Small and Medium-Sized Deposit-Taking Institutions (SMSBs) Capital and Liquidity Requirements – Guideline (2026)

Information

Table of contents

Subsections 485(1) and 949(1) of the Bank Act (BA), subsection 473(1) of the Trust and Loan Companies Act (TLCA) require banks (including federal credit unions), bank holding companies, federally regulated trust companies, and federally regulated loan companies to maintain adequate capital and adequate and appropriate forms of liquidity. This Small and Medium-Sized Deposit-Taking Institutions Capital and Liquidity Requirements Guideline (SMSB-CLR) is not made pursuant to subsections 485(2) or 949(2) of the BA, or to subsection 473(2) of the TLCA. However, the capital, leverage and liquidity standards referred to in this guideline, from the requirements set out in the Capital Adequacy Requirements (CAR), Leverage Requirements (LR) and Liquidity Adequacy Requirements (LAR) Guidelines, provide the framework within which the Superintendent assesses whether a bank, a bank holding company, a trust company, or a loan company maintains adequate capital and liquidity pursuant to the Acts. For this purpose, the Superintendent has established the following minimum standards:

- the leverage ratio described in the LR Guideline;

- the risk-based capital ratios described in the CAR GuidelineFootnote 1;

- the Liquidity Coverage Ratio (LCR) described in the LAR Guideline; and,

- the Net Stable Funding Ratio (NSFR) described in the LAR Guideline.

The first measure provides an overall measure of the adequacy of an institution's capital. The second measure focuses on risk faced by the institution. The third and fourth measures – in conjunction with additional liquidity metrics where OSFI reserves the right to apply supervisory requirements as needed, including the net cumulative cash flow (NCCF), the operating cash flow statement (OCFS), the liquidity monitoring tools and the intraday liquidity monitoring tools which, when assessed as a package – provide an overall perspective of the liquidity adequacy of an institution.

Notwithstanding that a bank, bank holding company, trust company, or loan company may meet these standards, the Superintendent may direct a bank or bank holding company to increase its capital or to take actions to improve its liquidity under subsections 485(3) or 949(3) of the BA, or a trust company or a loan company to increase its capital or to take actions to improve its liquidity under subsection 473(3) of the TLCA.

I. Purpose of the Guideline

-

This guideline details the criteria OSFI uses to segment small and medium-sized deposit-taking institutions (SMSBs) into three categories for the purposes of determining capital and liquidity requirements.

-

Capital and liquidity requirements for SMSBs are detailed in the Capital Adequacy Requirements (CAR) Guideline, the Leverage Requirements (LR) Guideline and the Liquidity Adequacy Requirements (LAR) Guideline, which are referenced throughout. This guideline is a reference tool for SMSBs to clarify which parts of the CAR, LR and LAR are applicable to SMSBs in their category.

II. Scope of Application

-

For the purposes of this guideline, SMSBs are banks (including federal credit unions), bank holding companies, federally regulated trust companies, and federally regulated loan companies that have not been designated by OSFI as domestic systemically important banks (D-SIBs). This includes subsidiaries of SMSBs or D-SIBs that are banks (including federal credit unions), federally regulated trust companies or federally regulated loan companies.

-

The segmentation, capital and liquidity requirements referenced in this guideline apply to SMSBs on a consolidated basis.

III. Segmentation of SMSBs

-

SMSBs are segmented into three categories for the purposes of their capital and liquidity requirements based on the general criteria, as follows:

- SMSBs reporting more than $10 billionFootnote 2 in total assets are in Category I

- SMSBs reporting less than $10 billion in total assets are in Category II if they meet any of the following criteria:

- report greater than $100 million in total loans

- enter into interest rate or foreign exchange derivatives with a combined notional amount greater than 100% of total capital

- have any other types of derivative exposure

- have exposure to other off-balance sheet items greater than 100% of total capital Footnote 3

- SMSBs reporting less than $10 billion in total assets that do not meet any of the criteria in 5(b) above are in Category III. SMSBs that do not meet any of the criteria in 5(b) may also request to OSFI to be in Category II. Any such request must be made in writing, and explain why the Category III capital and liquidity requirements are not appropriate for the nature of their institution's activitiesFootnote 4. Institutions must make such a request prior to the implementation of this guideline, or in the case of new SMSBs, prior to the making of an Order to Commence and Carry on Business.

-

Subsidiaries of SMSBs are subject to the same capital and liquidity requirements as their parent institution. Provided the criteria outlined in the exemption of section 1.2 of the LAR Guideline are met, some subsidiaries of SMSBs may be exempted from adhering to minimum liquidity requirements.

-

Subsidiaries of D-SIBs are considered to be in Category I for the purposes of capital and liquidity requirements.

-

Notwithstanding the general criteria in paragraph 5, OSFI has the discretion to move an institution into a different categoryFootnote 4. Factors OSFI may consider include:

- Changes in an institution's activities that may not yet be reflected in its balance sheet; and,

- An institution's business model, where its category, based on the general criteria above, would result in capital or liquidity requirements that do not appropriately reflect the nature of its activities.

OSFI will notify any institutions that are moved into a category different from the general criteria in paragraph 5, including the time period in which the institution must meet the requirements of its new category.

-

New SMSBs will be categorized based on the planned activities and balance sheet in the institution's business plan. The categorization will be confirmed at the time the Superintendent issues an Order to Commence and Carry on Business.

-

For the purposes of SMSB segmentation, institutions must calculate average total assets and total loans at the end of each fiscal year based on the amount reported in OSFI's M4 monthly Balance Sheet return for each of the previous 12 months. If an institution crosses either the $10 billion total assets or $100 million total loans thresholds, they must notify OSFI within 60 days of their fiscal year end, and after confirmation by OSFI, would be subject to the requirements of their new category the following fiscal year. If, after a minimum of two fiscal years in a category, an institution once again crosses a segmentation threshold for total assets or total loans, the institution must notify OSFI and would, after confirmation by OSFI, be subject to the requirements of their new category the following fiscal year.

The following example illustrates how asset or loan thresholds for segmentation would operate in practice. The example focuses on the migration between Categories III and II, however the process would be the same with the $10 billion total asset threshold to move between Categories II and I.

An institution with a December fiscal year end initially has $90 million in total loans and is therefore in Category III.

In January 2024 the total loans threshold is assessed using fiscal 2023 data and average total loans, using the 12 month-end balances from fiscal 2023, is above $100 million. The institution must inform OSFI that it has crossed the threshold by March 1, 2024 and, subject to OSFI confirmation, would need to meet the capital and liquidity requirements for Category II for at least two years, starting in Q1 2025.

In January 2026, the 12-month average calculation is performed again using the 12 month-end balances from fiscal 2025 and the average total loans is below the $100 million threshold. The institution would then need to inform OSFI that it has crossed the threshold before March 1, 2026, and, subject to OSFI confirmation, would need to meet the capital and liquidity requirements for Category III starting in Q1 2027.

-

Category III SMSBs must also notify OSFI within 60 days of a fiscal quarter end if they had derivative or other off-balance sheet exposures in excess of the thresholds in paragraph 5(b) (ii), (iii) or (iv) at any point during the quarter. After confirmation from OSFI that the institution no longer meets the criteria for Category III, the institution would then be subject to the requirements of Category II after four fiscal quarters. During this period, OSFI may request an institution that has crossed the derivative and/or off-balance sheet thresholds to track, and regularly report on the notional amount, and exposures, from these activities. An institution that has crossed the derivative or off-balance sheet thresholds must remain in Category II for a minimum of two years. If the institution remains below the thresholds in paragraph 5(b) (ii), (iii) and (iv) for a minimum of two years, the institution must notify OSFI and would, after confirmation by OSFI, be subject to the requirements of Category III after four fiscal quarters.

The following example illustrates how the derivative and other off-balance sheet exposure thresholds for segmentation would operate in practice.

An institution with a December fiscal year end initially has no derivative exposure and is therefore in Category III.

In February 2024, the institution completes an F/X derivatives trade with a notional value of $15 million, which is greater than the amount of the institution's total capital. The institution must inform OSFI, no later than May 31, 2024 (60 days after the fiscal quarter end). The institution would, subject to OSFI confirmation, then be subject to the Category II capital and liquidity requirements starting in fiscal Q2 2025. The institution remains in Category II until at least Q2 2027.

The institution closes all of its derivative exposure in Q4 2025. For the next two years, the institution has no derivative or other off-balance sheet exposures. In Q1 2028, the institution informs OSFI that is has remained below the thresholds in paragraph 5(b) (ii), (iii) or (iv) for two years. After written confirmation from OSFI, the institution becomes subject to the Category III requirements again starting in fiscal 2029.

IV. Category I SMSBs – Capital and Liquidity Requirements

4.1 Risk-Based Capital Requirements

4.1.1 Overview of Risk-Based Capital Requirements and Definition of Capital

-

Chapter 1 of the CAR Guideline explains how to calculate risk-based capital ratios and the minimum and target ratios.

- The minimum risk-based capital ratios for Category I SMSBs are in CAR Chapter 1, section 1.6.1.

- Category I SMSBs are also subject to the capital conservation buffer in CAR Chapter 1, section 1.7.1.

- The capital targets for Category 1 SMSBs are summarized in CAR Chapter 1, section 1.10.

- The countercyclical buffer (CAR Chapter 1, section 1.7.2) may also be applicable to Category I institutionsFootnote 5. OSFI will inform SMSBs whenever the countercyclical buffer has been deployed in Canada and must be applied to domestic exposures. Category I institutions must also apply the countercyclical buffer for any international exposures where the countercyclical buffer has been deployed by the local regulator.

- The D-SIB Surcharge and the Domestic Stability Buffer described in Chapter 1 of the CAR Guideline are not applicable to Category I SMSBs.

- Annex 1 of Chapter 1 of the CAR Guideline (Domestic Systemic Importance and Capital Targets) is not applicable to Category I SMSBs.

-

Category I SMSBs are eligible to apply to use the Internal Ratings Based (IRB) approach for credit risk, as detailed in section 1.4.1 in Chapter 1 of the CAR. CAR Chapter 1, sections 1.4 and 1.5, which describe the Capital Floor, are only applicable to Category I SMSBs that have been approved by OSFI to use the IRB approach.

-

Chapter 2 of the CAR Guideline defines the tiers of capital used in the calculation of the risk-based capital ratios, as well as required adjustments to each tier of capital.

4.1.2 Operational Risk

-

Chapter 3 of the CAR Guideline details how to calculate operational risk capital requirements using either the Simplified Standardized or Standardized Approach.

-

Category I SMSBs with an annual Adjusted Gross IncomeFootnote 6 greater than $1.5 billion must use the Standardized Approach (see CAR Chapter 3, section 3.2 and section 3.4).

-

Category I SMSBs with an annual Adjusted Gross Income less than $1.5 billion are also eligible to apply to use the Standardized Approach, if they meet the criteria detailed in section 3.2 of the CAR Guideline.

-

Unless approved by OSFI to use the Standardized Approach, Category I SMSBs with an annual Adjusted Gross Income less than $1.5 billion must use the Simplified Standardized Approach (section 3.3 of CAR Chapter 3). For these institutions, CAR Chapter 3, section 3.4 (Standardized Approach) is not applicable.

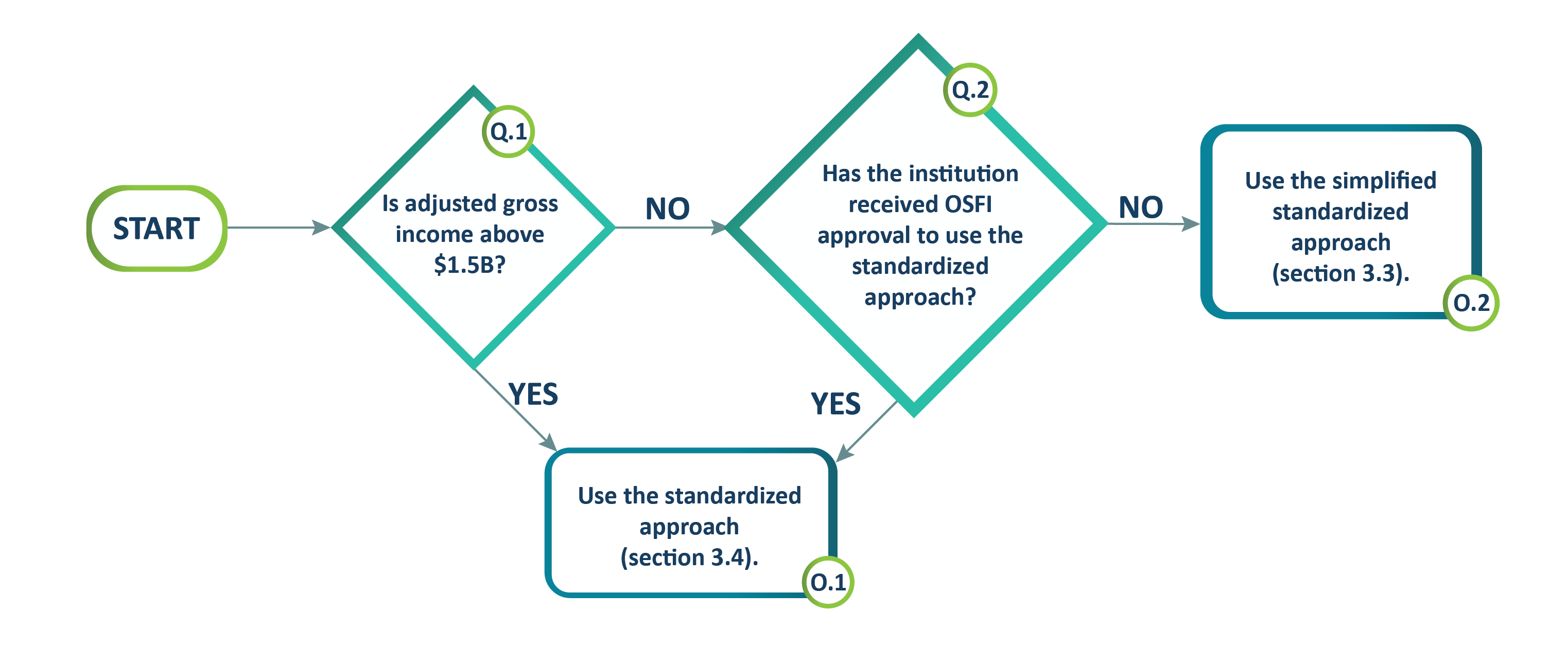

Text Description - Chart 1

Start:

Question 1: Is adjusted gross income above $1.5B?

- If yes, proceed to Output 1.

- If no, proceed to Question 2.

Question 2: Has the institution received OSFI approval to use the standardized approach?

Output 1: Use the standardized approach (section 3.4).

- END.

Output 2: Use the simplified standardized approach (section 3.3).

- END.

4.1.3 Credit Risk

-

The following section provides information related to the credit risk requirements for Category I SMSBs, broken down by the following exposure types:

- Banking Book;

- Securitization; and,

- Exposures with Counterparty Credit Risk.

Banking Book Exposures

-

Risk-weighted assets (RWA) for banking book exposures, with the exception of certain securitizations, exposures with counterparty credit risk and CVA exposures, are calculated using either the Standardized or IRB approach.

- Chapter 5 of the CAR Guideline details the IRB approach to calculating credit risk capital. This chapter is only applicable to those Category I SMSBs that have received OSFI approval to use the IRB approach.

- Chapter 4 of the CAR Guideline details how to calculate credit risk capital using the Standardized Approach. This chapter is applicable to all Category I SMSBs. Category I SMSBs are eligible to apply a simplified treatment to the asset class groupings listed in Appendix I of Chapter 4 of the CAR Guideline, provided the total exposure to the asset class grouping does not exceed $500 million.

-

Category I SMSBs may reflect eligible guarantees or credit derivatives designed to mitigate credit risk for banking book exposures in the calculation of RWA using either:

- the IRB approach, if an institution has approval to use the IRB approach for both the original exposure and the guarantor. The recognition of guarantees and credit derivatives under the IRB approach is detailed in section 5.4 of Chapter 5 of the CAR Guideline; or,

- the Standardized Approach, as detailed in section 4.3 of Chapter 4 of the CAR Guideline, for all other guarantees and credit derivatives.

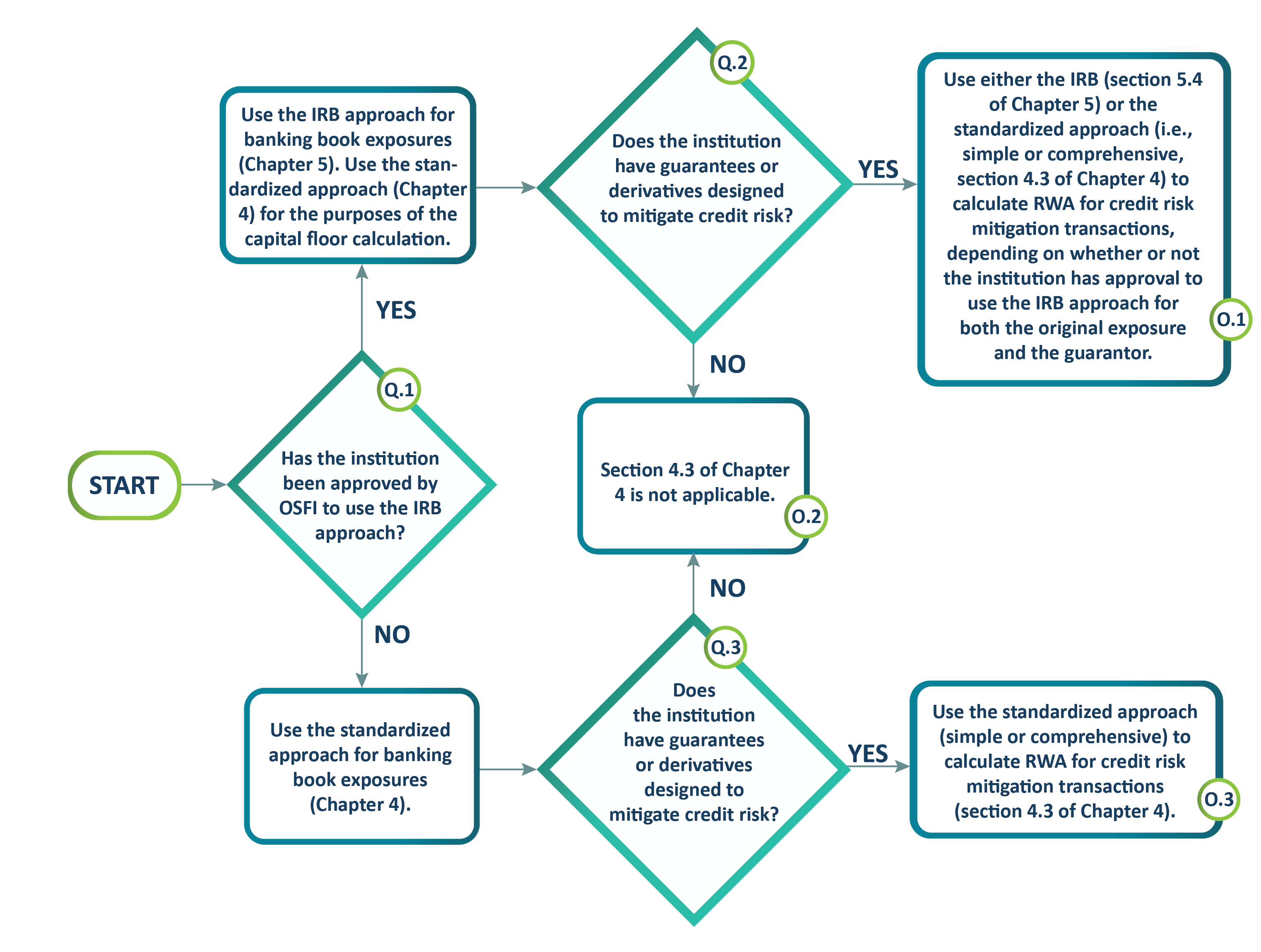

Text Description - Chart 2

Start:

Question 1: Has the institution been approved by OSFI to use the IRB approach?

- If yes, use the IRB approach for banking book exposures (Chapter 5). Use the standardized approach (Chapter 4) for the purposes of the capital floor calculation. Proceed to Question 2.

- If no, use the standardized approach for banking book exposures (Chapter 4). Proceed to Question 3.

Question 2: Does the institution have guarantees or derivatives designed to mitigate credit risk?

Question 3: Does the institution have guarantees or derivatives designed to mitigate credit risk?

Output 1: Use either the IRB (section 5.4 of Chapter 5) or the standardized approach (i.e., simple or comprehensive, section 4.3 of Chapter 4) to calculate RWA for credit risk mitigation transactions, depending on whether or not the institution has approval to use the IRB approach for both the original exposure and the guarantor.

- END.

Output 2: Section 4.3 of Chapter 4 is not applicable.

- END.

Output 3: Use the standardized approach (simple or comprehensive) to calculate RWA for credit risk mitigation transactions (section 4.3 of Chapter 4).

- END.

Securitization Exposures

-

Chapter 6 of the CAR Guideline details how to calculate RWA for securitization exposures. This chapter is only applicable for Category I SMSBs if they have securitization exposures that involve tranching, with associated subordination of credit risk, as defined in paragraph 3 and section 6.1 of Chapter 6 of the CAR GuidelineFootnote 7.

- Securitization exposures can include, but are not restricted to, the following: asset-backed securities, mortgage-backed securities, credit enhancements, liquidity facilities, loans to securitization vehicles to fund the acquisition of assets, interest rate or currency swaps, credit derivatives and tranched coverFootnote 8.

-

In order to apply the securitization treatment in Chapter 6 for exposures originated by the institution (e.g. assets sold into a securitization structure), the operational requirements for risk transference detailed in section 6.3 must be metFootnote 9. If these requirements are not met, institutions must risk weight the assets underlying the securitization as if they had not been securitized.

-

When calculating RWA for each securitization exposure, institutions must follow the hierarchy of approaches outlined in section 6.5.2 of Chapter 6 of the CAR Guideline. The terms used in the descriptions of the approaches are defined in section 6.2 of CAR Chapter 6.

- The Securitization Internal Ratings-Based Approach (SEC-IRBA, section 6.6.1 in Chapter 6 of the CAR Guideline) and the Internal Assessment Approach (SEC-IAA, section 6.6.3 in Chapter 6 of the CAR Guideline) are only applicable to Category I SMSBs that have received OSFI approval to use IRB approaches for the relevant assets in these securitization structures.

- Category I institutions that have not received OSFI approval to use IRB approaches for the relevant assets must use either the External Ratings-Based Approach (SEC-ERBA, section 6.6.2 in Chapter 6 of the CAR Guideline) or the standardized approach (SEC-SA, section 6.6.4 in Chapter 6 of the CAR Guideline).

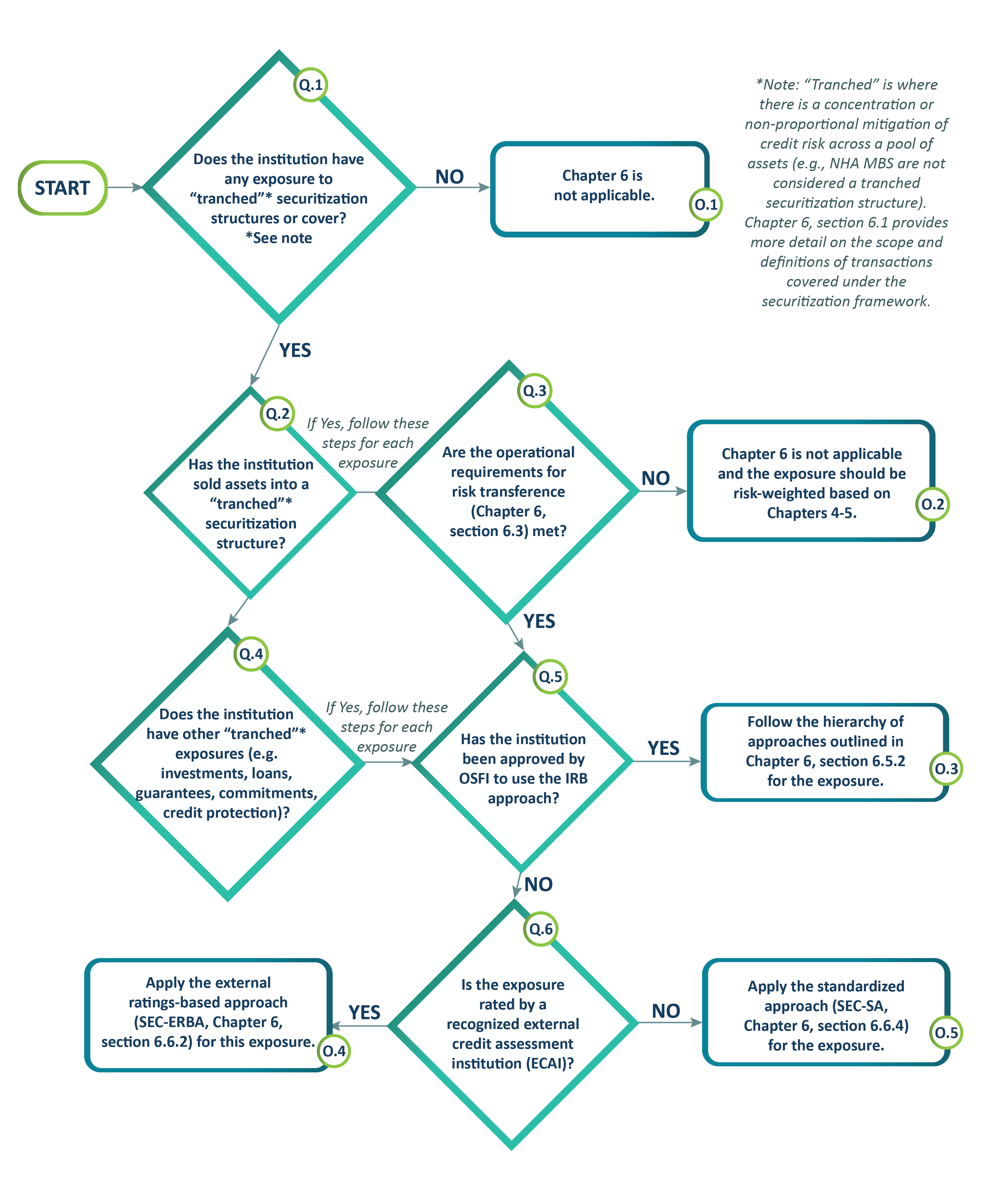

Text Description - Chart 3

Start:

Question 1: Does the institution have any exposure to "tranched"Footnote * securitization structures or cover?

- If yes, proceed to Question 2.

- If no, proceed to Output 1.

Question 2: Has the institution sold assets into a "tranched"Footnote * securitization structure?

- If yes, follow these steps for each exposure. Proceed to Question 3.

- If no, proceed to Question 4.

Output 1: Chapter 6 is not applicable.

- END.

Question 3: Are the operational requirements for risk transference (Chapter 6, section 6.3) met?

- If yes, proceed to Question 5.

- If no, proceed to Output 2.

Question 4: Does the institution have other "tranched"Footnote * exposures (e.g. investments, loans, guarantees, commitments, credit protection)?

- If yes, follow these steps for each exposure. Proceed to Question 5.

- If no, END.

Question 5: Has the institution been approved by OSFI to use the IRB approach?

- If yes, proceed to Output 3.

- If no, proceed to Question 6.

Output 2: Chapter 6 is not applicable and the exposure should be risk-weighted based on Chapters 4-5.

- END.

Output 3: Follow the hierarchy of approaches outlined in Chapter 6, section 6.5.2 for the exposure.

- END.

Question 6: Is the exposure rated by a recognized external credit assessment institution (ECAI)?

Output 4: Apply the external ratings-based approach (SEC-ERBA, Chapter 6, section 6.6.2) for this exposure.

- END.

Output 5: Apply the standardized approach (SEC-SA, Chapter 6, section 6.6.4) for the exposure.

- END.

Counterparty Credit Risk

-

Category I SMSBs with exposures to instruments with counterparty credit risk must also calculate a capital charge for counterparty credit risk for these exposures. Exposures with counterparty credit risk, as detailed in CAR Chapter 7, section 7.1.2, are:

- Over the counter (OTC) Derivatives;

- Exchange-traded derivatives (ETDs);

- Long Settlement transactions; and,

- Securities Financing Transactions (SFTs).

-

The following approaches should be used for counterparty credit risk exposure, unless the institution has approval from OSFI to use an Internal Model Method (IMM):

- For derivative and long settlement transaction exposures:

- the standardized approach for counterparty credit risk (SA-CCR), detailed in Chapter 7, section 7.1.7 of the CAR Guideline, should be used to calculate exposure or exposure at default (EAD); and

- Chapter 4 or 5 of the CAR Guideline should be used to determine the applicable risk-weight, depending on whether or not the institution has been approved to use IRB models for the exposure.

- For SFT exposures:

- the simple or comprehensive approach (detailed in CAR Chapter 4, section 4.3.3), or the VaR modelFootnote 10 approach for collateralized transactions, should be used to calculate exposure or EAD; and,

- Chapter 4 or 5 of the CAR Guideline should be used to determine the applicable risk-weight, depending on whether or not the institution has been approved to use IRB models for the exposure.

- For derivative and long settlement transaction exposures:

-

Only those Category I SMSBs that are required by OSFI to apply the market risk framework are eligible to apply to use an IMM for counterparty credit risk, as detailed in CAR Chapter 7, section 7.1.4. These institutions can apply to OSFI to use IMM for either derivative or SFT exposures (or both). CAR Chapter 7, section 7.1.5, details how to measure exposure and capital requirements using IMM.

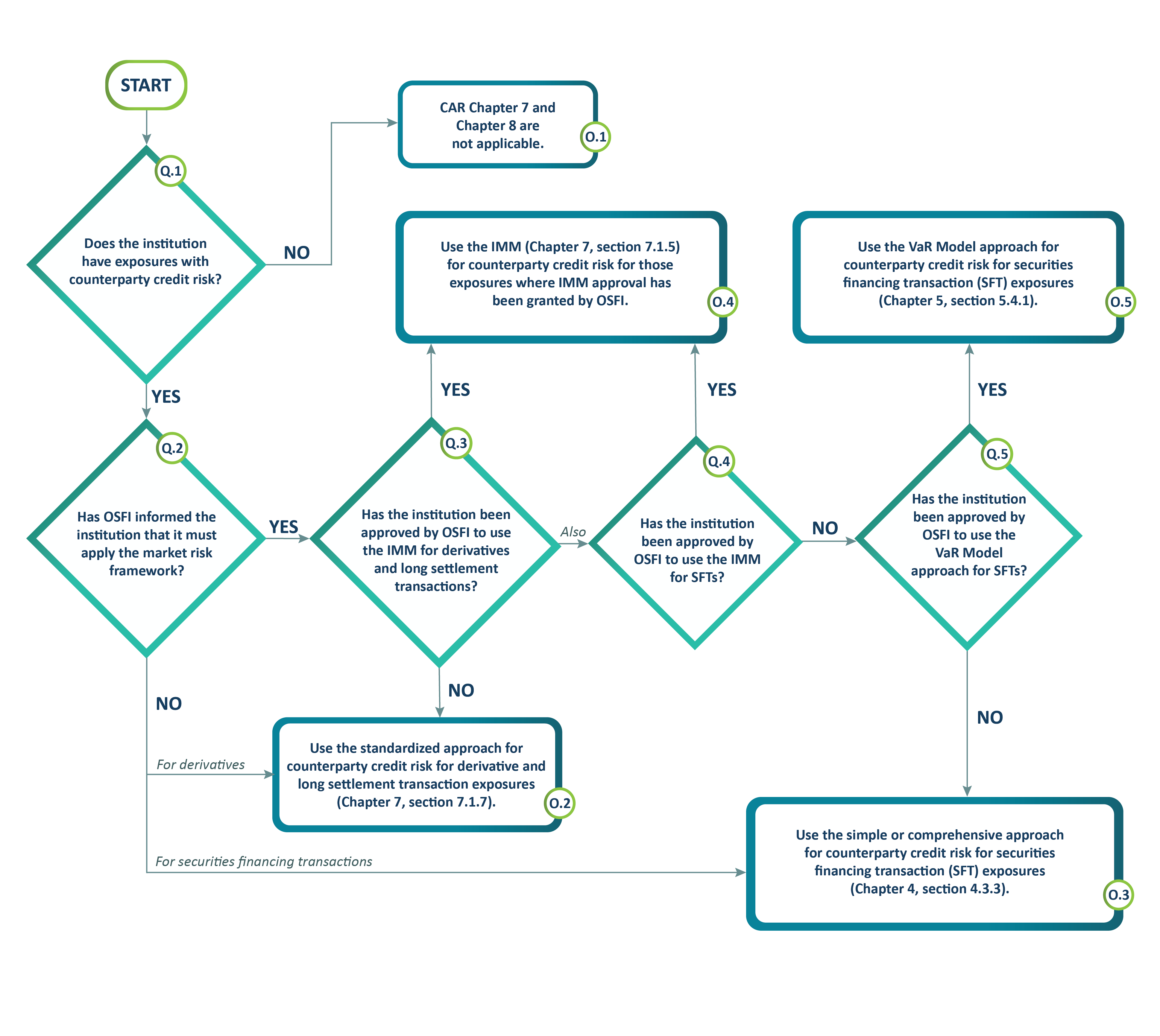

Text Description - Chart 4

Start:

Question 1: Does the institution have exposures with counterparty credit risk?

- If yes, proceed to Question 2.

- If no, proceed to Output 1.

Question 2: Has OSFI informed the institution that it must apply the market risk framework?

- If yes, for derivatives proceed to Question 3 or for securities financing transactions proceed to Question 4.

- If no, for derivatives proceed to Output 2 or for securities financing transactions proceed to Output 3.

Output 1: CAR Chapter 7 and Chapter 8 are not applicable.

- END.

Question 3: Has the institution been approved by OSFI to use IMM for derivatives and long settlement transactions?

Question 4: Has the institution been approved by OSFI to use the IMM for SFTs?

- If yes, proceed to Output 4.

- If no, proceed to Question 5.

Output 2: Use the standardized approach for counterparty credit risk for derivative and long settlement transaction exposures (Chapter 7, section 7.1.7).

- END.

Output 3: Use the simple or comprehensive approach for counterparty credit risk for securities financing transaction (SFT) exposures (Chapter 4, section 4.3.3).

- END.

Output 4: Use the IMM (Chapter 7, section 7.1.5) for counterparty credit risk for those exposures where IMM approval has been granted by OSFI.

- END.

Question 5: Has the institution been approved by OSFI to use the VaR Model approach for SFTs?

Output 5: Use the VaR Model approach for counterparty credit risk for securities financing transaction (SFT) exposures (Chapter 5, section 5.4.1).

- END.

-

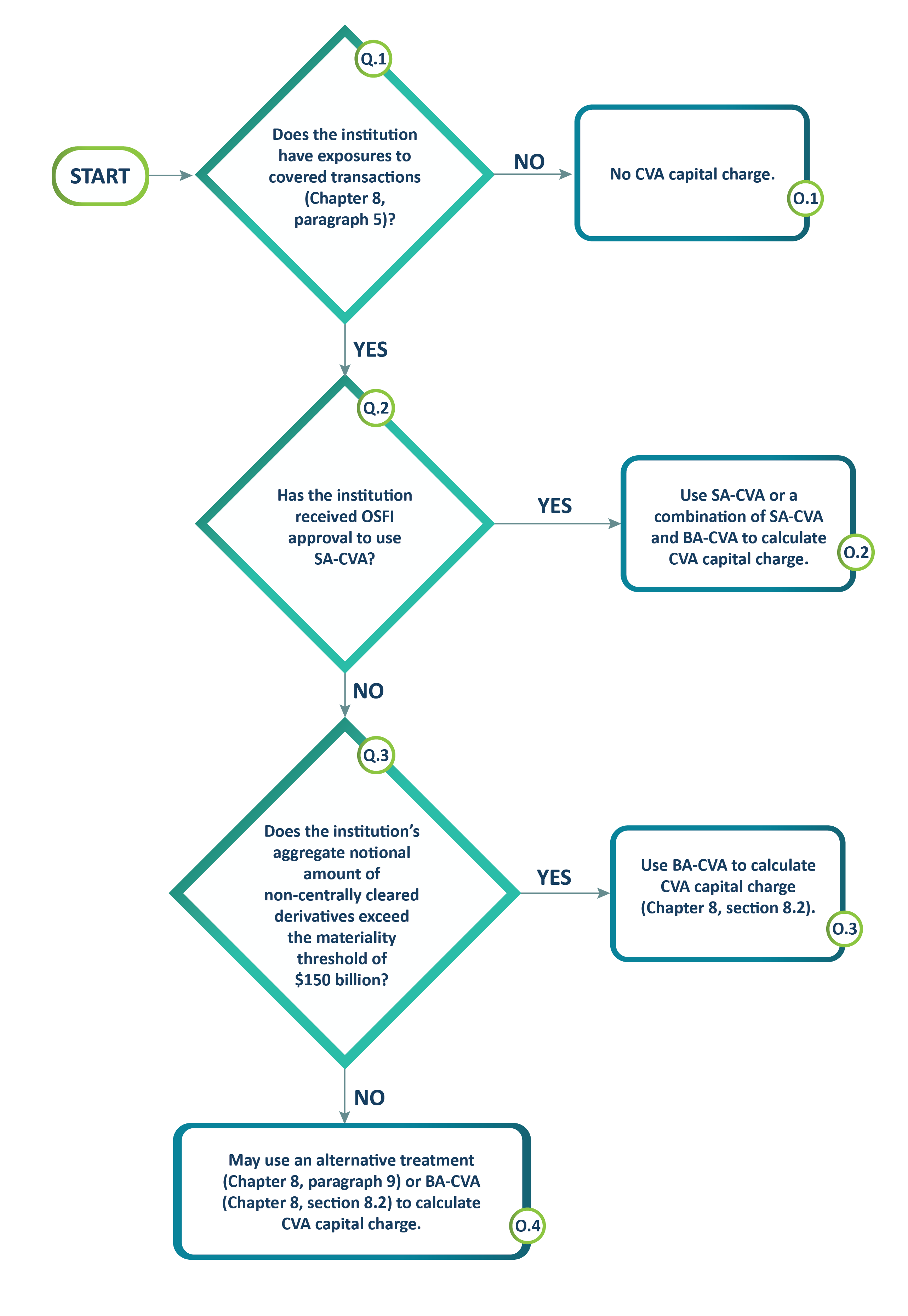

Category I SMSBs are also subject to capital requirements for credit valuation adjustment risk (CVA, see Chapter 8 of the CAR Guideline) to cover the risk of mark-to-market losses on the expected counterparty risk for each of the following types of exposures:

- Over the counter (OTC) instruments with counterparty credit risk (e.g. OTC derivatives)Footnote 11; and

- Securities financing transactions (SFT), if OSFI has notified the institution that it has determined that the institution's CVA loss exposures arising from SFT transactions are material.

-

Chapter 8 of the CAR Guideline is not applicable for Category I SMSBs that do not have either of the two types of exposures in paragraph 28Footnote 12.

Text Description - Chart 5

Start:

Question 1: Does the institution have exposures to covered transactions (Chapter 8, paragraph 6)?

- If yes, proceed to Question 2.

- If no, proceed to Output 1.

Question 2: Has the institution received OSFI approval to use SA-CVA?

- If yes, proceed to Output 2.

- If no, proceed to Question 3.

Output 1: No CVA capital charge.

- END.

Output 2: Use SA-CVA or a combination of SA-CVA and BA-CVA to calculate CVA capital charge.

- END.

Question 3: Does the institution's aggregate notional amount of non-centrally cleared derivatives exceed the materiality threshold of $150 billion?

Output 3: Use BA-CVA to calculate CVA capital charge (Chapter 8, section 8.2).

- END.

Output 4: May use an alternative treatment (Chapter 8, paragraph 10) or BA-CVA (Chapter 8, section 8.2) to calculate CVA capital charge.

- END.

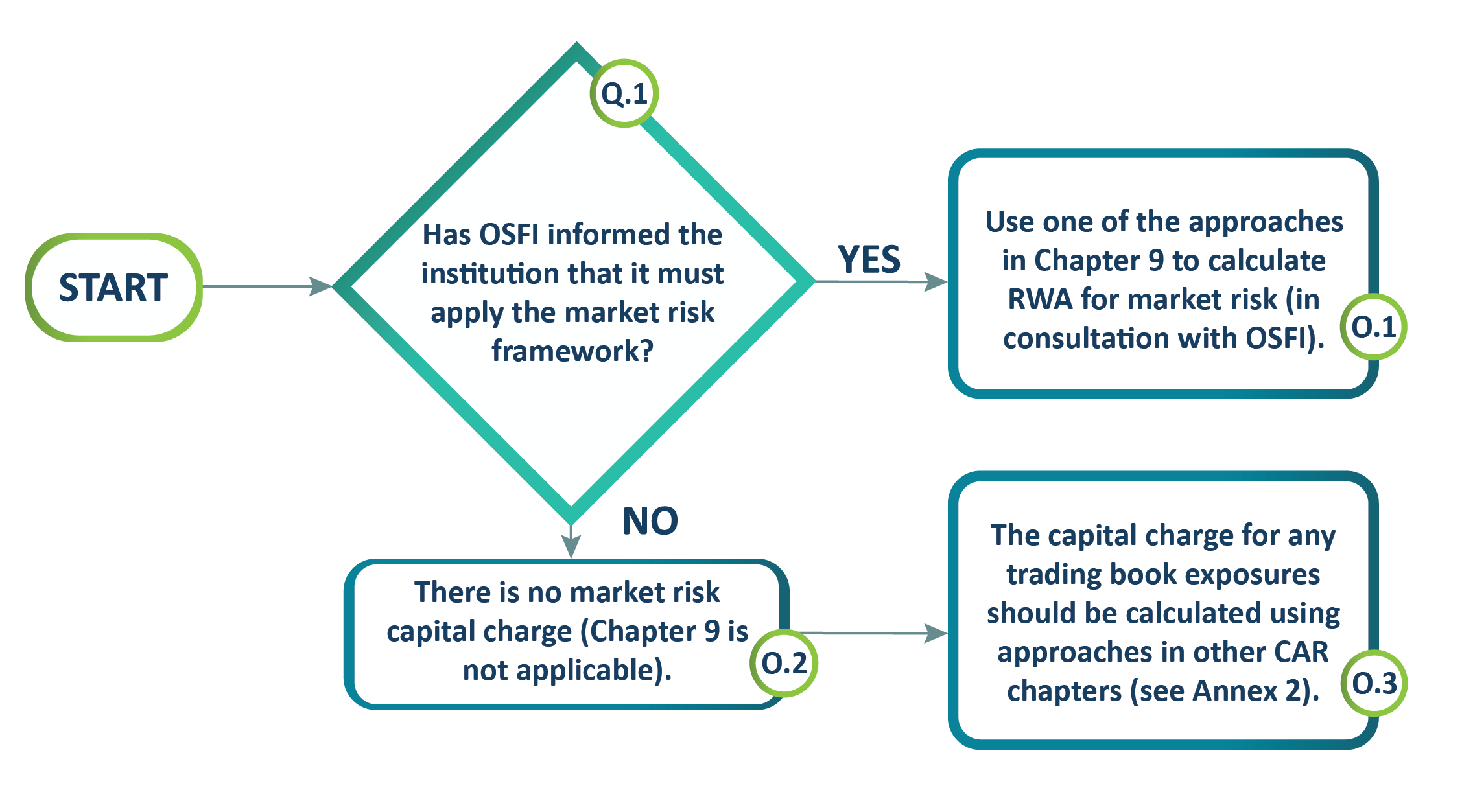

4.1.4 Market Risk and Trading Book Exposures

-

Category I SMSBs will be informed by OSFI if the market risk framework is applicable to their institution. These institutions should use one of the approaches detailed in Chapter 9 of the CAR Guideline to calculate RWA for market risk, in consultation with OSFI.

-

All other Category I SMSBs, for whom the market risk framework is not applicable, should include any trading book exposures in the calculation of RWA using the approaches detailed in other chapters of the CAR GuidelineFootnote 13. For these institutions, Chapter 9 of the CAR Guideline is not applicable.

Text Description - Chart 6

Start:

Question 1: Has OSFI informed the institution that it must apply the market risk framework?

Output 1: Use one of the approaches in Chapter 9 to calculate RWA for market risk (in consultation with OSFI).

- END.

Output 2: There is no market risk capital charge (Chapter 9 is not applicable).

- Proceed to Output 3.

Output 3: The capital charge for any trading book exposures should be calculated using approaches in other CAR chapters (see Annex 2).

- END.

4.2 Leverage Requirements

-

The LR Guideline outlines the leverage requirements for Category I SMSBs, including minimum and authorized leverage ratios. Category I SMSBs are not subject to the leverage ratio buffer described in section IV of the LR Guideline.

4.3 Liquidity Requirements

-

Chapter 1 of the LAR Guideline provides an overview of the liquidity adequacy requirements. Category I SMSBs are subject to all of the liquidity metrics detailed in section 1.3 of the LAR Guideline, with the following exceptions:

- Only those Category I SMSBs with a significant level of wholesale funding are subject to a minimum Net Stable Funding Ratio (NSFR) requirement (see paragraph 36 below).

- Category I SMSBs are not subject to any requirements related to the Operating Cash Flow Statement (OCFS) (LAR Chapter 5).

- Category I SMSBs are only subject to the intraday liquidity monitoring tools (LAR Chapter 7) if they are direct clearers.

-

OSFI generally considers the liquidity adequacy of subsidiaries of SMSBs in the context of the consolidated parent entity. Therefore, subsidiaries of Category I SMSBs may be exempted from the minimum liquidity requirements in the LAR, provided they meet the criteria in section 1.2 of the LAR Guideline. Subsidiaries of D-SIBs are subject to the same liquidity adequacy requirements as Category I SMSBs, with the exception of:

- The NSFR (see paragraph 36); and,

- The NCCF, provided they meet the criteria in the LAR (Chapter 1, paragraph 4).

-

All Category I SMSBs are subject to the requirements of the Liquidity Coverage Ratio (LCR), detailed in Chapter 2 of the LAR Guideline.

-

The Net Stable Funding Ratio (NSFR), detailed in Chapter 3 of the LAR Guideline, is only applicable to Category I SMSBs with significant reliance on wholesale funding, defined as funding 40% or more of their total on-balance sheet assets with wholesale funding sources, as detailed in Chapter 3, Annex 1 of the LAR. Note that the NSFR is only a requirement for the consolidated parent entity in Canada that is regulated by OSFI, therefore subsidiaries of D-SIBs and subsidiaries of SMSBs are not subject to separate NSFR requirements.

The following examples illustrate when the NSFR would, or would not, be applicable:

Example #1: A Category I SMSB is a subsidiary of another financial institution outside Canada. This SMSB would be subject to the NSFR requirement if its wholesale funding levels exceed the 40% threshold.

Example #2: A federally-regulated trust company in Canada is a subsidiary of a D-SIB. This SMSB would not be subject to the NSFR.

Example #3: A Category I SMSB is a subsidiary of a provincially-regulated credit union. This SMSB would be subject to the NSFR requirement if its wholesale funding levels exceed the 40% threshold.

-

Chapter 4 of the LAR Guideline details the Net Cumulative Cash Flow (NCCF) metric and related requirements. Category I SMSBs are subject to the Comprehensive NCCF. The Streamlined NCCF is not applicable to Category I SMSBs.

-

The Operating Cash Flow Statement (OCFS) detailed in Chapter 5 of the LAR Guideline is not applicable to Category I SMSBs.

-

Chapter 6 of the LAR Guideline details several other liquidity monitoring tools applicable to Category I SMSBs that should be used to assess their liquidity adequacy.

-

Chapter 7 of the LAR Guideline (Intraday Liquidity Monitoring Tools) covers intraday liquidity monitoring tools applicable to Category I SMSBs. However, they are only subject to the regulatory reporting requirements outlined in Chapter 7 if they are direct clearers of Lynx.

V. Category II SMSBs – Capital and Liquidity Requirements

5.1 Risk-Based Capital Requirements

5.1.1 Overview of Risk-Based Capital Requirements and Definition of Capital

-

Chapter 1 of the CAR Guideline explains how to calculate risk-based capital ratios and sets out the minimum and target ratios.

- The minimum risk-based capital ratios for Category II SMSBs are in CAR Chapter 1, section 1.6.1.

- Category II SMSBs are also subject to the capital conservation buffer in CAR Chapter 1, section 1.7.1.

- The capital targets for Category II SMSBs are summarized in CAR Chapter 1, section 1.10.

- The countercyclical buffer (CAR Chapter 1, section 1.7.2) may also be applicable to Category II institutionsFootnote 14. OSFI will inform SMSBs whenever the countercyclical buffer has been deployed in Canada, and must be applied to domestic exposures. Category II institutions must also apply the countercyclical buffer for any international exposures where the countercyclical buffer has been deployed by the local regulator.

- The D-SIB Surcharge and the Domestic Stability Buffer described in Chapter 1 of the CAR Guideline are not applicable to Category II SMSBs.

- Annex 1 of Chapter 1 of the CAR Guideline (Domestic Systemic Importance and Capital Targets) is not applicable to Category II SMSBs.

-

Category II SMSBs are not eligible to apply to use the Internal Ratings Based (IRB) approach for credit risk, therefore sections 1.4 and 1.5 of Chapter 1 of the CAR Guideline are not applicable to these institutions.

-

Chapter 2 of the CAR Guideline defines the tiers of capital used in the calculation of the risk-based capital ratios, as well as required adjustments to each tier of capital.

5.1.2 Operational Risk

-

Chapter 3 of the CAR Guideline details how to calculate operational risk capital. Category II SMSBs must use the Simplified Standardized Approach, therefore CAR Chapter 3, section 3.4 (Standardized Approach) is not applicable.

5.1.3 Credit Risk

-

The following section provides information related to the credit risk requirements for Category II SMSBs, broken down by the following exposure types:

- Banking Book;

- Securitization; and,

- Exposures with Counterparty Credit Risk.

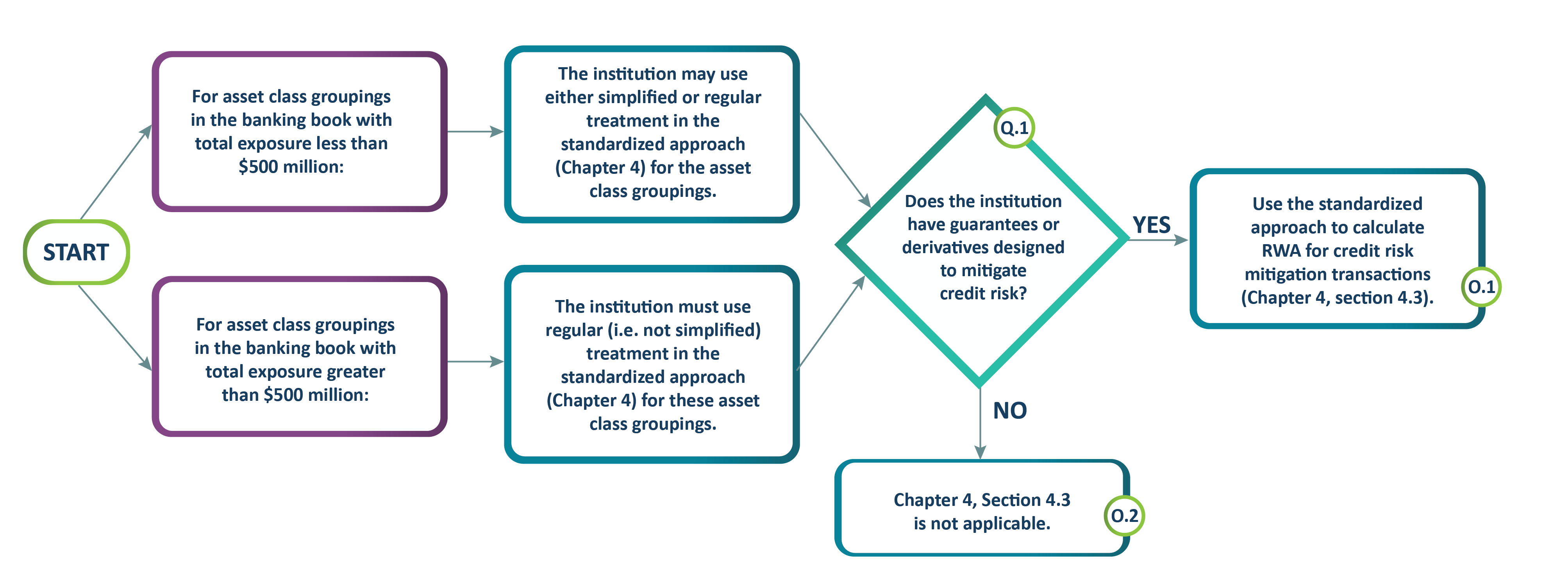

Banking Book Exposures

-

RWA for banking book exposures, with the exception of certain securitizations, exposures with counterparty credit risk and CVA exposures, are calculated using the Standardized Approach (detailed in Chapter 4 of the CAR Guideline). Category II SMSBs are eligible to apply a simplified treatment to the asset class groupings listed in Appendix I of Chapter 4 of the CAR Guideline, provided the total exposure to the asset class grouping does not exceed $500 million.

-

Category II SMSBs may reflect eligible guarantees or credit derivatives designed to mitigate credit risk for banking book exposures in the calculation of RWA using the Standardized Approach, as detailed in section 4.3 of Chapter 4 of the CAR Guideline.

-

Chapter 5 of the CAR Guideline is not applicable to Category II SMSBs.

Text Description - Chart 7

Start:

- For asset class groupings in the banking book with total exposure less than $500 million: the institution may use either simplified or regular treatment in the standardized approach (Chapter 4) for the asset class groupings. Proceed to Question 1.

- For asset class groupings in banking book with total exposure greater than $500 million: the institution must use regular (i.e. not simplified) treatment in the standardized approach (Chapter 4) for these asset class groupings. Proceed to Question 1.

Question 1: Does the institution have guarantees or derivatives designed to mitigate credit risk?

Output 1: Use the standardized approach to calculate RWA for credit risk mitigation transactions (Chapter 4, section 4.3).

- END.

Output 2: Chapter 4, Section 4.3 is not applicable.

- END.

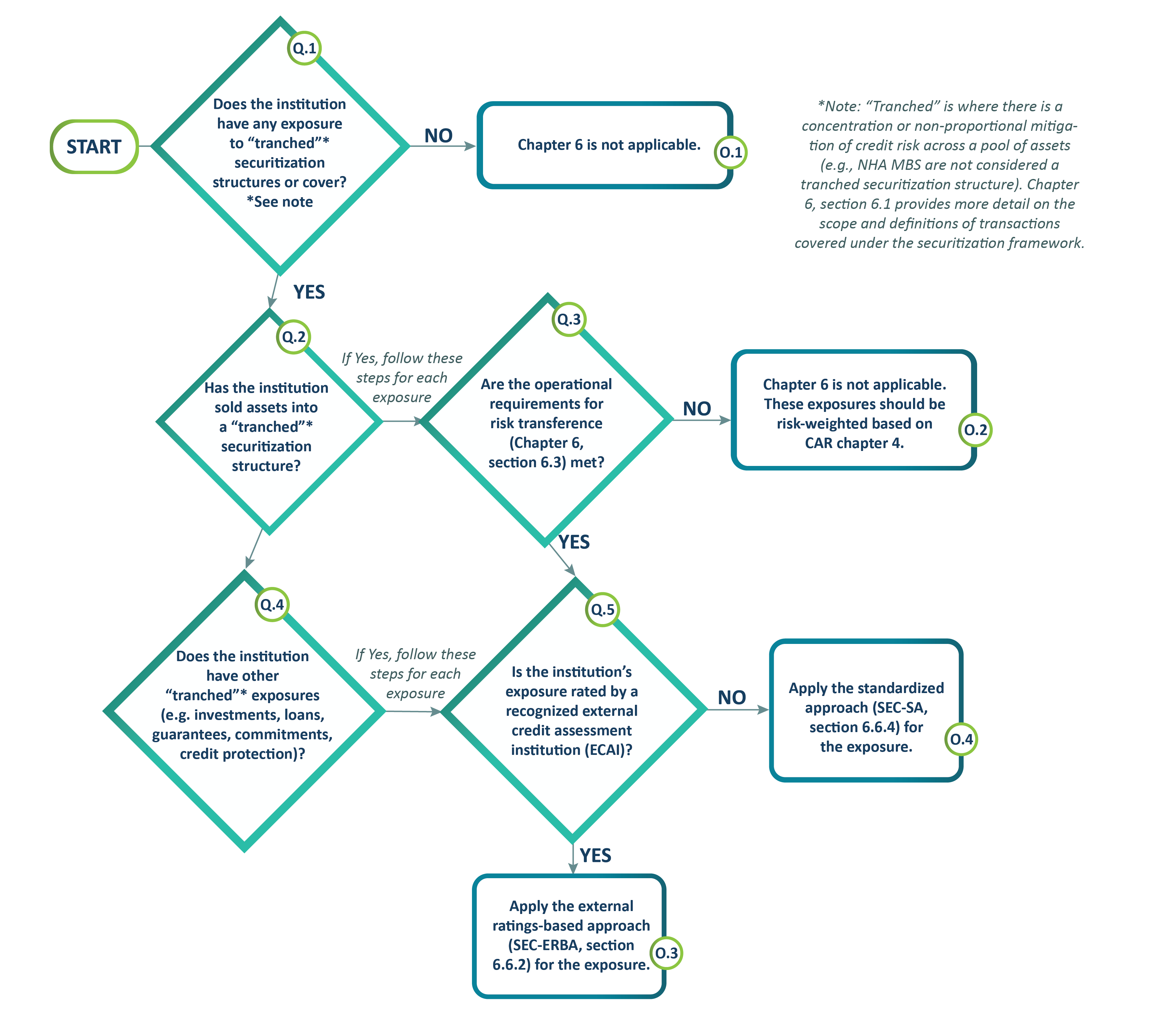

Securitization Exposures

-

Chapter 6 of the CAR Guideline details how to calculate RWA for securitization exposures. This chapter is only applicable for Category II SMSBs if they have securitization exposures that involve tranching, with associated subordination of credit risk, as defined in paragraph 3 and section 6.1 of Chapter 6 of the CAR GuidelineFootnote 15.

- Securitization exposures can include, but are not restricted to the following: asset-backed securities, mortgage-backed securities, credit enhancements, liquidity facilities, loans to securitization vehicles to fund the acquisition of assets, interest rate or currency swaps, credit derivatives and tranched coverFootnote 16.

-

In order to apply the securitization treatment in Chapter 6 of the CAR Guideline for exposures originated by the institution (e.g. assets sold into a securitization structure), the operational requirements for risk transference detailed in section 6.3 must be metFootnote 17. If these requirements are not met, institutions must risk-weight the assets underlying the securitization as if they had not been securitized.

-

When calculating RWA for each securitization exposure, Category II SMSBs must use either the External Ratings-Based Approach (SEC-ERBA, section 6.6.2 of the CAR Guideline) or the Standardized Approach (SEC-SA, section 6.6.4 of the CAR Guideline) for securitization exposures. Since Category II SMSBs are not eligible to use either the Internal Ratings-Based Approach (SEC-IRBA, section 6.6.1 of the CAR Guideline) or the Internal Assessment Approach (SEC-IAA, section 6.6.3 of the CAR Guideline), these sections do not apply.

Text Description - Chart 8

Start:

Question 1: Does the institution have any exposure to "tranched"Footnote * securitization structures or cover?

- If yes, proceed to Question 2.

- If no, proceed to Output 1.

Question 2: Has the institution sold assets into a "tranched"Footnote * securitization structure?

- If yes, follow these steps for each exposure. Proceed to Question 3.

- If no, proceed to Question 4.

Output 1: Chapter 6 is not applicable.

- END.

Question 3: Are the operational requirements for risk transference (Chapter 6, section 6.3) met?

- If yes, proceed to Question 5.

- If no, proceed to Output 2.

Question 4: Does the institution have other "tranched"Footnote * exposures (e.g. investments, loans, guarantees, commitments, credit protection)?

- If yes, follow these steps for each exposure. Proceed to Question 5.

- If no, END.

Question 5: Is the institution's exposure rated by a recognized external credit assessment institution (ECAI)?

Output 2: Chapter 6 is not applicable. These exposures should be risk-weighted based on CAR Chapter 4.

- END.

Output 3: Apply the external ratings-based approach (SEC-ERBA, section 6.6.2) for the exposure.

- END.

Output 4: Apply the standardized approach (SEC-SA, section 6.6.4) for the exposure.

- END.

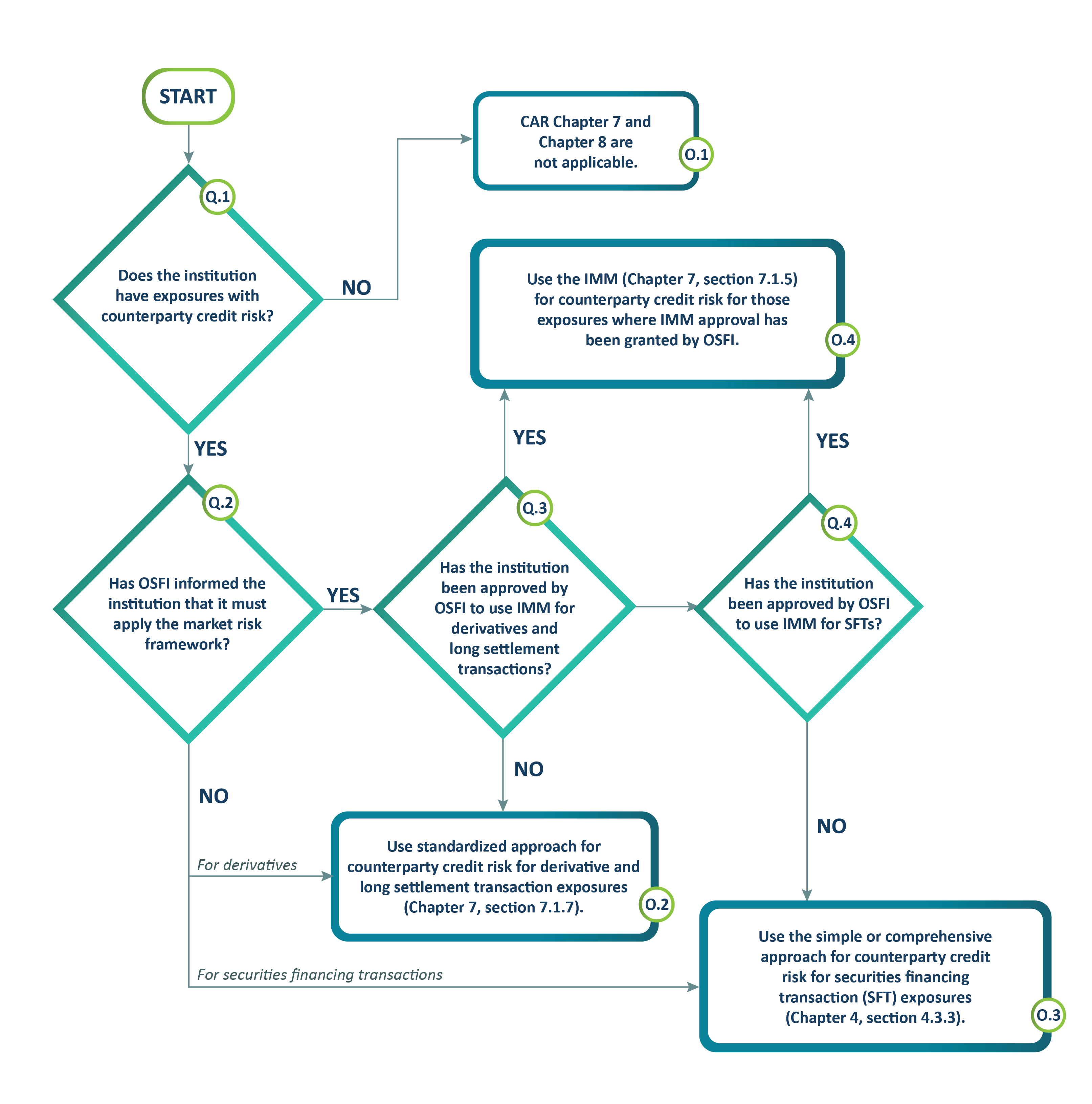

Counterparty Credit Risk

-

Category II SMSBs with exposures to instruments with counterparty credit risk must also calculate a capital charge for counterparty credit risk for these exposures. Exposures with counterparty credit risk, as detailed in CAR Chapter 7, section 7.1.2, are:

- Over the counter (OTC) Derivatives;

- Exchange-traded derivatives (ETDs);

- Long Settlement transactions; and,

- Securities Financing Transactions (SFTs).

-

The following approaches should be used for counterparty credit risk exposure, unless the institution has approval from OSFI to use an Internal Model Method (IMM):

- For derivative and long settlement transaction exposures:

- the standardized approach for counterparty credit risk (SA-CCR), detailed in Chapter 7, section 7.1.7 of the CAR Guideline, should be used to calculate exposure or exposure at default (EAD); and

- Chapter 4 of the CAR Guideline should be used to determine the applicable risk-weight.

- For SFT exposures:

- the simple or comprehensive approach (detailed in CAR Chapter 4, section 4.3.3) should be used to calculate exposure or EAD; and,

- Chapter 4 of the CAR Guideline should be used to determine the applicable risk-weight.

- For derivative and long settlement transaction exposures:

-

Only those Category II SMSBs that are required by OSFI to apply the market risk framework are eligible to apply to use an IMM for counterparty credit risk, as detailed in CAR Chapter 7, section 7.1.4. These institutions can apply to OSFI to use IMM for either derivative or SFT exposures (or both). CAR Chapter 7, section 7.1.5, details how to measure exposure and capital requirements using IMM.

Text Description - Chart 9

Start:

Question 1: Does the institution have exposures with counterparty credit risk?

- If yes, proceed to Question 2.

- If no, proceed to Output 1.

Question 2: Has OSFI informed the institution that it must apply the market risk framework?

- If yes, for derivatives proceed to Question 3 or for securities financing transactions proceed to Question 4.

- If no, for derivatives proceed to Output 2 or for securities financing transactions proceed to Output 3.

Output 1: CAR Chapter 7 and Chapter 8 are not applicable.

- END.

Question 3: Has the institution been approved by OSFI to use IMM for derivatives and long settlement transactions?

Question 4: Has the institution been approved by OSFI to use IMM for SFTs?

Output 2: Use standardized approach for counterparty credit risk for derivative and long settlement transaction exposures (Chapter 7, section 7.1.7).

- END.

Output 3: Use the simple or comprehensive approach for counterparty credit risk for securities financing transaction (SFT) exposures (Chapter 4, section 4.3.3).

- END.

Output 4: Use the IMM (Chapter 7, section 7.1.5) for counterparty credit risk for those exposures where IMM approval has been granted by OSFI.

- END.

-

Category II SMSBs are also subject to capital requirements for credit value adjustment risk (CVA, see Chapter 8 of the CAR Guideline) to cover the risk of mark-to-market losses on the expected counterparty risk for each of the following types of exposures:

- Over the counter (OTC) instruments with counterparty credit risk (e.g. OTC derivatives)Footnote 18; and

- Securities financing transactions (SFT), if OSFI has notified the institution that it has determined that the institution's CVA loss exposures arising from SFT transactions are material.

-

Chapter 8 of the CAR Guideline is not applicable for Category II SMSBs that do not have either of the two types of exposures in paragraph 55Footnote 19.

Text Description - Chart 10

Start:

Question 1: Does the institution have exposures to covered transactions (Chapter 8, paragraph 6)?

- If yes, proceed to Question 2.

- If no, proceed to Output 1.

Question 2: Has the institution received OSFI approval to use SA-CVA?

- If yes, proceed to Output 2.

- If no, proceed to Question 3.

Output 1: No CVA capital charge.

- END.

Output 2: Use SA-CVA or a combination of SA-CVA and BA-CVA to calculate CVA capital charge.

- END.

Question 3: Does the institution's aggregate notional amount of non-centrally cleared derivatives exceed the materiality threshold of $150 billion?

Output 3: Use BA-CVA to calculate CVA capital charge (Chapter 8, section 8.2).

- END.

Output 4: May use an alternative treatment (Chapter 8, paragraph 10) or BA-CVA (Chapter 8, section 8.2) to calculate CVA capital charge.

- END.

5.1.4 Market Risk and Trading Book Exposures

-

Category II SMSBs will be informed by OSFI if the market risk framework is applicable to their institution. These institutions should use one of the approaches detailed in Chapter 9 of the CAR Guideline to calculate RWA for market risk, in consultation with OSFI.

-

All other Category II SMSBs, for whom the market risk framework is not applicable, should include any trading book exposures in the calculation of RWA using the approaches detailed in other chapters of the CAR GuidelineFootnote 20. For these institutions, Chapter 9 of the CAR Guideline is not applicable.

Text Description - Chart 11

Start:

Question 1: Has OSFI informed the institution that it must apply the market risk framework?

Output 1: Use one of the approaches in Chapter 9 to calculate RWA for market risk (in consultation with OSFI).

- END.

Output 2: There is no market risk capital charge (Chapter 9 is not applicable).

- Proceed to Output 3.

Output 3: The capital charge for any trading book exposures should be calculated using approaches in other CAR chapters (see Annex 2).

- END.

5.2 Leverage Requirements

-

The LR Guideline outlines the leverage requirements for Category II SMSBs, including minimum and authorized leverage ratios. Category II SMSBs are not subject to the leverage ratio buffer described in section IV of the LR Guideline.

5.3 Liquidity Requirements

-

Chapter 1 of the LAR Guideline provides an overview of the liquidity adequacy requirements. Category II SMSBs are subject to all of the liquidity metrics detailed in section 1.3 of the LAR Guideline, with the following exceptions:

- Category II SMSBs are not subject to any requirements related to the Net Stable Funding Ratio (NSFR).

- Category II SMSBs are not subject to any requirements related to the Operating Cash Flow Statement (OCFS).

- Category II SMSBs are only subject to the intraday liquidity monitoring tools (LAR Chapter 7) if they are direct clearers.

-

OSFI generally considers the liquidity adequacy of subsidiaries of SMSBs in the context of the consolidated parent entity. Therefore, subsidiaries of Category II SMSBs may be exempted from the minimum liquidity requirements in the LAR Guideline, provided they meet the criteria in section 1.2 of Chapter 1 of the LAR Guideline.

-

All Category II SMSBs are subject to the requirements of the Liquidity Coverage Ratio (LCR), detailed in Chapter 2 of the LAR Guideline.

-

Category II SMSBs are not subject to the Net Stable Funding Ratio (NSFR) requirements. Therefore Chapter 3 of the LAR Guideline is not applicable to these institutions.

-

Chapter 4 of the LAR Guideline details the Net Cumulative Cash Flow (NCCF) metric and related requirements. Category II SMSBs should complete the Streamlined NCCF unless directed otherwise by OSFI.

-

The Operating Cash Flow Statement (OCFS) detailed in Chapter 5 of the LAR Guideline is not applicable to Category II SMSBs.

-

Chapter 6 of the LAR Guideline details several other liquidity monitoring tools applicable to Category II institutions to assess their liquidity adequacy.

- Chapter 7 of the LAR Guideline (Intraday Liquidity Monitoring Tools) covers intraday liquidity monitoring tools applicable to Category II SMSBs. However, they are only subject to the regulatory reporting requirements outlined in Chapter 7 if they are direct clearers of Lynx.

VI. Category III SMSBs – Capital and Liquidity Requirements

6.1 Risk-Based Capital Requirements

-

Category III SMSBs are subject to a Simplified Risk-Based Capital Ratio (SRBCR), as described in section 1.6.2 in Chapter 1 of the CAR Guideline.

- The minimum SRBCRs for Category III SMSBs are in CAR Chapter 1, section 1.6.2.

- Category III SMSBs are also subject to the capital conservation buffer detailed in section 1.7.1 of the CAR Guideline.

- The capital targets for Category III SMSBs are summarized in CAR Chapter 1, section 1.10.

- The countercyclical buffer (CAR Chapter 1, section 1.7.2) may also be applicable to Category III institutionsFootnote 21. OSFI will inform SMSBs whenever the countercyclical buffer has been deployed in Canada, and must be applied to domestic exposures. Category III institutions must also apply the countercyclical buffer for any international exposures where the countercyclical buffer has been deployed by the local regulator.

- The D-SIB Surcharge and the Domestic Stability Buffer described in Chapter 1 of the CAR Guideline are not applicable to Category III SMSBs.

- Annex 1 of Chapter 1 of the CAR Guideline (Domestic Systemic Importance and Capital Targets) is not applicable to Category III SMSBs.

-

Sections 1.4 and 1.5 of Chapter 1 of the CAR Guideline (IRB approach) are also not applicable to Category III SMSBs.

-

Chapter 2 of the CAR Guideline defines the tiers of capital used in the calculation of the risk-based capital ratios, including the SRBCR, as well as required adjustments to each tier of capital.

-

Chapter 3 of the CAR Guideline details how to calculate operational risk capital. Category III SMSBs must use the Simplified Standardized Approach, therefore CAR Chapter 3, section 3.4 (Standardized Approach) is not applicable.

-

Chapters 4 to 9 of the CAR Guideline are generally not applicable to Category III SMSBs, as there are no Credit or Market RWA requirements for the SRBCR. However, chapters 1 to 3 of the CAR refer to certain sections of these other chapters, which Category III SMSBs may therefore need to review for certain exposures.

6.2 Leverage Requirements

-

Since the measure of leverage is incorporated into the SRBCR, Category III SMSBs are not subject to a separate minimum Pillar 1 leverage requirement. Therefore, the LR Guideline is not applicable to these institutions.

6.3 Liquidity Requirements

-

Category III SMSBs are only subject to the requirements related to the Operating Cash Flow Statement (OCFS), as detailed in Chapter 5 of the LAR Guideline.

-

Chapter 7 of the LAR Guideline (Intraday Liquidity Monitoring Tools) covers intraday liquidity monitoring tools applicable to Category III SMSBs. However, they are only subject to the regulatory reporting requirements outlined in Chapter 7 if they are direct clearers of Lynx.

- The rest of the metrics and returns described in Chapter 1 of the LAR Guideline are therefore not applicable to Category III SMSBs. As a result, the following chapters of the LAR Guideline are also not applicable to Category III SMSBs:

- Chapter 2 (Liquidity Coverage Ratio - LCR)

- Chapter 3 (Net Stable Funding Ratio - NSFR)

- Chapter 4 (Net Cumulative Cash Flow - NCCF)

- Chapter 6 (Liquidity Monitoring Tools)

Annex 1 – Summary of SMSB Capital and Liquidity Requirements by Category

| Requirements | OSFI Guideline Reference | Category I | Category II | Category III |

|---|---|---|---|---|

| Risk-based capital requirements |

Risk-based Ratio(s) and Definition of Capital CAR Chapters 1-2 |

CET1/Tier1/Total Capital Ratios | CET1/Tier1/Total Capital Ratios | Simplified Risk-Based Capital Ratios for CET1/Tier1/Total Capital |

| Risk-based capital requirements |

Operational Risk Capital Methodology CAR Chapter 3 |

Standardized ApproachAnnex 1a table footnote * or Simplified Standardized Approach | Simplified Standardized Approach | Simplified Standardized Approach |

| Risk-based capital requirements |

Credit Risk Capital Methodology CAR Chapters 4-8Annex 1a table footnote ** |

Internal Ratings-Based (IRB)Annex 1a table footnote * or Standardized Approach with simplified treatment available for certain asset classes | Standardized Approach with simplified treatment available for certain asset classes | n/a |

| Risk-based capital requirements |

Market Risk Capital MethodologyAnnex 1a table footnote *** CAR Chapter 9 |

Internal ModelsAnnex 1a table footnote * or Standardized Approach | Internal ModelsAnnex 1a table footnote * or Standardized Approach | n/a |

| Leverage Ratio (LR) | Leverage Requirement | Leverage Ratio | Leverage Ratio | No Leverage Ratio |

|

Annex 1a table footnotes

|

||||

| Requirements | OSFI Guideline Reference | Category I | Category II | Category III |

|---|---|---|---|---|

| Liquidity Coverage Ratio (LCR) | LAR Chapter 2 | LCR | LCR | No LCR |

| Cash Flow-Based Requirement | LAR Chapter 4 or 5 | Comprehensive NCCF | Streamlined NCCF (unless directed otherwise by OSFI) | Operating Cash Flow Statement (OCFS) |

| Net Stable Funding Ratio (NSFR) | LAR Chapter 3 | Only for institutions with significant wholesale funding relianceAnnex 1b table footnote * | No NSFR | No NSFR |

| Intraday Liquidity Requirements | LAR Chapter 7 | Chapter 7 of the LAR Guideline (Intraday Liquidity Monitoring Tools) covers intraday liquidity monitoring tools applicable to Category I, II and III SMSBs. However, they are only subject to the regulatory reporting requirements outlined in Chapter 7 if they are direct clearers of Lynx. | Chapter 7 of the LAR Guideline (Intraday Liquidity Monitoring Tools) covers intraday liquidity monitoring tools applicable to Category I, II and III SMSBs. However, they are only subject to the regulatory reporting requirements outlined in Chapter 7 if they are direct clearers of Lynx. | Chapter 7 of the LAR Guideline (Intraday Liquidity Monitoring Tools) covers intraday liquidity monitoring tools applicable to Category I, II and III SMSBs. However, they are only subject to the regulatory reporting requirements outlined in Chapter 7 if they are direct clearers of Lynx. |

|

Annex 1b table footnotes

|

||||

Annex 2 – Application of Credit and Market Risk CAR Chapters by Type of Exposure

| Type of Exposure | Credit Risk | Counterparty Credit Risk (CCR) | Credit Value Adjustment (CVA) | Market Risk | |

|---|---|---|---|---|---|

| Category I Institutions Approved for IRB | All other Category I and II Institutions | ||||

| "Tranched" Securitization Exposures that meet Risk Transference Criteria | Chapter 6 | Chapter 6 | n/a | n/a | n/a |

| Bilateral OTC Derivatives (including long settlement transactions) | Chapter 4 or 5, to determine the RW applicable to CCR EAD | Chapter 4 to determine the RW applicable to CCR EAD | Chapter 7 to determine CCR EAD | Chapter 8 (applies to all institutions involved in covered transactions in both banking book and trading book (per Chapter 8, paragraph 5)) | Chapter 9 (only for Market Risk BanksAnnex 2 table footnote *) |

| Centrally Cleared Derivatives | Chapter 4 or 5, to determine the RW applicable to CCR EAD | Chapter 4 to determine the RW applicable to CCR EAD | Chapter 7 to determine CCR EAD | n/a | Chapter 9 (only for Market Risk BanksAnnex 2 table footnote *) |

| Securities Financing Transactions (SFT) | Chapter 4 or 5, to determine the RW applicable to CCR EAD | Chapter 4 to determine the RW applicable to CCR EAD | Chapter 4 or Chapter 7 to determine CCR EAD | Chapter 8Annex 2 table footnote *** (applies to all institutions involved in covered transactions in both banking book and trading book (per Chapter 8, paragraph 5)) | Chapter 9 (only for Market Risk BanksAnnex 2 table footnote *) |

| All other Banking Book Exposures | Chapter 4 or 5, depending on exposure | Chapter 4 | n/a | n/a | n/a |

| All other Trading Book Exposures | Chapter 4 or 5, depending on exposure (only for non-Market Risk BanksAnnex 2 table footnote **) | Chapter 4 (only for non-Market Risk BanksAnnex 2 table footnote **) | n/a | n/a | Chapter 9 (only for Market Risk BanksAnnex 2 table footnote *) |

|

Annex 2 table footnotes

|

|||||