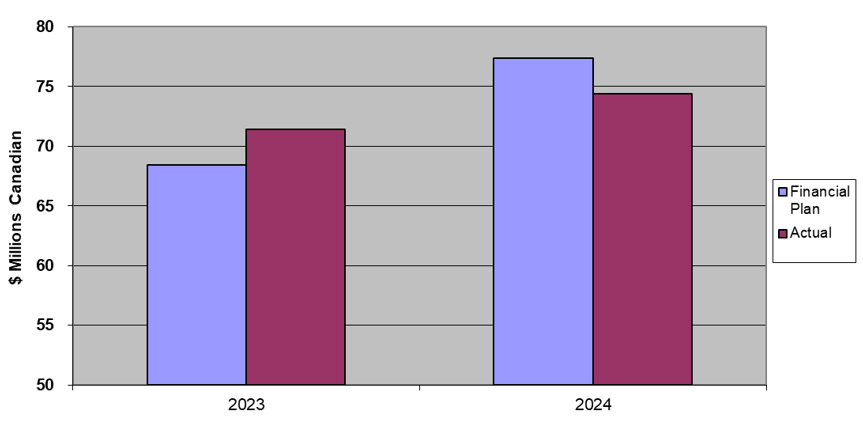

OSFI operates on a cost recovery model. Assessment revenue is recorded at an amount necessary to balance revenue and expenses after all other sources of revenue are taken into account. OSFI’s total expenses for the three months ended June 30, 2024, were $74.4 million, a $2.9 million or 4.1% increase from the same period last year.

- Personnel costs rose by $4.1 million or 7.0% due to the staffing of vacant / new positions in accordance with OSFI’s most recent Operational Plan and normal escalation / merit increases.

- Machinery and equipment costs increased by $0.3 million or 164.9% due to the purchase of furniture and fixtures to continue to fit up office space for OSFI’s hybrid work model.

- Professional services costs decreased by $0.9 million or 14.4% primarily as a result of costs incurred last year related to the implementation of OSFI’s Blueprint for Transformation. OSFI is also aligning with the Government’s Budget 2023 announcement to refocus spending through reducing professional service costs and other discretionary expenses where possible.

- Repairs and maintenance costs decreased by $0.2 million or 59.4% due to some one-time costs incurred last year that were not required this year.

- Travel costs decreased by $0.1 million or 32.1% also due to the refocusing of government spending on discretionary expenses.

OSFI’s total year-to-date expenses of $74.4 million were $3.0 million or 3.9% lower than planned (versus $3.0 million or 4.4% higher than planned for the same period last year). OSFI monitors its performance via monthly reporting and regular forecast exercises.

Chart 1 – Text version

| blank | 2023 | 2024 |

|---|---|---|

| Financial Plan | $68.4 | $77.4 |

| Actual | $71.4 | $74.4 |

Government Funding

In addition to its assessment and cost-recovered services revenues, OSFI was granted a parliamentary appropriation of $1.2 million for the fiscal year ending March 31, 2025 (2024 - $ 1.2 million). During the three months ended June 30, 2024, OSFI recognized $0.3 million (2023 - $0.3 million) of this annual amount.

Risks and Uncertainties

OSFI operates in a constantly changing environment reflected in uncertain economic and financial conditions and an industry that can undergo periods of rapid change and that is becoming increasingly complex. The intensity and pace at which the risk environment is changing requires a reimagining of OSFI’s approach to its risk appetite. OSFI needs a more rigorous and future focussed risk appetite framework that grapples with both identified and other yet-to-be foreseen risks. The risks that exist in such circumstances can have financial consequences, thereby affecting financial statements.

Enterprise Risks

Through its Enterprise Risk Management (ERM) framework and processes, OSFI identifies its key external and internal risksFootnote 1. While OSFI continues to actively address the suite of risks covered by its framework, it also monitors for new ones during each reporting period. As part of the Blueprint for OSFI’s Transformation 2022-25, OSFI has invested additional resources to fortify its risk management capabilities.

External Risks

Some of the more significant external risks are identified below. For a more fulsome narrative of external risks please consult OSFI’s 2024-25 Annual Risk Outlook.

Real estate secured lending and mortgage risks

Of the mortgages outstanding as of February 2024, 76% will be coming up for renewal by the end of 2026. Canadian homeowners who will renew their mortgages during this time period could potentially face a payment shock. This payment shock will be most significant for homeowners who took out mortgages when interest rates were lower in 2020 to 2022. Households that are more heavily leveraged and have mortgages with variable rates but fixed payments will feel this shock more acutely. We expect payment increases to lead to a higher incidence of residential mortgage loans falling into arrears or defaults.

Mortgages that have already experienced payment increases due to renewal or product type, such as adjustable-rate mortgages, are already showing higher rates of non-performance. Should residential real estate markets weaken, this could lead to higher defaults, lower recovery rates, and, therefore, higher credit losses for institutions.

OSFI response

OSFI continuously monitors the risk profiles of institutions’ residential mortgage lending activities and regularly conducts examinations to ensure they follow sound underwriting standards and use prudent lending, portfolio, and account management practices.

In December 2023, we announced that we were maintaining the minimum qualifying rate for uninsured mortgages at the greater of the mortgage contract rate plus 2% or 5.25%. This helps ensure borrowers can still make payments if they experience negative financial shocks, such as a reduction in income, an increase in household expenses, or an increase in mortgage interest rates. Going forward, we will maintain our internal review process to evaluate the calibration of the minimum qualifying rate, with assessments conducted at least annually.

In March 2024, we published a Regulatory Notice that reinforces OSFI’s expectations on sound residential mortgage account and portfolio management practices. Key areas include the need for robust risk monitoring of existing mortgages and proactive engagement with vulnerable borrowers. The Notice also underscores the inherent risks posed by variable rate mortgages with fixed payments and reinforces recent OSFI actions to strengthen risk-based capital requirements in relation to residential real estate exposures, including expectations around provisions for expected credit losses.

Wholesale credit risk

Wholesale credit risk, including risk from commercial real estate (CRE) lending as well as corporate and commercial debt, remains a significant exposure for institutions. Economic uncertainties and changes in these markets are impacting the risk environment. Current interest rate levels have produced challenging refinancing conditions for some commercial and corporate borrowers and the conditions could negatively affect wholesale credit markets in the coming year.

Higher interest rates, inflation, and lower demand have put CRE markets under pressure. We expect these challenges to extend into 2024 and 2025.

The office sub-segment of the CRE market is facing additional changes associated with the move towards hybrid work environments leading to rising vacancies and declining asset values. Lower quality office buildings face more acute risks while higher quality older properties have also experienced pressure from reduced demand for office space.

While office properties face challenges from changes in working environments, other CRE assets also face challenges. The construction market continues to show signs of a slowdown as developers face unfavorable economic conditions. There are also signs that the industrial sector is facing headwinds following a period of strong growth.

OSFI response

OSFI continuously monitors wholesale exposures and lending activities to assess borrower and portfolio vulnerabilities, account management and underwriting practices, and loan loss provisioning.

These efforts will be enhanced by a new loan level data call on CRE exposures at deposit-taking institutions. This data will:

- increase our understanding of the prudential impact of market developments

- allow us to compare risk across institutions and identify higher risk exposures for discussion with institutions

- support our supervision of the expectations outlined in the September 2023 CRE Regulatory Notice

We plan to broaden the scope of the data call to include all wholesale exposures in the future.

OSFI will continue to focus on monitoring institutions' exposures and risk management of wholesale credit risk through regular direct discussions, review of regulatory returns, risk reports, policies, and governance.

Funding and liquidity risks

Liquidity and funding conditions remain sensitive to an uncertain financial market landscape. The expected and actual path of global interest rates will influence the risk appetite of market participants.

Liquidity shocks are a persistent concern and can arise if depositor behaviour shifts dramatically. Intensifying digitalization of the banking environment means that deposit outflows can arise more abruptly and intensely than some market participants expect. Deposit competition has increased over the past year as higher interest rates provide opportunities for depositors and other investors to seek the best possible returns. This has an impact on depositor behaviour and could affect bank deposit persistency and the assumptions deposit-taking institutions make when estimating funding costs. Access to wholesale funding and repo markets remain open, however, at current interest rates. Interest rate changes also impact valuations of high-quality assets held for liquidity at institutions and could reduce the capacity of markets to provide liquidity and contribute to market stability in periods of stress. Changes in depositor behaviour, funding costs and valuations also impact the management of interest rate risk in the banking book.

OSFI response

In 2024, OSFI plans to broaden and intensify its assessment of liquidity risk.

The approach will span key topics, with a focus on intra-day liquidity risk management, and liquidity and interest rate risk in the banking book management effectiveness in material foreign subsidiaries. OSFI will also deepen its line-of-sight into the operational aspects of contingency funding plans to better understand asset monetization decisions during stress events.

Integrity, security, and foreign interference

As the pace of social and political conflict increases globally, so do risks to institutions. A major geopolitical event could disrupt markets and create instability for institutions. The escalation of political tensions and the polarizing effect of geopolitical issues have the potential to make Canadian institutions a target for politically motivated attacks.

We are concerned with threats to institutions’ integrity and security ranging from fraud and money laundering to cyber security and foreign interference. With advances in technology, financial institutions are facing more sophisticated and frequent threats to their security and operational resilience. Geopolitical instability increases the likelihood of risk materializing because geopolitical conflict can motivate hostile foreign nations, affiliated threat actors, or criminals to destabilize our institutions for the purposes of financial gain or the advancement of interests.

Institutions that have integrity and security vulnerabilities, gaps, or issues could be subject to reputational harm, financial risks, or a cyber or national security risk, including foreign interference. These issues could lead to regulatory compliance measures that fall under OSFI’s or the Minister of Finance’s authority.

Given that the financial sector has been identified as one of Canada’s critical infrastructure sectors, and that the institutions OSFI regulates are heavily integrated into the lives of Canadians, we take these threats seriously.

OSFI response

To address these new and growing risks, OSFI has been given an expanded mandate by Parliament, and has established a National Security Sector. This new sector is responsible for helping OSFI ensure that FRFIs address threats from foreign interference and threats to national security that affect federally regulated financial institutions. OSFI also created an Integrity and Security Risk Division to lead integrity and security supervision and policy.

In 2024, OSFI issued an Integrity and Security Guideline with policy and procedure expectations for institutions. OSFI’s guidance aims to help institutions and the Canadian financial system become more resilient to these threats. Institutions also completed an integrity and security questionnaire to assess their alignment with OSFI’s integrity and security expectations. Additionally, we plan to work with institutions to provide them with information on the threat environment.

Public confidence in the Canadian financial system depends on its institutions acting with integrity and securing themselves against diverse threats, including foreign interference. We are building our capacity, and our partnerships with key stakeholders and partners, to leverage existing information and provide advice to monitor the threat environment as it relates to institutions.

Other key risks

It is worth noting the interdependencies that the four ARO risks have on industries we regulate and supervise. For instance, a housing market downturn could cause stress in the mortgage insurance industry. Credit risks and market volatility could impact investment portfolios, asset liability management, and hedging strategies for all insurers.

OSFI considers risks related to deposit-taking institutions, as well as those that are unique to the insurance and pension industries. For example, the impact of a large earthquake and changing weather and flood patterns on the property and casualty industry, as well as changes to life expectancy, impacts both life insurers and pension plans.

OSFI also assesses many other risks posed by cyber and technology, climate, third party outsourcing, and transmission risk from the less-regulated or unregulated financial sector. We continue to monitor the number and severity of disruptive events arising from these risks. These events underscore the importance of operational resilience at institutions and pension plans. The direct costs and, more importantly, the reputational impacts of prolonged disruptions or outages can negatively impact the resilience and stability of an institution and create risk.

Internal Risks

OSFI manages a suite of internal risks that can also affect resources, given the investments needed to mitigate them appropriately. Areas of focus pertain to:

Internal change agenda and organizational change management maturity. OSFI has undergone several significant business changes and adaptations in the areas of technology renewal, organizational re-structuring, and supervisory process reviews. There is a risk that development and delivery of OSFI’s internal change agenda may be detrimental to the effective delivery of its core mandate or its workforce due to change fatigue and diminishing morale. To mitigate this risk, OSFI has developed a 3-year strategic plan that forms the basis for a single, enterprise-wide Operational Plan to guide this transformation. Additionally, extensive efforts have been deployed in the area of change management.

Human resources capacity and capability. OSFI’s success is dependent upon having employees with highly specialized knowledge, skills, and experience to regulate and supervise FIs. There is a risk that OSFI’s human capital may be inadequate to deliver on its mandate due to skill gaps, experience gaps, a lack of technical knowledge to keep pace with FIs’ evolving business models (FinTech), turnover, succession planning/ key person risk, or poor performers. In response to this risk, OSFI is continuing the implementation of its comprehensive Human Capital Strategy. Risks related to employee wellness and resilience have changed as OSFI returns to the Office in a hybrid model.

Financial institution information and data. There is a risk that OSFI may over-rely on information provided by FIs’ management to assess the quality of portfolios or that the FI data collected and OSFI’s management of it are inadequate to effectively deliver on OSFI’s mandate. OSFI has developed an Enterprise Data Management Strategy, which it continues to execute on to respond to this risk.

Protection of Information. OSFI’s information holdings include sensitive and personal information. As such, there is a risk that OSFI’s systems may be inappropriately accessed by external parties or inappropriately used by its employees. To address this risk OSFI is implementing a Cyber Security Strategy and Action Plan while also optimizing the use of existing security technologies.

Financial Risks

Financial risks, primarily liquidity risk and credit risk, are closely managed and continue to be rated low. Please refer to Note 11 to the financial statements for a full analysis of the financial risks to which OSFI is exposed.

Significant Changes in Relation to Operations, Personnel and Programs

There have been no significant changes in relation to Operations, Personnel and Programs during the quarter ended June 30, 2024.

Approval by Senior Officials

Approved by,

Michael Hammond CPA, CGA,

Chief Financial Officer

Peter Routledge,

Superintendent