Pension Plan for the Public Service of Canada: Population and Mortality Study - Actuarial Study No. 25

Office of the Chief Actuary

Office of the Superintendent of Financial Institutions Canada

255 Albert Street

Ottawa, Ontario K1A 0H2

E-mail address: oca-bac@osfi-bsif.gc.ca

Table of contents

List of tables

- Table 1 - Annualized growth rate for male and female from plan years 2011 to 2023

- Table 2 - Proportion of disabled pensionersa to member population for male and female for plan years 2011 and 2023

- Table 3 - Male-to-female ratio for plan years 2011 and 2023

- Table 4 - Average age and percentage of centenarians by population type for plan years 2011 and 2023

- Table 5 - Life expectancy at age 65 for male and female for plan years 2011 and 2023

- Table 6 - Evolution of the number of members and surviving spouses aged 50 and over between plan year 2011 and 2023

- Table 7 - Average longevity improvement factors between plan years 2012 and 2022

- Table 8 - Non-disabled male member mortality rates for plan years 2012 to 2022

- Table 9 - Non-disabled female member mortality rates for plan years 2012 to 2022

- Table 10 - Disabled male member mortality rates for plan years 2012 to 2022

- Table 11 - Disabled female member mortality rates for plan years 2012 to 2022

- Table 12 - Surviving spouse male mortality rates for plan years 2012 to 2022

- Table 13 - Surviving spouse female mortality rates for plan years 2012 to 2022

- Table 14 - 11-year average longevity improvement factors

- Table 15 - Complete period of life table

List of figures

- Figure 1 - Period life expectancy at age 65 for plan year 2023

- Figure 2 - Evolution of the number of non‑disabled population aged 50 and over from plan years 2011 to 2023

- Figure 3 - Average age of non-disabled population aged 50 and over from plan years 2011 to 2023

- Figure 4 - Age distribution of the 50 and over non-disabled male members from plan years 2011 to 2023

- Figure 5 - Age distribution of the 50 and over non-disabled female members from plan years 2011 to 2023

- Figure 6 - Centenarian members as percentage of the non-disabled populations aged 50 and over and their average age from plan years 2011 to 2023

- Figure 7 - Evolution of disabled population aged 50 and over from plan years 2011 to 2023

- Figure 8 - Evolution of surviving spouse population from plan years 2011 to 2023

- Figure 9 - Evolution of percentage of centenarians in surviving spouse population from plan years 2011 to 2023

- Figure 10 - Mortality rates for age group 65 to 69 from plan years 2012 to 2022

- Figure 11 - Mortality rates for age group 70 to 74 from plan years 2012 to 2022

- Figure 12 - Mortality rates for age group 75 to 79 from plan years 2012 to 2022

- Figure 13 - Mortality rates for age group 80 to 84 from plan years 2012 to 2022

- Figure 14 - Mortality rates for age group 85 to 89 from plan years 2012 to 2022

- Figure 15 - Mortality rates for age group 90 to 94 from plan years 2012 to 2022

- Figure 16 - Period life expectancies at age 65 for all three groups from plan years 2012 to 2022

- Figure 17 - Period life expectancies at age 65 in 2021

- Figure 18 - Crude monthly mortality rate for aged 50 and over from plan years 2012 to 2022

1 Executive summary

1.1 Purpose

This study was conducted to support the identification of mortality assumptions for the 20th Actuarial Report on the Pension Plan for the Public Service of Canada (PSPP) as at 31 March 2023.

The increase in life expectancy and the changes in future longevity improvement rates are important risks faced by defined benefit pension plans. This study helps to manage these risks by understanding the evolution of plan experience in order to determine appropriate mortality assumptions.

1.2 Context

This is the Office of the Chief Actuary's (OCA) second mortality experience study of the Pension Plan for the PSPP. It examines population characteristics, trends in mortality rates, longevity improvement factors and period life expectancy of various populations in the PSPP.

The PSPP, which is governed by the Public Service Superannuation Act, is a defined benefit pension plan offered to federal public service employees. The PSPP holds more than $200 billion in actuarial liability and covers more than 700,000 members.

1.3 Scope

This study focuses on historical information for yearsFootnote 1 2011 to 2023 and includes PSPP members and surviving spouses aged 50 and over, representing more than 400,000 members.

The data are grouped into three distinct populations: non-disabled population, disabled population, and surviving spouse population.

- The non-disabled population is composed of contributors and non-disabled pensioners. Non-disabled pensioners include deferred pensioners.

- The disabled population is composed of disabled pensioners.

- The surviving spouse population is composed of spouses or former spouses of members who are receiving survivor benefits following the deaths of the members. Due to limited information, no distinction is made between non‑disabled or disabled surviving spouses.

- For the purposes of establishing mortality rates, data are deemed credible between ages 50 and 95 for the non‑disabled and disabled member populations. For the surviving spouse population, data are deemed credible between ages 60 and 95 for men and between ages 55 and 95 for women. This study was done on an age-nearest basis.Footnote 2

1.4 Highlights

1.4.1 Population statistics and trends for aged 50 and over

The total population grew at an average annual rate of 1.5% from plan year 2011 to plan year 2023. The annualized growth rate by population and gender is presented below.

| Population Type | Male (%) | Female (%) |

|---|---|---|

| Non-disabled | 0.9 | 3.1 |

| Disabled | −1.2 | 3.1 |

| Surviving spouse | 3.9 | −1.6 |

The proportion of disabled population declined over the period of study.

| Male | Female | ||

|---|---|---|---|

| 2011 | 2023 | 2011 | 2023 |

| 3.7% | 2.9% | 5.0% | 4.9% |

The ratio of the number of males to females decreased over the period of study for both the non-disabled and disabled populations while it increased for the surviving spouse population. For the non‑disabled population, the number of males surpassed that of females in plan year 2011, whereas they were equal in 2023.

| Population Type | 2011 | 2023 |

|---|---|---|

| Non-disabled | 1.3 | 1.0 |

| Disabled | 0.9 | 0.6 |

| Surviving spouse | 0.1 | 0.2 |

The average age increased for each population and gender over the period of study and the proportion of members over age 100 significantly increased.

| Male | Female | |||

|---|---|---|---|---|

| 2011 | 2023 | 2011 | 2023 | |

| Average age: Non-disabled | 66.1 | 67.5 | 62.8 | 64.9 |

| Average age: Disabled | 67.7 | 68.4 | 64.7 | 65.7 |

| Average age: Surviving spouse | 72.2 | 74.7 | 79.4 | 81.1 |

| Centenarians to non‑disabled | 0.01% | 0.09% | 0.01% | 0.12% |

| Centenarians to surviving spouse | 0.02% | 0.34% | 0.09% | 1.46% |

1.4.2 Period life expectancy at age 65

Period life expectancies increased for the non-disabled population while they decreased slightly for the disabled and surviving spouse populations over the period of study.

| Population Type | Male | Female | ||

|---|---|---|---|---|

| 2011 | 2023 | 2011 | 2023 | |

| Non-disabled | 19.7 | 20.6 | 22.2 | 22.5 |

| Disabled | 15.1 | 15.0 | 18.3 | 17.9 |

| Surviving spouse | 18.1 | 17.9 | 21.5 | 21.1 |

1.4.3 Longevity improvements

The 11-year average longevity improvement factors from plan years 2012 to 2022 for non‑disabled population were positive for both genders and all age groups between 50 and 95, except for females in the 90 to 95 age group. A positive average longevity improvement factor means that the mortality rates have generally decreased over time.

1.4.4 Salary impact

As salary level increases, period life expectancy increases. Non‑disabled female population is less affected by the level of salary than non‑disabled male population.

2 Definitions

- Active members (contributors):

-

Public servants who are currently contributing to the PSPP

- Deferred pensioners:

-

Former public servants who have terminated employment, for reason other than disability and retirement, but maintained entitlement to pension benefits from the PSPP

- Disabled pensioners:

-

Former public servants who have terminated employment for reason of disability

- Non-disabled members:

-

Public servants who are active, deferred, or retired status

- Members:

-

Public servant who are active, deferred, disabled, or retired status

- Period life expectancy:

-

Calculation of life expectancy assuming mortality rates remain constant into the future

- Populations:

-

Aged 50 and over non-disabled members, disabled members, or surviving spouses

- Retired members:

- Former public servants who have terminated employment for reason of retirement

- Status:

-

Possible participation status of a person to the PSPP: active, deferred, disabled, retired or surviving spouse

- Surviving spouse:

- Status of a spouse or former spouse who is receiving survivor benefits following the death of the member, or

- Population type that contains spouse or former spouse of a member who is receiving survivor benefits following the death of the member.

3 Considerations

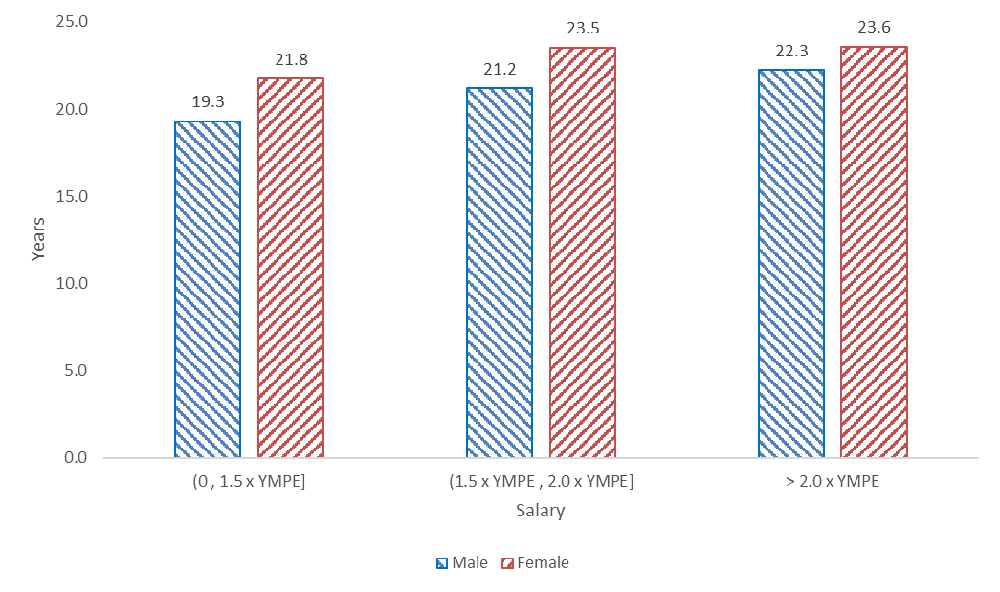

The last Pension Plan for the Public Service of Canada Mortality Study, Actuarial Study No. 14, suggested that socioeconomic factors such as a person's salary level may influence mortality rates. Consequently, starting from the Actuarial Report as at 31 March 2017, the mortality assumptions included in the actuarial reports for the PSPP take into account salary-weighted mortality rates. The results from an analysis in this current study reaffirms that the level of salary influences life expectancy. As shown in Figure 1, life expectancy increases as the level of salary increases.

The salaries of the PSPP non‑disabled population aged 50 to 95 are grouped in three levels:

- less than or equal to 1.5 times Year's Maximum Pensionable Earnings (YMPE)Footnote 3 (46%)

- more than 1.5 times YMPE and less than or equal to 2.0 times of YMPE (29%)

- more than 2.0 times of YMPE (25%)

Figure 1 shows that the period life expectancy for the non-disabled female population is less affected by the increase in the salary level beyond two times YMPE than the male population. Although the salary level affects mortality rates, the mortality rates and period life expectancies calculated beyond this section herein this report are not salary-weighted so that they are comparable to other external studies.

Figure 1 - Text version

| Salary | Male | Female |

|---|---|---|

| (0, 1.5 × YMPE] | 19.3 | 21.8 |

| (1.5 × YMPE, 2.0 × YMPE] | 21.2 | 23.5 |

| > 2.0 × YMPE | 22.3 | 23.6 |

4 Data

The data we use in this study are seriatim data provided by Public Services and Procurement Canada (PSPC). We use the same data to perform the statutory valuations.

We exclude some records due to:

- Date of death being before the start of the study period

- Missing key data such as birthdate

- Cash outs over the study period

- Inconsistent date of entry in relation to the date of termination over the study period

- Inconsistent benefit entitlement stop date in relation to the date of last payment over the study period

5 Population characteristics

The populations in this study refer to the members and the surviving spouses aged 50 and over only. Table 6 shows the number and the annualized rate of growth of the members and the surviving spouses from plan year 2011 to plan year 2023. Although the number of non‑disabled females was smaller than the number of non‑disabled males by 22% in plan year 2011, the non‑disabled female population grew at a faster rate leading to the number of non‑disabled females exceeding the number of non‑disabled males by 1.7% by plan year 2023.

| Male | Female | |||||

|---|---|---|---|---|---|---|

| 2011 | 2023 | % Annual Change | 2011 | 2023 | % Annual Change | |

| Non-disabled | 158,141 | 175,728 | 0.9% | 123,276 | 178,691 | 3.1% |

| Active | 52,829 | 57,592 | 0.7% | 57,392 | 66,534 | 1.2% |

| Deferred | 2,389 | 4,817 | 6.0% | 3,032 | 5,716 | 5.4% |

| Retired | 102,923 | 113,319 | 0.8% | 62,852 | 106,441 | 4.5% |

| Disabled | 5,995 | 5,216 | −1.2% | 6,486 | 9,305 | 3.1% |

| Surviving spouses | 4,637 | 7,367 | 3.9% | 48,375 | 39,694 | −1.6% |

| Total | 168,773 | 188,311 | 0.9% | 178,137 | 227,690 | 2.1% |

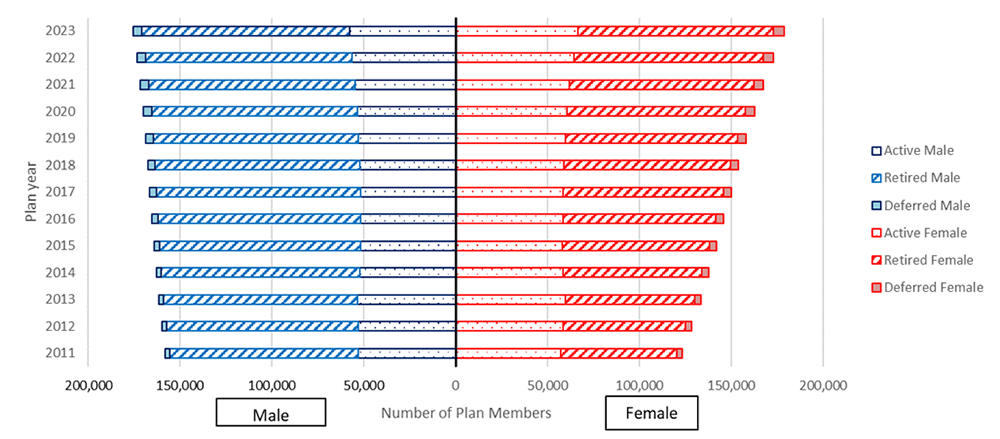

Figure 2 shows the evolution of the non-disabled population aged 50 and over broken down by year and by status. The growth rate for active populations ranges from −1.9% (PY 2014) to 3.3% (PY 2022) for males and from −2.0% (PY 2014) to 4.1% (PY 2022) for females. The fluctuation in the growth rate reflects different government policies over time. From plan years 2019 to 2023, the average growth rates were 2% for active males and 2.4% for active females. The number of deferred and retired members grew steadily throughout the study period.

Figure 2 - Text version

| Plan Year | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Active Male | 52829 | 52876 | 53280 | 52286 | 51793 | 51807 | 51876 | 52179 | 52910 | 53422 | 54648 | 56463 | 57592 |

| Deferred Male | 2389 | 2478 | 2652 | 2837 | 3079 | 3481 | 3663 | 3836 | 3992 | 4519 | 4601 | 4697 | 4817 |

| Retired Male | 102923 | 104366 | 105607 | 107808 | 109280 | 110048 | 110929 | 111333 | 111677 | 112123 | 112571 | 112467 | 113319 |

| Active Female | 57392 | 58544 | 59850 | 58651 | 58208 | 58353 | 58669 | 59028 | 59594 | 60476 | 61976 | 64510 | 66534 |

| Deferred Female | 3032 | 3225 | 3457 | 3676 | 3917 | 4198 | 4380 | 4617 | 4877 | 5202 | 5358 | 5475 | 5716 |

| Retired Female | 62852 | 66560 | 70206 | 75505 | 79919 | 83391 | 87117 | 90420 | 93784 | 97103 | 100192 | 102829 | 106441 |

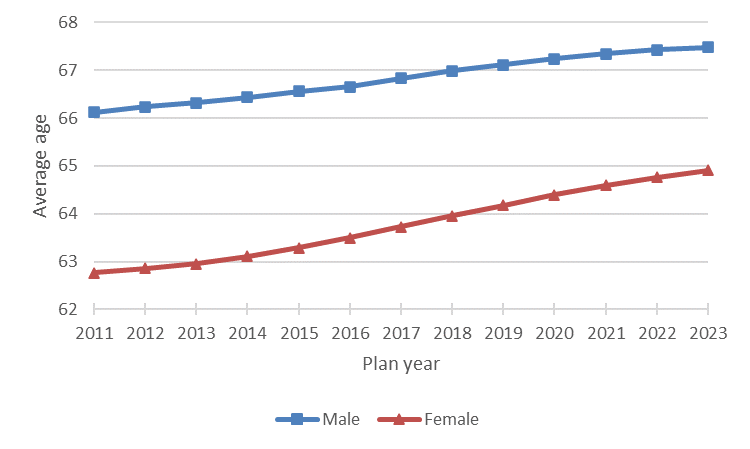

Figure 3 shows the evolution of the average age of the non-disabled population aged 50 and over from plan year 2011 to plan year 2023. The average age of a non-disabled male steadily increased from 66.1 years in plan year 2011 to 67.5 years in plan year 2023 and from 62.8 years to 64.9 years for a non‑disabled female.

Chart 3 - Text version

| Plan Year | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Average Age Male | 66.1 | 66.2 | 66.3 | 66.4 | 66.6 | 66.7 | 66.8 | 67.0 | 67.1 | 67.2 | 67.3 | 67.4 | 67.5 |

| Average Age Female | 62.8 | 62.9 | 62.9 | 63.1 | 63.3 | 63.5 | 63.7 | 64.0 | 64.2 | 64.4 | 64.6 | 64.8 | 64.9 |

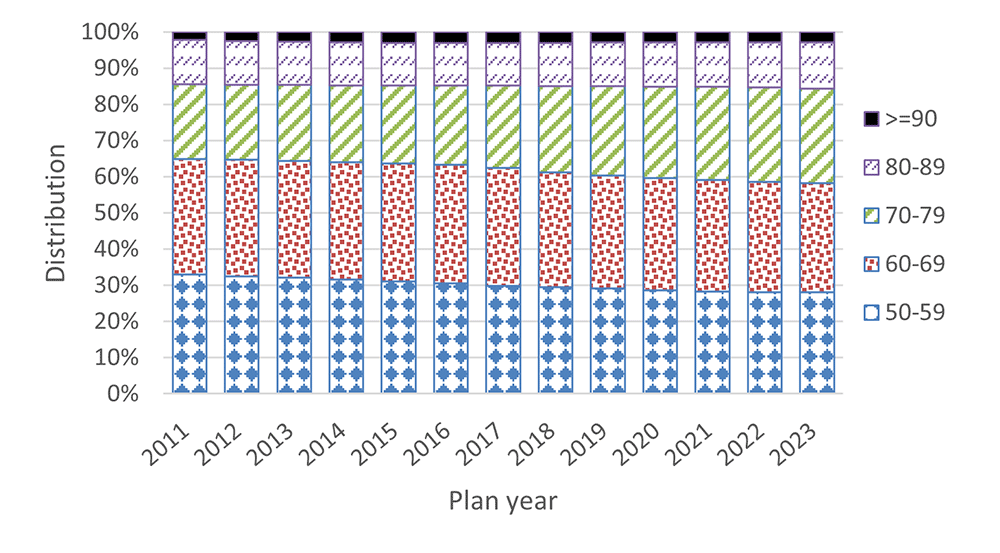

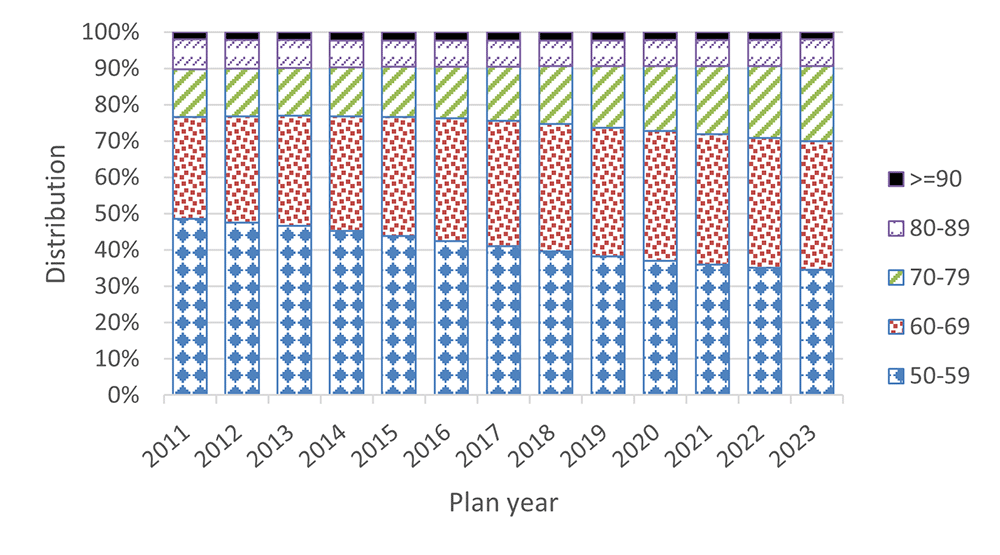

Figure 4 and Figure 5 show the evolution of the non-disabled population broken down by age group. In plan year 2011, the age range 50 to 69 made up 65% of the male population and 77% of the female population. In plan year 2023, these proportions dropped to 58% for males and 70% for females as age range 70 to 79 became larger for both genders.

Figure 4 - Text version

| Plan year | 50-59 | 60-69 | 70-79 | 80-89 | >=90 |

|---|---|---|---|---|---|

| 2011 | 0.330705 | 0.318659 | 0.206366 | 0.122277 | 0.021993 |

| 2012 | 0.325119 | 0.322283 | 0.206875 | 0.120905 | 0.024818 |

| 2013 | 0.321056 | 0.323736 | 0.209194 | 0.119123 | 0.026891 |

| 2014 | 0.3156 | 0.324825 | 0.212519 | 0.118731 | 0.028325 |

| 2015 | 0.310529 | 0.325655 | 0.216854 | 0.117586 | 0.029375 |

| 2016 | 0.305874 | 0.327019 | 0.22049 | 0.116998 | 0.029618 |

| 2017 | 0.299517 | 0.32512 | 0.227671 | 0.118185 | 0.029507 |

| 2018 | 0.294446 | 0.318402 | 0.238676 | 0.119398 | 0.029077 |

| 2019 | 0.290991 | 0.31361 | 0.246958 | 0.120145 | 0.028295 |

| 2020 | 0.287251 | 0.310271 | 0.252329 | 0.121983 | 0.028166 |

| 2021 | 0.283797 | 0.307624 | 0.257543 | 0.122902 | 0.028134 |

| 2022 | 0.281823 | 0.304561 | 0.260962 | 0.124405 | 0.02825 |

| 2023 | 0.281401 | 0.301904 | 0.261387 | 0.127037 | 0.028271 |

Figure 5 - Text version

| Plan year | 50-59 | 60-69 | 70-79 | 80-89 | >=90 |

|---|---|---|---|---|---|

| 2011 | 0.485545 | 0.280801 | 0.132402 | 0.081338 | 0.019915 |

| 2012 | 0.476478 | 0.291742 | 0.131958 | 0.079117 | 0.020705 |

| 2013 | 0.466838 | 0.302937 | 0.132504 | 0.075925 | 0.021796 |

| 2014 | 0.453073 | 0.314673 | 0.136057 | 0.073851 | 0.022346 |

| 2015 | 0.43961 | 0.326765 | 0.138288 | 0.072372 | 0.022965 |

| 2016 | 0.425525 | 0.338011 | 0.141871 | 0.071104 | 0.023489 |

| 2017 | 0.411298 | 0.345305 | 0.149375 | 0.070229 | 0.023794 |

| 2018 | 0.396047 | 0.350657 | 0.160186 | 0.069996 | 0.023114 |

| 2019 | 0.383103 | 0.354131 | 0.170491 | 0.069931 | 0.022344 |

| 2020 | 0.370062 | 0.35783 | 0.179573 | 0.070893 | 0.021643 |

| 2021 | 0.359681 | 0.358971 | 0.188598 | 0.071481 | 0.021268 |

| 2022 | 0.351517 | 0.357176 | 0.198161 | 0.072378 | 0.020768 |

| 2023 | 0.346011 | 0.353269 | 0.206843 | 0.073669 | 0.020208 |

Furthermore, the number of centenarians has been increasing between plan years 2011 and 2023. Figure 6 shows that the number of centenarians as the percentage of the non-disabled population aged 50 and over gradually increased from 0.01% in plan year 2011 to 0.09% in plan year 2023 for males and from 0.01% to 0.12% for females. The average age of male centenarians increased from 100.8 years in plan year 2011 to 101.2 in plan year 2023 while the average age of female centenarians dropped slightly from 101.6 years to 101.4 years during the same period.

Figure 6 - Text version

| 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Average Age Male Centenarian | 100.8 | 100.8 | 100.9 | 100.8 | 101.0 | 101.1 | 101.0 | 100.9 | 100.8 | 100.9 | 100.9 | 101.0 | 101.2 |

| Average Age Female Centenarian | 101.6 | 101.1 | 101.3 | 101.4 | 101.5 | 101.7 | 101.5 | 101.2 | 101.3 | 101.4 | 101.4 | 101.4 | 101.4 |

| % Male Centenarian | 0.01% | 0.01% | 0.02% | 0.04% | 0.04% | 0.04% | 0.04% | 0.05% | 0.05% | 0.06% | 0.08% | 0.09% | 0.09% |

| % Female Centenarian | 0.01% | 0.03% | 0.04% | 0.07% | 0.08% | 0.07% | 0.07% | 0.08% | 0.08% | 0.07% | 0.09% | 0.10% | 0.12% |

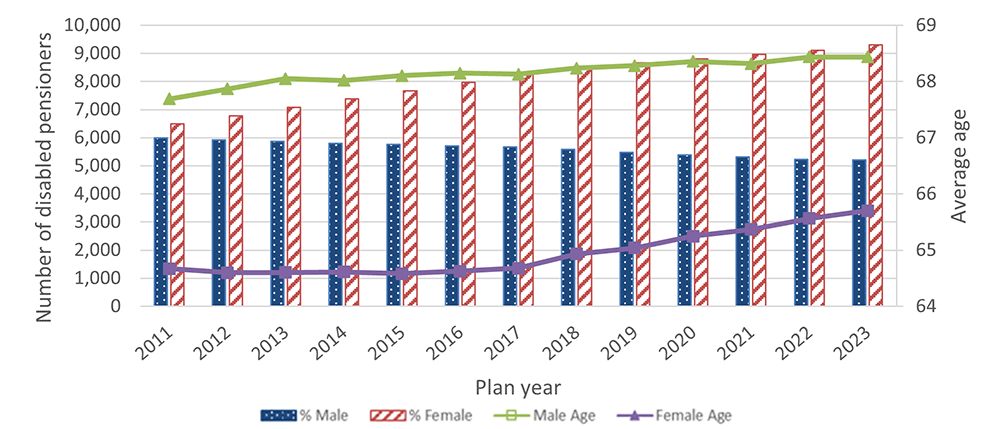

This study also includes an analysis of the mortality of disabled and surviving spouse populations. Figure 7 and Figure 8 show the evolutions of these populations over the past decade. Figure 7 shows the number of female disabled pensioners increased steadily while the number of male disabled pensioners declined. From plan years 2011 to 2023, the percentage of disabled male pensioners to total male members aged 50 and over decreased from 3.7% to 2.9%, while the percentage of disabled female members remained stable at around 5%. As the number of disabled female pensioners grew larger over time, the male-to-female ratio for the disabled populations declined from 0.9 in plan year 2011 to 0.6 in plan year 2023, indicating that females are more likely to become disabled than males. The average age for disabled pensioners increased from 67.7 years old in plan year 2011 to 68.4 years in plan year 2023 for males and from 64.7 years old to 65.7 years old for females.

Figure 7 - Text version

| 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Disabled Male | 5995 | 5920 | 5867 | 5804 | 5768 | 5716 | 5672 | 5581 | 5476 | 5387 | 5324 | 5223 | 5216 |

| Disabled Female | 6486 | 6781 | 7081 | 7377 | 7664 | 7964 | 8254 | 8458 | 8670 | 8809 | 8969 | 9107 | 9305 |

| Average Age Male Disabled | 67.7 | 67.9 | 68.0 | 68.0 | 68.1 | 68.1 | 68.1 | 68.2 | 68.3 | 68.4 | 68.3 | 68.4 | 68.4 |

| Average Age Female Disabled | 64.7 | 64.6 | 64.6 | 64.6 | 64.6 | 64.6 | 64.7 | 64.9 | 65.0 | 65.2 | 65.4 | 65.6 | 65.7 |

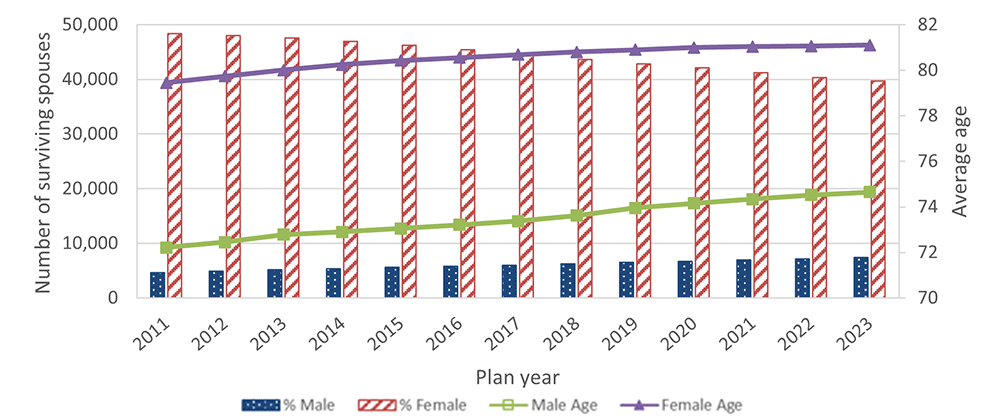

Figure 8 shows the opposite trend for the surviving spouse population. The number of female surviving spouses declined while the number of male surviving spouses increased. The annualized rate of growth of the male spouse population was 3.9% while the female spouse population shrank at the rate of −1.6%. As the number of male surviving spouses rose, the male-to-female ratio increased from 0.1 in plan year 2011 to 0.2 in plan year 2023.

The average age of the surviving spouses increased from 72.2 years old in plan year 2011 to 74.7 years old in plan year 2023 for males and from 79.4 to 81.1 years old for females, indicating that there are more older surviving spouses in plan year 2023 than in plan year 2011.

Figure 8 - Text version

| 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Male surviving spouse | 4637 | 4905 | 5129 | 5329 | 5592 | 5811 | 6013 | 6210 | 6470 | 6712 | 6938 | 7134 | 7367 |

| Female surviving spouse | 48375 | 48012 | 47584 | 46985 | 46218 | 45426 | 44586 | 43635 | 42832 | 42075 | 41225 | 40303 | 39694 |

| Male Average Age | 72.2 | 72.4 | 72.8 | 72.9 | 73.0 | 73.2 | 73.4 | 73.6 | 74.0 | 74.2 | 74.3 | 74.5 | 74.7 |

| Female Average Age | 79.4 | 79.7 | 80.0 | 80.2 | 80.4 | 80.6 | 80.7 | 80.8 | 80.9 | 81.0 | 81.0 | 81.1 | 81.1 |

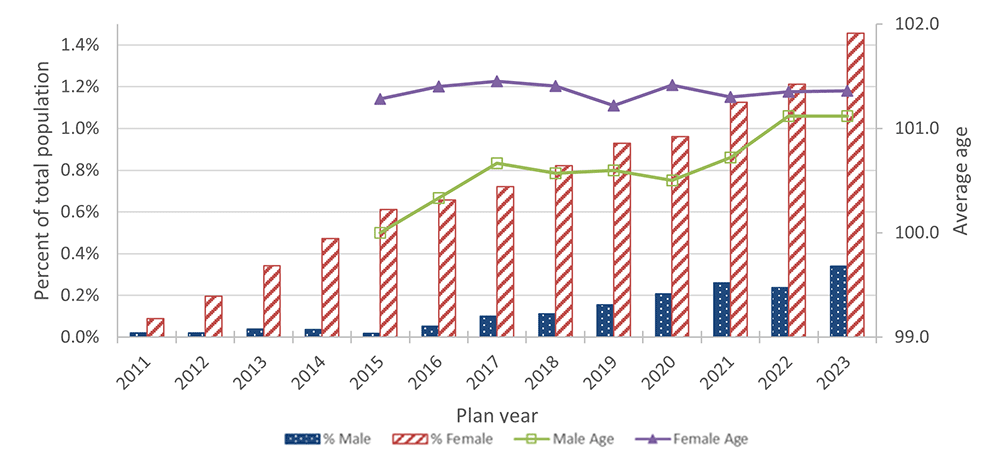

Similar to the non-disabled populations, the percentage of centenarians in the surviving spouse populations increased over the past 12 years. Figure 9 shows the progression of the increases for both genders from plan years 2011 to 2023. The female centenarian surviving spouse population had sharp growth during this period. The percentage of male centenarian surviving spouses increased from 0.02% in plan year 2011 to 0.34% in plan year 2023. It rose sharply for female surviving spouses, from 0.09% in 2011 to 1.46% in 2023. The proportion of both male and female centenarian surviving spouses increased by approximately the same multiple of 16. The average age of the centenarian surviving spouses increased from 100.0 years old in plan year 2015 to 101.1 years old in plan year 2023 for males and slightly decreased from 101.5 years old to 101.4 years old for females. The average ages of the centenarian surviving spouses are comparable to those of the non-disabled centenarians. Due to small data set prior to plan year 2015, only results from plan year 2015 are presented.

Figure 9 - Text version

| 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| % Male Centenarians | 0.02% | 0.02% | 0.04% | 0.04% | 0.02% | 0.05% | 0.10% | 0.11% | 0.15% | 0.21% | 0.26% | 0.24% | 0.34% |

| % Female Centenarians | 0.09% | 0.20% | 0.34% | 0.47% | 0.61% | 0.66% | 0.72% | 0.82% | 0.93% | 0.96% | 1.13% | 1.21% | 1.46% |

| Average age male centenarians | n/a | n/a | n/a | n/a | n/a | 100.3 | 100.7 | 100.6 | 100.6 | 100.5 | 100.7 | 101.1 | 101.1 |

| Average age female centenarians | n/a | n/a | n/a | n/a | n/a | 101.4 | 101.5 | 101.4 | 101.2 | 101.4 | 101.3 | 101.3 | 101.4 |

6 Mortality and life expectancy trends

6.1 Development of mortality rates

The mortality rates were calculated based on the mortality experience over three consecutive plan years to increase the number of exposures and to reduce the variability in the annual data. Therefore, while the period of study spanned from plan years 2011 to 2023, only mortality rates for plan years 2012 to 2022 could be derived. This method was also adopted in the development of the mortality rates for the 20th Actuarial Report on the Pension Plan for the Public Service of Canada as at 31 March 2023.

Mortality rate is defined as the number of deaths during the year divided by the population who was alive at the beginning of the year. The mortality rates for each plan year are estimated using the following four-step process.

6.1.1 Combine three annual data sets to one

Starting in plan year 2012 and ending in plan year 2022, for each plan year and each age, add the number of members who were alive at the beginning of the previous plan year, the current plan year, and the next plan year to arrive at the exposure of the current plan year (). That is:

, where

-

= total number of members who were alive on April 1 of plan year

-

= total number of members who were alive on April 1 of plan year

- = total number of members who were alive on April 1 of plan year .

For the same time period, for each plan year and each age, add the number of members who died during the previous plan year, the current plan year, and the next plan year to arrive at the total number of deaths of the current plan year (D). That is:

, where

-

= total number of deaths during plan year

-

= total number of deaths during plan year

-

= total number of deaths during plan year .

6.1.2 Calculate crude mortality rates

For each plan year and each age, the crude mortality rate is calculated by dividing by .

6.1.3 Graduate crude mortality rates

The crude mortality rates are then graduated to reflect a compromise between smoothness and fit. A Whittaker-Henderson graduation method is used to produce the graduated rates from age 50 to 95 for all populations, except surviving spouses. Due to limited data, the crude mortality rates for the surviving spouse population are graduated from age 60 to 95 for males and from age 55 to 95 for females. For the male surviving spouse population, the mortality rates from age 50 to 59 were linearly interpolated using the mortality rates of the non-disabled male members at age 50 as a starting point to the first graduated rate based on male surviving spouse population at age 60. Similarly, the mortality rates for female surviving spouses from age 50 to 54 are linearly interpolated using the mortality rates of the non-disabled female members at age 50 as a starting point to the first graduated rate at age 55.

6.1.4 Extend graduated mortality rates to age 115

Due to limited data beyond age 95, the mortality rates from age 96 to 105 are calculated using linear interpolation from mortality rate at age 95 determined as per Section 6.1.3 to age 106. Furthermore, the mortality rates at ages 106 to 114 are fixed at 0.5 and set to 1 at age 115.

6.2 Mortality rate trends

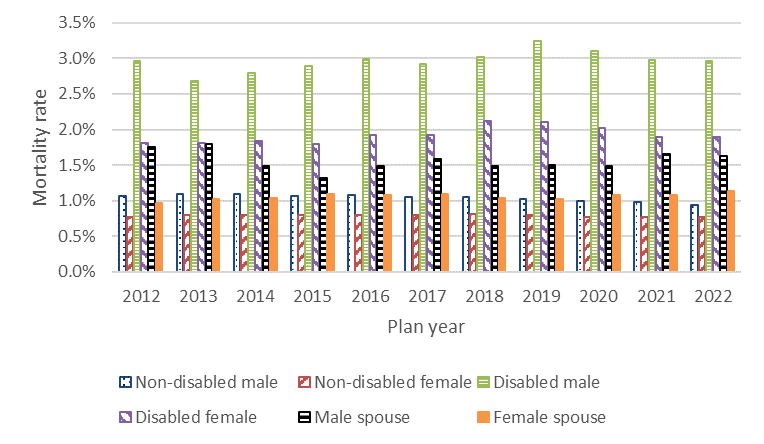

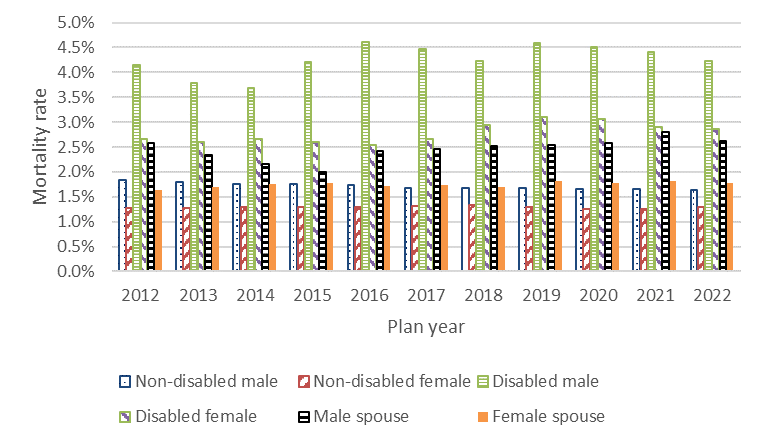

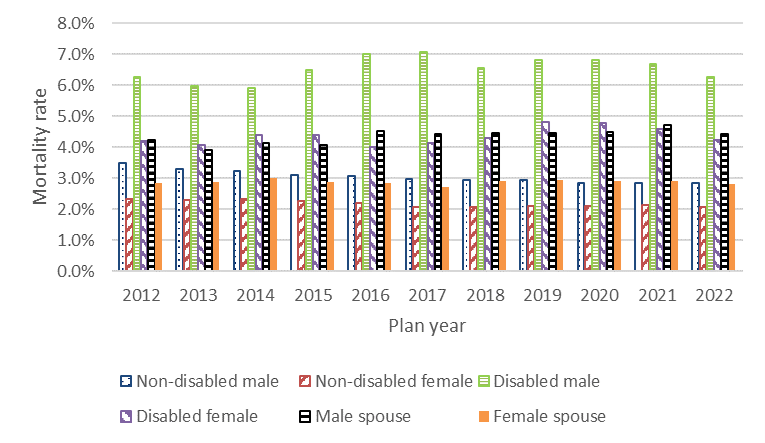

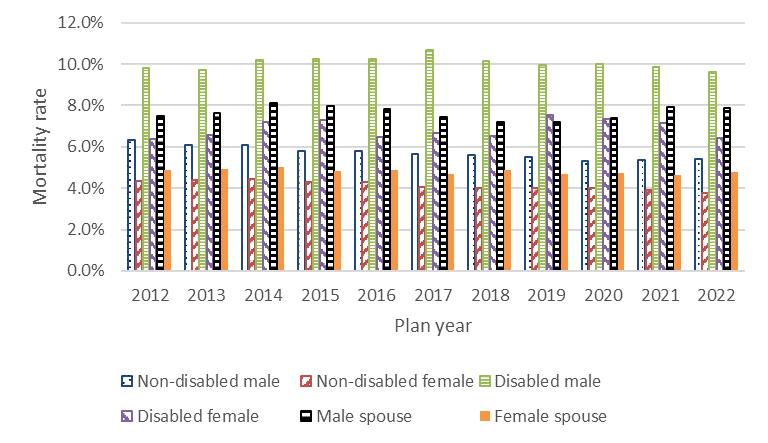

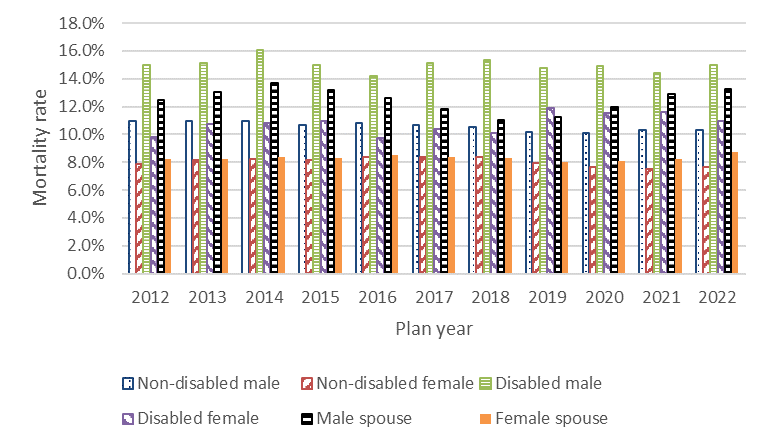

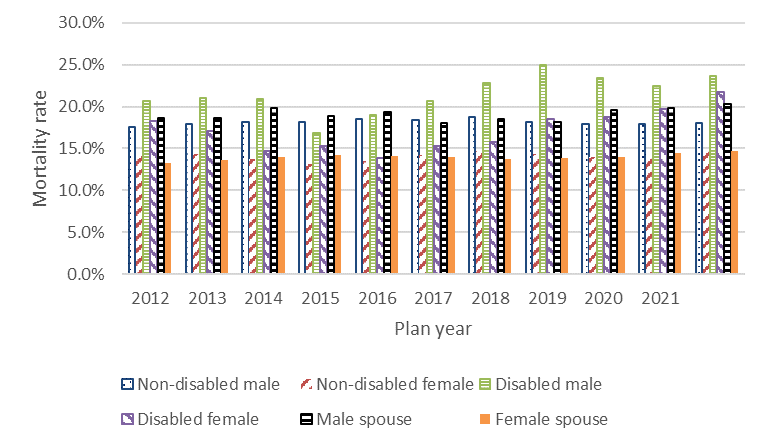

Figure 10 to Figure 15 show the evolutions of the mortality rates from plan years 2012 to 2022 for both genders for all three populations by age group. The complete mortality tables for all ages are provided in Appendix A. It can be seen from figures that the mortality rates for the non‑disabled populations generally gradually decreased from plan years 2012 to 2022 for both genders and all age groups. The disabled male pensioners had stable but highest mortality rates when compared to other populations throughout the period of study. The disabled female pensioners at age groups 65 to 74 had the second-highest mortality rates when compared to other populations. However, as age progresses, the mortality rates of the male surviving spouse rise at a faster rate and the male surviving spouse eventually becomes the population that has the second-highest mortality rates for age groups 80 to 89, except for plan year 2018. The male surviving spouses always had higher mortality rates than those of the non-disabled males up to age group 85 to 89. At age group 90 to 94, the male surviving spouses and non-disabled males had similar mortality rates. In contrast, the female surviving spouses had higher mortality rates than those of the non-disabled females up to age group 80 to 84. Starting at age group 85 to 89, the female surviving spouses and non-disabled females also had similar mortality rates.

Figure 10 - Text version

| 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Healthy Male Mortality Rate | 1.1% | 1.1% | 1.1% | 1.1% | 1.1% | 1.0% | 1.1% | 1.0% | 1.0% | 1.0% | 0.9% |

| Healthy Female Mortality Rate | 0.8% | 0.8% | 0.8% | 0.8% | 0.8% | 0.8% | 0.8% | 0.8% | 0.8% | 0.8% | 0.8% |

| Disabled Male Mortality Rate | 3.0% | 2.7% | 2.8% | 2.9% | 3.0% | 2.9% | 3.0% | 3.2% | 3.1% | 3.0% | 3.0% |

| Disabled Female Mortality Rate | 1.8% | 1.8% | 1.8% | 1.8% | 1.9% | 1.9% | 2.1% | 2.1% | 2.0% | 1.9% | 1.9% |

| Male Spouse Mortality Rate | 1.8% | 1.8% | 1.5% | 1.3% | 1.5% | 1.6% | 1.5% | 1.5% | 1.5% | 1.7% | 1.6% |

| Female Spouse Mortality Rate | 1.0% | 1.0% | 1.0% | 1.1% | 1.1% | 1.1% | 1.0% | 1.0% | 1.1% | 1.1% | 1.1% |

Figure 11 - Text version

| 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Healthy Male Mortality Rate | 1.8% | 1.8% | 1.8% | 1.8% | 1.7% | 1.7% | 1.7% | 1.7% | 1.7% | 1.7% | 1.6% |

| Healthy Female Mortality Rate | 1.3% | 1.3% | 1.3% | 1.3% | 1.3% | 1.3% | 1.3% | 1.3% | 1.2% | 1.3% | 1.3% |

| Disabled Male Mortality Rate | 4.2% | 3.8% | 3.7% | 4.2% | 4.6% | 4.5% | 4.2% | 4.6% | 4.5% | 4.4% | 4.2% |

| Disabled Female Mortality Rate | 2.7% | 2.6% | 2.7% | 2.6% | 2.5% | 2.7% | 3.0% | 3.1% | 3.1% | 2.9% | 2.9% |

| Male Spouse Mortality Rate | 2.6% | 2.3% | 2.2% | 2.0% | 2.4% | 2.5% | 2.5% | 2.5% | 2.6% | 2.8% | 2.6% |

| Female Spouse Mortality Rate | 1.6% | 1.7% | 1.8% | 1.8% | 1.7% | 1.7% | 1.7% | 1.8% | 1.8% | 1.8% | 1.8% |

Figure 12 - Text version

| 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Healthy Male Mortality Rate | 3.5% | 3.3% | 3.2% | 3.1% | 3.1% | 3.0% | 3.0% | 2.9% | 2.8% | 2.8% | 2.9% |

| Healthy Female Mortality Rate | 2.3% | 2.3% | 2.3% | 2.2% | 2.2% | 2.1% | 2.1% | 2.1% | 2.1% | 2.1% | 2.1% |

| Disabled Male Mortality Rate | 6.3% | 6.0% | 5.9% | 6.5% | 7.0% | 7.1% | 6.6% | 6.8% | 6.8% | 6.7% | 6.3% |

| Disabled Female Mortality Rate | 4.2% | 4.1% | 4.4% | 4.4% | 4.0% | 4.1% | 4.3% | 4.8% | 4.8% | 4.6% | 4.2% |

| Male Spouse Mortality Rate | 4.2% | 3.9% | 4.1% | 4.1% | 4.5% | 4.4% | 4.5% | 4.5% | 4.5% | 4.7% | 4.4% |

| Female Spouse Mortality Rate | 2.8% | 2.9% | 3.0% | 2.9% | 2.8% | 2.7% | 2.9% | 2.9% | 2.9% | 2.9% | 2.8% |

Figure 13 - Text version

| 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Healthy Male Mortality Rate | 6.3% | 6.1% | 6.1% | 5.8% | 5.8% | 5.7% | 5.6% | 5.5% | 5.3% | 5.4% | 5.4% |

| Healthy Female Mortality Rate | 4.3% | 4.4% | 4.4% | 4.3% | 4.3% | 4.1% | 4.0% | 4.0% | 4.0% | 3.9% | 3.7% |

| Disabled Male Mortality Rate | 9.8% | 9.7% | 10.2% | 10.3% | 10.2% | 10.7% | 10.2% | 9.9% | 10.0% | 9.9% | 9.6% |

| Disabled Female Mortality Rate | 6.4% | 6.6% | 7.2% | 7.3% | 6.5% | 6.7% | 6.5% | 7.5% | 7.3% | 7.2% | 6.4% |

| Male Spouse Mortality Rate | 7.5% | 7.6% | 8.1% | 8.0% | 7.8% | 7.4% | 7.2% | 7.2% | 7.4% | 7.9% | 7.9% |

| Female Spouse Mortality Rate | 4.9% | 4.9% | 5.0% | 4.8% | 4.9% | 4.7% | 4.9% | 4.7% | 4.7% | 4.6% | 4.8% |

Figure 14 - Text version

| 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Healthy Male Mortality Rate | 11.0% | 10.9% | 11.0% | 10.7% | 10.8% | 10.7% | 10.5% | 10.2% | 10.1% | 10.3% | 10.3% |

| Healthy Female Mortality Rate | 7.9% | 8.1% | 8.2% | 8.1% | 8.4% | 8.4% | 8.3% | 8.0% | 7.7% | 7.5% | 7.6% |

| Disabled Male Mortality Rate | 15.0% | 15.1% | 16.1% | 15.0% | 14.2% | 15.1% | 15.3% | 14.8% | 15.0% | 14.4% | 15.0% |

| Disabled Female Mortality Rate | 9.8% | 10.8% | 10.8% | 11.0% | 9.7% | 10.4% | 10.1% | 11.9% | 11.6% | 11.6% | 11.0% |

| Male Spouse Mortality Rate | 12.4% | 13.1% | 13.7% | 13.2% | 12.6% | 11.8% | 11.0% | 11.2% | 12.0% | 12.9% | 13.3% |

| Female Spouse Mortality Rate | 8.3% | 8.2% | 8.4% | 8.3% | 8.5% | 8.4% | 8.3% | 8.0% | 8.1% | 8.3% | 8.7% |

Figure 15 - Text version

| 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Healthy Male Mortality Rate | 17.6% | 17.9% | 18.1% | 18.1% | 18.5% | 18.4% | 18.7% | 18.1% | 17.9% | 17.9% | 18.0% |

| Healthy Female Mortality Rate | 14.3% | 14.3% | 13.8% | 13.2% | 13.5% | 14.3% | 14.6% | 14.4% | 13.9% | 14.1% | 14.9% |

| Disabled Male Mortality Rate | 20.7% | 21.1% | 20.9% | 16.9% | 19.0% | 20.7% | 22.8% | 25.0% | 23.4% | 22.5% | 23.7% |

| Disabled Female Mortality Rate | 18.3% | 17.1% | 14.7% | 15.3% | 13.8% | 15.3% | 15.8% | 18.5% | 18.7% | 19.8% | 21.8% |

| Male Spouse Mortality Rate | 18.6% | 18.6% | 19.9% | 18.8% | 19.4% | 18.0% | 18.5% | 18.1% | 19.6% | 19.8% | 20.3% |

| Female Spouse Mortality Rate | 13.3% | 13.6% | 14.0% | 14.2% | 14.1% | 14.0% | 13.7% | 13.9% | 14.0% | 14.4% | 14.7% |

In general, declining mortality rates over time implied positive longevity improvements. For example, the mortality rates of non-disabled males and non-disabled females age 65 to 69 have been generally decreasing over the past 12 years, resulting in 11-year average improvement rates for this age group of 1.5% for males and 0.3% for females. Table 7 shows the 11-year average longevity improvement factorsFootnote 4 by age group for all three populations. The non‑disabled populations have positive longevity improvements for all age groups except for the female age group 90 to 95. Disabled and surviving spouse populations experienced negative longevity improvements for most age groups. Appendix B provides complete 11‑year improvement factors for age 50 to 95 for all three groups.

| Age group | Contributors and non-disabled pensioners | Disabled pensioners | Surviving spouses | |||

|---|---|---|---|---|---|---|

| Male | Female | Male | Female | Male | Female | |

| 50‑54 | 2.6% | 3.3% | n/a | n/a | 3.9% | 2.3% |

| 55‑59 | 2.2% | 3.1% | n/a | 1.6% | 4.7% | −0.1% |

| 60‑64 | 1.7% | 1.5% | 0.5% | 1.0% | 3.9% | −1.0% |

| 65‑69 | 1.5% | 0.3% | −0.8% | −1.0% | 0.6% | −0.7% |

| 70‑74 | 1.2% | 0.0% | −1.4% | −1.8% | −1.7% | −0.7% |

| 75‑79 | 1.8% | 1.0% | −0.9% | −0.9% | −1.4% | −0.1% |

| 80‑84 | 1.7% | 1.5% | 0.2% | −0.4% | 0.1% | 0.5% |

| 85‑89 | 0.7% | 0.6% | 0.4% | −1.2% | 0.6% | 0.0% |

| 90‑95 | 0.1% | −0.1% | −2.3% | −2.4% | −0.4% | −0.3% |

6.3 Life expectancy trends

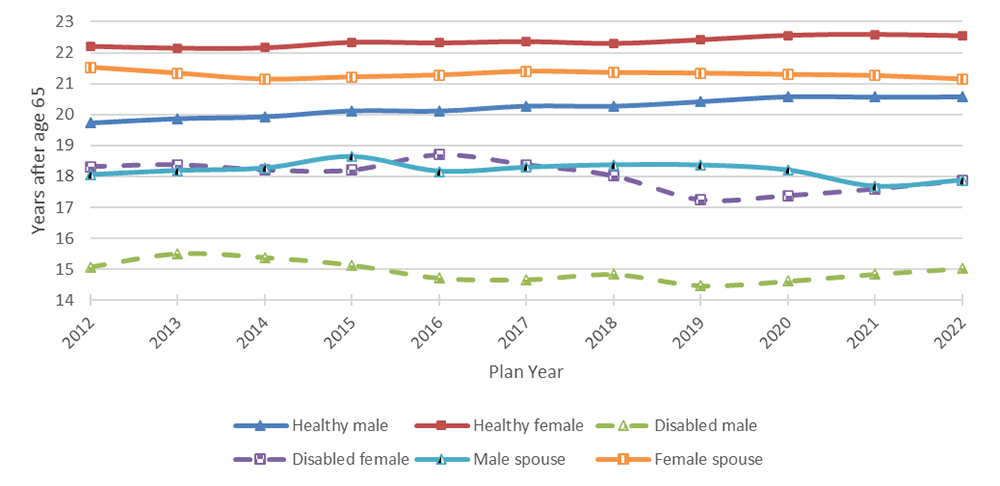

As a result of positive longevity improvement over the past 12 years for the non-disabled population, the period life expectancies at age 65 increased from 19.7 years in plan year 2012 to 20.6 years in plan year 2022 for males and from 22.2 years to 22.5 years for females. For the disabled pensioners, the period life expectancy at age 65 slightly decreased from 15.1 years to 15.0 years for males and from 18.3 years to 17.9 years for females. For the surviving spouse population, the period life expectancy at age 65 decreased from 18.1 years to 17.9 years for males and from 21.5 to 21.1 years for females. Figure 16 show the evolutions of period life expectancies at age 65 for both genders for all three groups from plan years 2012 to 2022.

In plan year 2022, a non-disabled member has longer period life expectancy at age 65 than a disabled pensioner by 5.6 years for males and 4.7 years for females. Similarly, a surviving spouse has shorter period life expectancy at age 65 than a non‑disabled member by 2.7 years for males and 1.4 years for females. Non‑disabled populations have longer period life expectancy at age 65 than the surviving spouse populations could partially be explained by a common phenomenon known as the "widowhood effect"Footnote 5 and a possible correlation between the mortality of the members and their spouses. Such correlation comes from the fact that the surviving spouses are potentially exposed to the same lifestyles and environmental factors that cause early deaths in the members, thereby leading the surviving spouse populations to have lower life expectancy.

Figure 16 - Text version

| 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Healthy male | 19.7 | 19.9 | 19.9 | 20.1 | 20.1 | 20.3 | 20.3 | 20.4 | 20.6 | 20.6 | 20.6 |

| Healthy female | 22.2 | 22.1 | 22.2 | 22.3 | 22.3 | 22.4 | 22.3 | 22.4 | 22.6 | 22.6 | 22.5 |

| Disabled male | 15.1 | 15.5 | 15.4 | 15.1 | 14.7 | 14.7 | 14.8 | 14.5 | 14.6 | 14.8 | 15.0 |

| Disabled female | 18.3 | 18.4 | 18.2 | 18.2 | 18.7 | 18.4 | 18.0 | 17.3 | 17.4 | 17.6 | 17.9 |

| Surviving spouse male | 18.1 | 18.2 | 18.3 | 18.6 | 18.2 | 18.3 | 18.4 | 18.4 | 18.2 | 17.7 | 17.9 |

| Surviving spouse female | 21.5 | 21.3 | 21.1 | 21.2 | 21.3 | 21.4 | 21.4 | 21.3 | 21.3 | 21.3 | 21.1 |

7 Comparison of PSPP mortality rates with other publicly available sources

This section compares life expectancies of non-disabled population at age 65 in 2021 to those of the:

- Canadian pensioners from the Canadian Pensioners' Mortality (CPM) tables (public, private and combined sectors)

- Canadian population (CAN)Footnote 6

- US population (US)Footnote 7

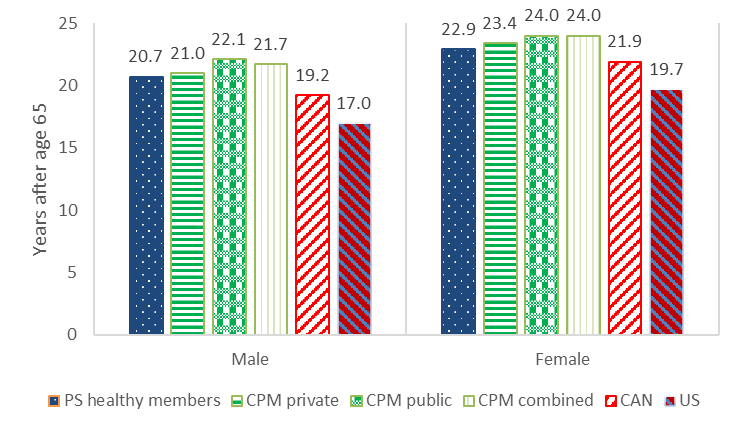

To account for the fact that different actuarial reports and mortality tables were produced at different times, and for purposes of comparability, the PSPP mortality rates are recalculated using data compiled as at January 1 instead of March 31, so that the period life expectancies are on the same time base as those for other populations.Figure 17 shows period life expectancies at age 65 in 2021 of the non-disabled population of the PSPP, the Canadian pensioners, the Canadian population, and the US population. The CPM tables for the public sector produced the highest life expectancies for both genders. Similar to the results found in the Pension Plan for the Public Service of Canada Mortality Study, Actuarial Study No. 14, the period life expectancies of non-disabled members were closer to those from the CPM private mortality tables despite the fact that the PSPP is a public pension plan. Since the Actuarial Study No. 14 publication, the gaps in life expectancies between the PSPP non-disabled population and the Canadian pensioners from the CPM private tables narrowed from 0.4 years (19.8 vs. 19.4) to −0.3 years (20.7 vs. 21.0) for males and widened from −0.2 years (22.2 vs. 22.4) to −0.5 years (22.9 vs. 23.4) for females. The negative gaps indicate that the actual longevity improvements of the non-disabled population are less than those used in the Canadian Institute of Actuaries' CPM-B improvement scale.

Figure 17 - Text version

| Male | Female | |

|---|---|---|

| PS healthy members | 20.7 | 22.9 |

| CPM private | 21 | 23.4 |

| CPM public | 22.1 | 24 |

| CPM combined | 21.7 | 24 |

| CAN | 19.2 | 21.9 |

| US | 17 | 19.7 |

8 Impact of COVID‑19

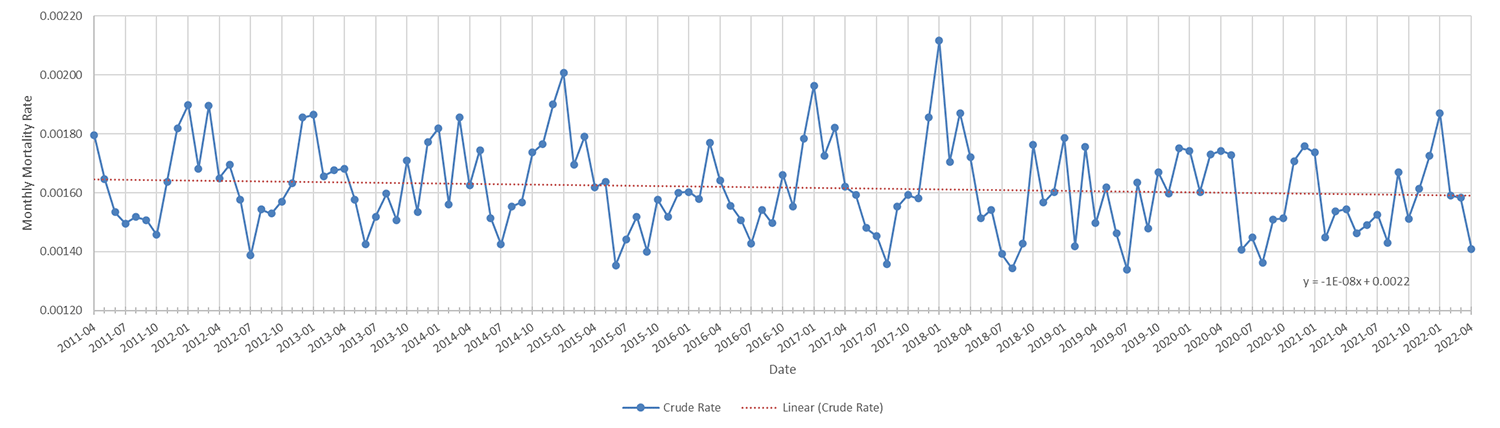

The data used in this study does not contain the causes of deaths therefore any observations made regarding mortality rates in this study does not imply causation of the emergence of COVID‑19. However, COVID-19 was first reported to the World Health Organization China Country Office on December 31, 2019,Footnote 8 and Canada had its first confirmed case on January 25, 2020, therefore the mortality rates in plan years 2021 and 2022 coincide with the time period of the emergence of COVID-19.Footnote 9 Figure 18 shows the fluctuations in the monthly mortality rates over the period of the study. The monthly mortality rates exhibit annual seasonality with relatively high mortality in the months of December, January, and March. These months coincide with the time of influenza seasons in the northern hemisphere. The trend line with negative slope indicates gains in mortality improvement over time. It can be observed that the mortality rates for winter months during years 2021 and 2022 were slightly higher than the recent past but were not as high as the mortality rates during the severe influenza seasons like those in 2014-2015Footnote 10 and 2017-2018.Footnote 11 Furthermore, the mortality rates during the summer months for plan years 2021 and 2022 were not as low as what have been in the recent past.

Figure 18 - Text version

Trend line equation:

| Date (yyyy-mm-dd) | Rate |

|---|---|

| 2011-04-01 | 0.00179 |

| 2011-05-01 | 0.00165 |

| 2011-06-01 | 0.00153 |

| 2011-07-01 | 0.0015 |

| 2011-08-01 | 0.00152 |

| 2011-09-01 | 0.00151 |

| 2011-10-01 | 0.00146 |

| 2011-11-01 | 0.00164 |

| 2011-12-01 | 0.00182 |

| 2012-01-01 | 0.0019 |

| 2012-02-01 | 0.00168 |

| 2012-03-01 | 0.0019 |

| 2012-04-01 | 0.00165 |

| 2012-05-01 | 0.00169 |

| 2012-06-01 | 0.00158 |

| 2012-07-01 | 0.00139 |

| 2012-08-01 | 0.00154 |

| 2012-09-01 | 0.00153 |

| 2012-10-01 | 0.00157 |

| 2012-11-01 | 0.00163 |

| 2012-12-01 | 0.00186 |

| 2013-01-01 | 0.00186 |

| 2013-02-01 | 0.00166 |

| 2013-03-01 | 0.00168 |

| 2013-04-01 | 0.00168 |

| 2013-05-01 | 0.00158 |

| 2013-06-01 | 0.00143 |

| 2013-07-01 | 0.00152 |

| 2013-08-01 | 0.0016 |

| 2013-09-01 | 0.00151 |

| 2013-10-01 | 0.00171 |

| 2013-11-01 | 0.00154 |

| 2013-12-01 | 0.00177 |

| 2014-01-01 | 0.00182 |

| 2014-02-01 | 0.00156 |

| 2014-03-01 | 0.00186 |

| 2014-04-01 | 0.00162 |

| 2014-05-01 | 0.00174 |

| 2014-06-01 | 0.00151 |

| 2014-07-01 | 0.00143 |

| 2014-08-01 | 0.00155 |

| 2014-09-01 | 0.00157 |

| 2014-10-01 | 0.00174 |

| 2014-11-01 | 0.00177 |

| 2014-12-01 | 0.0019 |

| 2015-01-01 | 0.00201 |

| 2015-02-01 | 0.00169 |

| 2015-03-01 | 0.00179 |

| 2015-04-01 | 0.00162 |

| 2015-05-01 | 0.00164 |

| 2015-06-01 | 0.00135 |

| 2015-07-01 | 0.00144 |

| 2015-08-01 | 0.00152 |

| 2015-09-01 | 0.0014 |

| 2015-10-01 | 0.00158 |

| 2015-11-01 | 0.00152 |

| 2015-12-01 | 0.0016 |

| 2016-01-01 | 0.0016 |

| 2016-02-01 | 0.00158 |

| 2016-03-01 | 0.00177 |

| 2016-04-01 | 0.00164 |

| 2016-05-01 | 0.00156 |

| 2016-06-01 | 0.00151 |

| 2016-07-01 | 0.00143 |

| 2016-08-01 | 0.00154 |

| 2016-09-01 | 0.0015 |

| 2016-10-01 | 0.00166 |

| 2016-11-01 | 0.00155 |

| 2016-12-01 | 0.00178 |

| 2017-01-01 | 0.00196 |

| 2017-02-01 | 0.00173 |

| 2017-03-01 | 0.00182 |

| 2017-04-01 | 0.00162 |

| 2017-05-01 | 0.00159 |

| 2017-06-01 | 0.00148 |

| 2017-07-01 | 0.00145 |

| 2017-08-01 | 0.00136 |

| 2017-09-01 | 0.00155 |

| 2017-10-01 | 0.00159 |

| 2017-11-01 | 0.00158 |

| 2017-12-01 | 0.00186 |

| 2018-01-01 | 0.00212 |

| 2018-02-01 | 0.0017 |

| 2018-03-01 | 0.00187 |

| 2018-04-01 | 0.00172 |

| 2018-05-01 | 0.00151 |

| 2018-06-01 | 0.00154 |

| 2018-07-01 | 0.00139 |

| 2018-08-01 | 0.00134 |

| 2018-09-01 | 0.00143 |

| 2018-10-01 | 0.00176 |

| 2018-11-01 | 0.00157 |

| 2018-12-01 | 0.0016 |

| 2019-01-01 | 0.00179 |

| 2019-02-01 | 0.00142 |

| 2019-03-01 | 0.00176 |

| 2019-04-01 | 0.0015 |

| 2019-05-01 | 0.00162 |

| 2019-06-01 | 0.00146 |

| 2019-07-01 | 0.00134 |

| 2019-08-01 | 0.00163 |

| 2019-09-01 | 0.00148 |

| 2019-10-01 | 0.00167 |

| 2019-11-01 | 0.0016 |

| 2019-12-01 | 0.00175 |

| 2020-01-01 | 0.00174 |

| 2020-02-01 | 0.0016 |

| 2020-03-01 | 0.00173 |

| 2020-04-01 | 0.00174 |

| 2020-05-01 | 0.00173 |

| 2020-06-01 | 0.00141 |

| 2020-07-01 | 0.00145 |

| 2020-08-01 | 0.00136 |

| 2020-09-01 | 0.00151 |

| 2020-10-01 | 0.00151 |

| 2020-11-01 | 0.00171 |

| 2020-12-01 | 0.00176 |

| 2021-01-01 | 0.00174 |

| 2021-02-01 | 0.00145 |

| 2021-03-01 | 0.00154 |

| 2021-04-01 | 0.00155 |

| 2021-05-01 | 0.00146 |

| 2021-06-01 | 0.00149 |

| 2021-07-01 | 0.00153 |

| 2021-08-01 | 0.00143 |

| 2021-09-01 | 0.00167 |

| 2021-10-01 | 0.00151 |

| 2021-11-01 | 0.00161 |

| 2021-12-01 | 0.00173 |

| 2022-01-01 | 0.00187 |

| 2022-02-01 | 0.00159 |

| 2022-03-01 | 0.00158 |

| 2022-04-01 | 0.00141 |

9 Conclusion

Over the past 12 years, the populations in the PSPP increased and evolved.

- All populations have positive growth rates, except for the disabled male and surviving spouse populations.

- The male-female ratio for non-disabled population reached parity.

- The average age for both genders for all populations increased.

- The percentage of centenarians increased for non-disabled and surviving spouse populations. However, the plan's experience in this regard cannot be reflected in mortality rates, as the data is not credible after age 95.

- Period life expectancy at age 65 for non-disabled members is salary-sensitive.

- Period life expectancy at age 65 for non-disabled population has improved, while it has remained stable or slightly deteriorated for other populations.

- Mortality improvement was lower than anticipated by the Canadian Institute of Actuaries' CPM-B improvement scale.

As demonstrated throughout this report, the three populations have different profiles, therefore it continues to be appropriate for the mortality rates in the 20th Actuarial Report on the PSPP to be separately analyzed. Furthermore, for valuation purposes, it remains appropriate for the mortality rates to be weighted by salary since it was first considered for the actuarial valuation as at 31 March 2017. Last, given a limited amount of data and the complexity of the modeling process for the longevity improvement rates as well as the majority of the members in the PSPP are from the non-disabled population, it also continues to be appropriate for all three populations to have the same assumed longevity improvement rates.

There are countless number of unknowns and unpredictable events that can impact mortality in a material way. Another looming mortality driver that is worth an investigation of its impact is climate change. Climate change may inflict a downside risk on future populations' longevity by stalling the progress of longevity improvement factors or even increasing mortality rates due to the emergence of new diseases and/or loss of lives by way of natural disasters. As the issue of climate change intensifies, its impact on the PSPP mortality can be included in the next study.

Appendix - A Detailed tables by age, year, and sex

| Age | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 50 | 0.0018 | 0.0017 | 0.0015 | 0.0013 | 0.0012 | 0.0011 | 0.0010 | 0.0012 | 0.0014 | 0.0014 | 0.0014 |

| 51 | 0.0019 | 0.0018 | 0.0017 | 0.0015 | 0.0014 | 0.0013 | 0.0013 | 0.0013 | 0.0014 | 0.0016 | 0.0015 |

| 52 | 0.0020 | 0.0019 | 0.0019 | 0.0016 | 0.0016 | 0.0014 | 0.0015 | 0.0014 | 0.0015 | 0.0016 | 0.0017 |

| 53 | 0.0022 | 0.0021 | 0.0021 | 0.0019 | 0.0018 | 0.0016 | 0.0017 | 0.0016 | 0.0017 | 0.0017 | 0.0017 |

| 54 | 0.0025 | 0.0022 | 0.0023 | 0.0021 | 0.0021 | 0.0018 | 0.0020 | 0.0019 | 0.0019 | 0.0019 | 0.0018 |

| 55 | 0.0027 | 0.0025 | 0.0026 | 0.0024 | 0.0024 | 0.0021 | 0.0023 | 0.0022 | 0.0022 | 0.0021 | 0.0020 |

| 56 | 0.0031 | 0.0028 | 0.0030 | 0.0028 | 0.0028 | 0.0025 | 0.0026 | 0.0026 | 0.0025 | 0.0024 | 0.0023 |

| 57 | 0.0034 | 0.0032 | 0.0033 | 0.0033 | 0.0032 | 0.0030 | 0.0030 | 0.0030 | 0.0029 | 0.0028 | 0.0026 |

| 58 | 0.0038 | 0.0036 | 0.0038 | 0.0038 | 0.0037 | 0.0036 | 0.0035 | 0.0035 | 0.0033 | 0.0033 | 0.0031 |

| 59 | 0.0043 | 0.0042 | 0.0044 | 0.0043 | 0.0042 | 0.0042 | 0.0040 | 0.0041 | 0.0038 | 0.0038 | 0.0036 |

| 60 | 0.0049 | 0.0048 | 0.0050 | 0.0049 | 0.0048 | 0.0049 | 0.0047 | 0.0047 | 0.0044 | 0.0043 | 0.0041 |

| 61 | 0.0055 | 0.0055 | 0.0057 | 0.0056 | 0.0055 | 0.0056 | 0.0053 | 0.0054 | 0.0050 | 0.0049 | 0.0047 |

| 62 | 0.0062 | 0.0063 | 0.0064 | 0.0063 | 0.0063 | 0.0063 | 0.0061 | 0.0061 | 0.0056 | 0.0055 | 0.0053 |

| 63 | 0.0069 | 0.0072 | 0.0073 | 0.0071 | 0.0071 | 0.0071 | 0.0069 | 0.0068 | 0.0063 | 0.0062 | 0.0060 |

| 64 | 0.0078 | 0.0081 | 0.0081 | 0.0079 | 0.0079 | 0.0078 | 0.0077 | 0.0076 | 0.0071 | 0.0069 | 0.0067 |

| 65 | 0.0087 | 0.0090 | 0.0090 | 0.0088 | 0.0088 | 0.0086 | 0.0086 | 0.0084 | 0.0079 | 0.0077 | 0.0075 |

| 66 | 0.0096 | 0.0100 | 0.0100 | 0.0097 | 0.0098 | 0.0095 | 0.0095 | 0.0092 | 0.0088 | 0.0086 | 0.0084 |

| 67 | 0.0107 | 0.0110 | 0.0110 | 0.0107 | 0.0108 | 0.0104 | 0.0105 | 0.0102 | 0.0098 | 0.0097 | 0.0094 |

| 68 | 0.0118 | 0.0121 | 0.0120 | 0.0118 | 0.0119 | 0.0114 | 0.0115 | 0.0112 | 0.0109 | 0.0108 | 0.0104 |

| 69 | 0.0131 | 0.0132 | 0.0132 | 0.0130 | 0.0130 | 0.0125 | 0.0126 | 0.0123 | 0.0121 | 0.0120 | 0.0117 |

| 70 | 0.0146 | 0.0145 | 0.0144 | 0.0143 | 0.0143 | 0.0137 | 0.0139 | 0.0136 | 0.0134 | 0.0134 | 0.0130 |

| 71 | 0.0163 | 0.0160 | 0.0158 | 0.0158 | 0.0157 | 0.0151 | 0.0152 | 0.0150 | 0.0149 | 0.0149 | 0.0145 |

| 72 | 0.0183 | 0.0178 | 0.0175 | 0.0175 | 0.0173 | 0.0168 | 0.0168 | 0.0167 | 0.0165 | 0.0165 | 0.0162 |

| 73 | 0.0206 | 0.0199 | 0.0195 | 0.0194 | 0.0192 | 0.0187 | 0.0186 | 0.0186 | 0.0183 | 0.0183 | 0.0181 |

| 74 | 0.0234 | 0.0224 | 0.0218 | 0.0216 | 0.0213 | 0.0208 | 0.0208 | 0.0207 | 0.0203 | 0.0203 | 0.0202 |

| 75 | 0.0266 | 0.0254 | 0.0246 | 0.0242 | 0.0239 | 0.0233 | 0.0232 | 0.0232 | 0.0226 | 0.0226 | 0.0226 |

| 76 | 0.0303 | 0.0288 | 0.0280 | 0.0272 | 0.0269 | 0.0262 | 0.0261 | 0.0261 | 0.0253 | 0.0252 | 0.0253 |

| 77 | 0.0345 | 0.0328 | 0.0319 | 0.0307 | 0.0303 | 0.0295 | 0.0295 | 0.0294 | 0.0284 | 0.0282 | 0.0285 |

| 78 | 0.0393 | 0.0373 | 0.0364 | 0.0348 | 0.0344 | 0.0333 | 0.0334 | 0.0332 | 0.0319 | 0.0318 | 0.0322 |

| 79 | 0.0446 | 0.0424 | 0.0416 | 0.0395 | 0.0391 | 0.0378 | 0.0379 | 0.0376 | 0.0361 | 0.0360 | 0.0365 |

| 80 | 0.0505 | 0.0481 | 0.0475 | 0.0449 | 0.0446 | 0.0431 | 0.0431 | 0.0426 | 0.0410 | 0.0410 | 0.0415 |

| 81 | 0.0570 | 0.0545 | 0.0541 | 0.0511 | 0.0508 | 0.0492 | 0.0491 | 0.0484 | 0.0468 | 0.0468 | 0.0474 |

| 82 | 0.0641 | 0.0615 | 0.0613 | 0.0581 | 0.0580 | 0.0563 | 0.0561 | 0.0550 | 0.0534 | 0.0537 | 0.0542 |

| 83 | 0.0718 | 0.0694 | 0.0694 | 0.0661 | 0.0662 | 0.0645 | 0.0640 | 0.0625 | 0.0610 | 0.0615 | 0.0620 |

| 84 | 0.0802 | 0.0780 | 0.0782 | 0.0750 | 0.0754 | 0.0739 | 0.0731 | 0.0711 | 0.0697 | 0.0706 | 0.0709 |

| 85 | 0.0894 | 0.0876 | 0.0878 | 0.0849 | 0.0858 | 0.0846 | 0.0834 | 0.0808 | 0.0796 | 0.0808 | 0.0810 |

| 86 | 0.0995 | 0.0982 | 0.0984 | 0.0959 | 0.0972 | 0.0964 | 0.0949 | 0.0917 | 0.0906 | 0.0922 | 0.0924 |

| 87 | 0.1105 | 0.1099 | 0.1101 | 0.1081 | 0.1098 | 0.1095 | 0.1077 | 0.1039 | 0.1029 | 0.1048 | 0.1050 |

| 88 | 0.1227 | 0.1228 | 0.1229 | 0.1214 | 0.1236 | 0.1237 | 0.1219 | 0.1174 | 0.1165 | 0.1186 | 0.1188 |

| 89 | 0.1361 | 0.1369 | 0.1370 | 0.1360 | 0.1386 | 0.1389 | 0.1374 | 0.1324 | 0.1314 | 0.1336 | 0.1340 |

| 90 | 0.1510 | 0.1525 | 0.1525 | 0.1518 | 0.1547 | 0.1551 | 0.1543 | 0.1488 | 0.1477 | 0.1498 | 0.1505 |

| 91 | 0.1676 | 0.1695 | 0.1697 | 0.1689 | 0.1720 | 0.1721 | 0.1725 | 0.1668 | 0.1654 | 0.1672 | 0.1683 |

| 92 | 0.1862 | 0.1881 | 0.1887 | 0.1874 | 0.1905 | 0.1897 | 0.1920 | 0.1864 | 0.1846 | 0.1856 | 0.1874 |

| 93 | 0.2069 | 0.2083 | 0.2097 | 0.2073 | 0.2100 | 0.2079 | 0.2129 | 0.2076 | 0.2053 | 0.2052 | 0.2078 |

| 94 | 0.2301 | 0.2303 | 0.2329 | 0.2286 | 0.2306 | 0.2265 | 0.2352 | 0.2305 | 0.2276 | 0.2258 | 0.2296 |

| 95 | 0.2563 | 0.2542 | 0.2586 | 0.2514 | 0.2523 | 0.2453 | 0.2587 | 0.2552 | 0.2516 | 0.2475 | 0.2528 |

| 96 | 0.2784 | 0.2765 | 0.2806 | 0.2740 | 0.2748 | 0.2685 | 0.2806 | 0.2774 | 0.2742 | 0.2705 | 0.2753 |

| 97 | 0.3006 | 0.2989 | 0.3025 | 0.2966 | 0.2973 | 0.2916 | 0.3026 | 0.2997 | 0.2967 | 0.2934 | 0.2977 |

| 98 | 0.3227 | 0.3212 | 0.3245 | 0.3192 | 0.3199 | 0.3148 | 0.3245 | 0.3219 | 0.3193 | 0.3164 | 0.3202 |

| 99 | 0.3449 | 0.3436 | 0.3464 | 0.3418 | 0.3424 | 0.3379 | 0.3464 | 0.3442 | 0.3419 | 0.3393 | 0.3427 |

| 100 | 0.3671 | 0.3659 | 0.3683 | 0.3644 | 0.3649 | 0.3611 | 0.3684 | 0.3665 | 0.3645 | 0.3623 | 0.3652 |

| 101 | 0.3892 | 0.3883 | 0.3903 | 0.3870 | 0.3874 | 0.3842 | 0.3903 | 0.3887 | 0.3871 | 0.3852 | 0.3876 |

| 102 | 0.4114 | 0.4106 | 0.4122 | 0.4096 | 0.4099 | 0.4074 | 0.4122 | 0.4110 | 0.4097 | 0.4082 | 0.4101 |

| 103 | 0.4335 | 0.4330 | 0.4342 | 0.4322 | 0.4324 | 0.4305 | 0.4342 | 0.4332 | 0.4322 | 0.4311 | 0.4326 |

| 104 | 0.4557 | 0.4553 | 0.4561 | 0.4548 | 0.4550 | 0.4537 | 0.4561 | 0.4555 | 0.4548 | 0.4541 | 0.4551 |

| 105 | 0.4778 | 0.4777 | 0.4781 | 0.4774 | 0.4775 | 0.4768 | 0.4781 | 0.4777 | 0.4774 | 0.4770 | 0.4775 |

| 106 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 |

| 107 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 |

| 108 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 |

| 109 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 |

| 110 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 |

| 111 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 |

| 112 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 |

| 113 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 |

| 114 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 |

| 115 | 1.0000 | 1.0000 | 1.0000 | 1.0000 | 1.0000 | 1.0000 | 1.0000 | 1.0000 | 1.0000 | 1.0000 | 1.0000 |

| Age | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 50 | 0.0013 | 0.0013 | 0.0014 | 0.0011 | 0.0012 | 0.0010 | 0.0010 | 0.0010 | 0.0010 | 0.0012 | 0.0011 |

| 51 | 0.0015 | 0.0015 | 0.0015 | 0.0013 | 0.0013 | 0.0011 | 0.0012 | 0.0011 | 0.0012 | 0.0013 | 0.0012 |

| 52 | 0.0016 | 0.0016 | 0.0017 | 0.0015 | 0.0014 | 0.0013 | 0.0013 | 0.0012 | 0.0012 | 0.0013 | 0.0012 |

| 53 | 0.0018 | 0.0018 | 0.0019 | 0.0017 | 0.0015 | 0.0015 | 0.0014 | 0.0013 | 0.0013 | 0.0014 | 0.0013 |

| 54 | 0.0019 | 0.0020 | 0.0021 | 0.0019 | 0.0017 | 0.0017 | 0.0015 | 0.0015 | 0.0015 | 0.0015 | 0.0014 |

| 55 | 0.0021 | 0.0022 | 0.0023 | 0.0022 | 0.0020 | 0.0019 | 0.0017 | 0.0017 | 0.0017 | 0.0017 | 0.0015 |

| 56 | 0.0022 | 0.0024 | 0.0026 | 0.0025 | 0.0023 | 0.0022 | 0.0020 | 0.0020 | 0.0019 | 0.0019 | 0.0017 |

| 57 | 0.0025 | 0.0027 | 0.0029 | 0.0028 | 0.0026 | 0.0025 | 0.0023 | 0.0023 | 0.0022 | 0.0022 | 0.0019 |

| 58 | 0.0028 | 0.0031 | 0.0033 | 0.0032 | 0.0030 | 0.0029 | 0.0027 | 0.0027 | 0.0026 | 0.0025 | 0.0022 |

| 59 | 0.0031 | 0.0034 | 0.0037 | 0.0037 | 0.0034 | 0.0033 | 0.0031 | 0.0031 | 0.0030 | 0.0029 | 0.0026 |

| 60 | 0.0035 | 0.0039 | 0.0041 | 0.0042 | 0.0039 | 0.0037 | 0.0036 | 0.0036 | 0.0034 | 0.0034 | 0.0030 |

| 61 | 0.0040 | 0.0044 | 0.0046 | 0.0046 | 0.0044 | 0.0041 | 0.0041 | 0.0041 | 0.0039 | 0.0039 | 0.0035 |

| 62 | 0.0046 | 0.0049 | 0.0052 | 0.0052 | 0.0049 | 0.0046 | 0.0046 | 0.0046 | 0.0045 | 0.0044 | 0.0041 |

| 63 | 0.0051 | 0.0055 | 0.0057 | 0.0057 | 0.0054 | 0.0052 | 0.0052 | 0.0052 | 0.0051 | 0.0050 | 0.0047 |

| 64 | 0.0057 | 0.0061 | 0.0062 | 0.0062 | 0.0060 | 0.0058 | 0.0058 | 0.0058 | 0.0057 | 0.0056 | 0.0054 |

| 65 | 0.0064 | 0.0067 | 0.0068 | 0.0068 | 0.0066 | 0.0065 | 0.0065 | 0.0065 | 0.0063 | 0.0063 | 0.0061 |

| 66 | 0.0070 | 0.0074 | 0.0074 | 0.0074 | 0.0072 | 0.0072 | 0.0073 | 0.0072 | 0.0070 | 0.0070 | 0.0069 |

| 67 | 0.0077 | 0.0081 | 0.0081 | 0.0081 | 0.0080 | 0.0081 | 0.0082 | 0.0081 | 0.0078 | 0.0077 | 0.0078 |

| 68 | 0.0085 | 0.0088 | 0.0088 | 0.0089 | 0.0088 | 0.0090 | 0.0092 | 0.0089 | 0.0086 | 0.0086 | 0.0087 |

| 69 | 0.0094 | 0.0097 | 0.0097 | 0.0097 | 0.0097 | 0.0100 | 0.0102 | 0.0099 | 0.0095 | 0.0095 | 0.0096 |

| 70 | 0.0103 | 0.0105 | 0.0106 | 0.0107 | 0.0108 | 0.0111 | 0.0113 | 0.0109 | 0.0104 | 0.0104 | 0.0106 |

| 71 | 0.0115 | 0.0116 | 0.0117 | 0.0118 | 0.0119 | 0.0122 | 0.0125 | 0.0120 | 0.0115 | 0.0115 | 0.0117 |

| 72 | 0.0128 | 0.0127 | 0.0129 | 0.0130 | 0.0131 | 0.0133 | 0.0136 | 0.0132 | 0.0126 | 0.0127 | 0.0129 |

| 73 | 0.0143 | 0.0141 | 0.0144 | 0.0144 | 0.0145 | 0.0144 | 0.0147 | 0.0144 | 0.0139 | 0.0140 | 0.0142 |

| 74 | 0.0161 | 0.0157 | 0.0160 | 0.0159 | 0.0160 | 0.0156 | 0.0159 | 0.0157 | 0.0154 | 0.0155 | 0.0156 |

| 75 | 0.0181 | 0.0176 | 0.0180 | 0.0177 | 0.0177 | 0.0170 | 0.0172 | 0.0172 | 0.0170 | 0.0172 | 0.0171 |

| 76 | 0.0205 | 0.0199 | 0.0203 | 0.0198 | 0.0197 | 0.0186 | 0.0187 | 0.0189 | 0.0190 | 0.0192 | 0.0189 |

| 77 | 0.0232 | 0.0226 | 0.0230 | 0.0223 | 0.0220 | 0.0205 | 0.0206 | 0.0209 | 0.0212 | 0.0214 | 0.0208 |

| 78 | 0.0263 | 0.0258 | 0.0262 | 0.0253 | 0.0248 | 0.0230 | 0.0229 | 0.0234 | 0.0239 | 0.0240 | 0.0231 |

| 79 | 0.0298 | 0.0296 | 0.0299 | 0.0288 | 0.0282 | 0.0261 | 0.0258 | 0.0264 | 0.0270 | 0.0269 | 0.0257 |

| 80 | 0.0338 | 0.0338 | 0.0342 | 0.0330 | 0.0322 | 0.0300 | 0.0296 | 0.0301 | 0.0307 | 0.0304 | 0.0289 |

| 81 | 0.0382 | 0.0387 | 0.0391 | 0.0378 | 0.0371 | 0.0348 | 0.0343 | 0.0346 | 0.0350 | 0.0344 | 0.0328 |

| 82 | 0.0432 | 0.0441 | 0.0446 | 0.0434 | 0.0428 | 0.0406 | 0.0400 | 0.0399 | 0.0400 | 0.0391 | 0.0374 |

| 83 | 0.0488 | 0.0502 | 0.0508 | 0.0497 | 0.0494 | 0.0474 | 0.0468 | 0.0462 | 0.0458 | 0.0445 | 0.0430 |

| 84 | 0.0551 | 0.0569 | 0.0577 | 0.0567 | 0.0569 | 0.0554 | 0.0548 | 0.0535 | 0.0525 | 0.0509 | 0.0497 |

| 85 | 0.0621 | 0.0643 | 0.0652 | 0.0644 | 0.0653 | 0.0643 | 0.0639 | 0.0617 | 0.0600 | 0.0582 | 0.0576 |

| 86 | 0.0701 | 0.0726 | 0.0735 | 0.0728 | 0.0745 | 0.0742 | 0.0740 | 0.0710 | 0.0685 | 0.0666 | 0.0669 |

| 87 | 0.0792 | 0.0818 | 0.0826 | 0.0817 | 0.0844 | 0.0849 | 0.0851 | 0.0813 | 0.0780 | 0.0762 | 0.0776 |

| 88 | 0.0895 | 0.0920 | 0.0926 | 0.0913 | 0.0948 | 0.0964 | 0.0970 | 0.0925 | 0.0886 | 0.0870 | 0.0897 |

| 89 | 0.1013 | 0.1036 | 0.1034 | 0.1015 | 0.1057 | 0.1085 | 0.1096 | 0.1047 | 0.1002 | 0.0992 | 0.1033 |

| 90 | 0.1148 | 0.1166 | 0.1153 | 0.1122 | 0.1169 | 0.1209 | 0.1228 | 0.1178 | 0.1129 | 0.1127 | 0.1184 |

| 91 | 0.1304 | 0.1314 | 0.1282 | 0.1235 | 0.1281 | 0.1337 | 0.1362 | 0.1317 | 0.1268 | 0.1276 | 0.1349 |

| 92 | 0.1485 | 0.1483 | 0.1424 | 0.1355 | 0.1392 | 0.1465 | 0.1499 | 0.1466 | 0.1419 | 0.1440 | 0.1529 |

| 93 | 0.1694 | 0.1676 | 0.1580 | 0.1481 | 0.1499 | 0.1592 | 0.1636 | 0.1622 | 0.1582 | 0.1619 | 0.1723 |

| 94 | 0.1938 | 0.1898 | 0.1749 | 0.1613 | 0.1599 | 0.1717 | 0.1771 | 0.1786 | 0.1757 | 0.1814 | 0.1932 |

| 95 | 0.2223 | 0.2154 | 0.1934 | 0.1751 | 0.1691 | 0.1837 | 0.1902 | 0.1957 | 0.1946 | 0.2024 | 0.2154 |

| 96 | 0.2475 | 0.2413 | 0.2213 | 0.2047 | 0.1992 | 0.2125 | 0.2184 | 0.2234 | 0.2224 | 0.2294 | 0.2413 |

| 97 | 0.2728 | 0.2671 | 0.2492 | 0.2342 | 0.2293 | 0.2412 | 0.2465 | 0.2510 | 0.2502 | 0.2565 | 0.2672 |

| 98 | 0.2980 | 0.2930 | 0.2770 | 0.2637 | 0.2593 | 0.2700 | 0.2747 | 0.2787 | 0.2779 | 0.2835 | 0.2930 |

| 99 | 0.3233 | 0.3189 | 0.3049 | 0.2933 | 0.2894 | 0.2987 | 0.3029 | 0.3064 | 0.3057 | 0.3106 | 0.3189 |

| 100 | 0.3485 | 0.3448 | 0.3328 | 0.3228 | 0.3195 | 0.3275 | 0.3310 | 0.3340 | 0.3334 | 0.3377 | 0.3448 |

| 101 | 0.3738 | 0.3706 | 0.3607 | 0.3523 | 0.3496 | 0.3562 | 0.3592 | 0.3617 | 0.3612 | 0.3647 | 0.3707 |

| 102 | 0.3990 | 0.3965 | 0.3885 | 0.3819 | 0.3797 | 0.3850 | 0.3873 | 0.3893 | 0.3890 | 0.3918 | 0.3965 |

| 103 | 0.4243 | 0.4224 | 0.4164 | 0.4114 | 0.4098 | 0.4137 | 0.4155 | 0.4170 | 0.4167 | 0.4188 | 0.4224 |

| 104 | 0.4495 | 0.4483 | 0.4443 | 0.4409 | 0.4398 | 0.4425 | 0.4437 | 0.4447 | 0.4445 | 0.4459 | 0.4483 |

| 105 | 0.4748 | 0.4741 | 0.4721 | 0.4705 | 0.4699 | 0.4712 | 0.4718 | 0.4723 | 0.4722 | 0.4729 | 0.4741 |

| 106 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 |

| 107 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 |

| 108 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 |

| 109 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 |

| 110 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 |

| 111 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 |

| 112 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 |

| 113 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 |

| 114 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 |

| 115 | 1.0000 | 1.0000 | 1.0000 | 1.0000 | 1.0000 | 1.0000 | 1.0000 | 1.0000 | 1.0000 | 1.0000 | 1.0000 |

| Age | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 50 | 0.0097 | 0.0008 | 0.0112 | 0.0144 | 0.0109 | 0.0051 | 0.0052 | 0.0032 | 0.0105 | 0.0111 | 0.0101 |

| 51 | 0.0123 | 0.0104 | 0.0124 | 0.0147 | 0.0120 | 0.0103 | 0.0079 | 0.0055 | 0.0112 | 0.0114 | 0.0112 |

| 52 | 0.0144 | 0.0159 | 0.0135 | 0.0151 | 0.0130 | 0.0138 | 0.0103 | 0.0077 | 0.0120 | 0.0119 | 0.0122 |

| 53 | 0.0161 | 0.0189 | 0.0147 | 0.0155 | 0.0141 | 0.0160 | 0.0123 | 0.0097 | 0.0128 | 0.0124 | 0.0132 |

| 54 | 0.0174 | 0.0204 | 0.0157 | 0.0159 | 0.0151 | 0.0173 | 0.0142 | 0.0116 | 0.0136 | 0.0130 | 0.0142 |

| 55 | 0.0184 | 0.0211 | 0.0168 | 0.0165 | 0.0162 | 0.0181 | 0.0157 | 0.0134 | 0.0145 | 0.0136 | 0.0151 |

| 56 | 0.0192 | 0.0213 | 0.0179 | 0.0170 | 0.0172 | 0.0186 | 0.0171 | 0.0151 | 0.0155 | 0.0144 | 0.0161 |

| 57 | 0.0199 | 0.0213 | 0.0189 | 0.0177 | 0.0173 | 0.0189 | 0.0184 | 0.0166 | 0.0164 | 0.0152 | 0.0170 |

| 58 | 0.0205 | 0.0213 | 0.0199 | 0.0184 | 0.0176 | 0.0191 | 0.0195 | 0.0181 | 0.0174 | 0.0161 | 0.0179 |

| 59 | 0.0212 | 0.0213 | 0.0209 | 0.0192 | 0.0181 | 0.0195 | 0.0205 | 0.0196 | 0.0185 | 0.0171 | 0.0189 |

| 60 | 0.0218 | 0.0214 | 0.0218 | 0.0200 | 0.0188 | 0.0199 | 0.0215 | 0.0210 | 0.0196 | 0.0182 | 0.0199 |

| 61 | 0.0225 | 0.0217 | 0.0227 | 0.0210 | 0.0197 | 0.0205 | 0.0225 | 0.0224 | 0.0209 | 0.0193 | 0.0209 |

| 62 | 0.0233 | 0.0221 | 0.0236 | 0.0220 | 0.0208 | 0.0213 | 0.0235 | 0.0238 | 0.0222 | 0.0207 | 0.0220 |

| 63 | 0.0242 | 0.0227 | 0.0245 | 0.0232 | 0.0221 | 0.0223 | 0.0245 | 0.0253 | 0.0236 | 0.0221 | 0.0232 |

| 64 | 0.0253 | 0.0234 | 0.0253 | 0.0244 | 0.0237 | 0.0236 | 0.0257 | 0.0268 | 0.0251 | 0.0237 | 0.0245 |

| 65 | 0.0266 | 0.0243 | 0.0261 | 0.0258 | 0.0255 | 0.0251 | 0.0269 | 0.0285 | 0.0268 | 0.0254 | 0.0259 |

| 66 | 0.0280 | 0.0255 | 0.0270 | 0.0273 | 0.0275 | 0.0269 | 0.0283 | 0.0303 | 0.0287 | 0.0274 | 0.0276 |

| 67 | 0.0295 | 0.0268 | 0.0280 | 0.0291 | 0.0298 | 0.0290 | 0.0300 | 0.0323 | 0.0308 | 0.0295 | 0.0294 |

| 68 | 0.0313 | 0.0284 | 0.0291 | 0.0310 | 0.0324 | 0.0315 | 0.0318 | 0.0345 | 0.0332 | 0.0319 | 0.0314 |

| 69 | 0.0334 | 0.0302 | 0.0304 | 0.0332 | 0.0353 | 0.0342 | 0.0340 | 0.0370 | 0.0358 | 0.0345 | 0.0337 |

| 70 | 0.0356 | 0.0323 | 0.0319 | 0.0356 | 0.0385 | 0.0373 | 0.0364 | 0.0398 | 0.0387 | 0.0374 | 0.0362 |

| 71 | 0.0382 | 0.0347 | 0.0339 | 0.0384 | 0.0420 | 0.0408 | 0.0392 | 0.0428 | 0.0419 | 0.0406 | 0.0391 |

| 72 | 0.0411 | 0.0376 | 0.0363 | 0.0416 | 0.0458 | 0.0447 | 0.0424 | 0.0462 | 0.0454 | 0.0441 | 0.0422 |

| 73 | 0.0444 | 0.0408 | 0.0393 | 0.0452 | 0.0499 | 0.0489 | 0.0460 | 0.0499 | 0.0492 | 0.0480 | 0.0456 |

| 74 | 0.0482 | 0.0446 | 0.0430 | 0.0493 | 0.0544 | 0.0536 | 0.0501 | 0.0539 | 0.0533 | 0.0521 | 0.0494 |

| 75 | 0.0524 | 0.0490 | 0.0474 | 0.0539 | 0.0593 | 0.0587 | 0.0546 | 0.0583 | 0.0579 | 0.0567 | 0.0535 |

| 76 | 0.0572 | 0.0539 | 0.0527 | 0.0590 | 0.0645 | 0.0643 | 0.0597 | 0.0630 | 0.0627 | 0.0616 | 0.0580 |

| 77 | 0.0625 | 0.0595 | 0.0589 | 0.0648 | 0.0701 | 0.0704 | 0.0653 | 0.0682 | 0.0680 | 0.0668 | 0.0630 |

| 78 | 0.0686 | 0.0658 | 0.0660 | 0.0712 | 0.0760 | 0.0769 | 0.0715 | 0.0737 | 0.0736 | 0.0724 | 0.0684 |

| 79 | 0.0753 | 0.0729 | 0.0741 | 0.0783 | 0.0823 | 0.0838 | 0.0783 | 0.0796 | 0.0796 | 0.0784 | 0.0743 |

| 80 | 0.0826 | 0.0806 | 0.0831 | 0.0861 | 0.0889 | 0.0913 | 0.0857 | 0.0859 | 0.0861 | 0.0848 | 0.0809 |

| 81 | 0.0907 | 0.0891 | 0.0930 | 0.0945 | 0.0959 | 0.0991 | 0.0937 | 0.0928 | 0.0931 | 0.0916 | 0.0881 |

| 82 | 0.0995 | 0.0983 | 0.1037 | 0.1035 | 0.1033 | 0.1075 | 0.1024 | 0.1001 | 0.1007 | 0.0989 | 0.0960 |

| 83 | 0.1090 | 0.1082 | 0.1151 | 0.1131 | 0.1109 | 0.1162 | 0.1118 | 0.1082 | 0.1089 | 0.1067 | 0.1048 |

| 84 | 0.1190 | 0.1187 | 0.1271 | 0.1232 | 0.1189 | 0.1254 | 0.1220 | 0.1170 | 0.1179 | 0.1151 | 0.1146 |

| 85 | 0.1297 | 0.1298 | 0.1394 | 0.1335 | 0.1272 | 0.1349 | 0.1329 | 0.1268 | 0.1279 | 0.1243 | 0.1255 |

| 86 | 0.1409 | 0.1414 | 0.1520 | 0.1439 | 0.1358 | 0.1448 | 0.1446 | 0.1378 | 0.1389 | 0.1345 | 0.1377 |

| 87 | 0.1525 | 0.1535 | 0.1645 | 0.1539 | 0.1446 | 0.1550 | 0.1571 | 0.1504 | 0.1512 | 0.1458 | 0.1514 |

| 88 | 0.1646 | 0.1660 | 0.1766 | 0.1631 | 0.1538 | 0.1656 | 0.1704 | 0.1649 | 0.1650 | 0.1586 | 0.1667 |

| 89 | 0.1771 | 0.1790 | 0.1880 | 0.1708 | 0.1632 | 0.1763 | 0.1846 | 0.1820 | 0.1808 | 0.1734 | 0.1839 |

| 90 | 0.1899 | 0.1924 | 0.1985 | 0.1761 | 0.1729 | 0.1874 | 0.1997 | 0.2024 | 0.1990 | 0.1908 | 0.2033 |

| 91 | 0.2030 | 0.2062 | 0.2075 | 0.1774 | 0.1829 | 0.1986 | 0.2157 | 0.2270 | 0.2200 | 0.2115 | 0.2253 |

| 92 | 0.2163 | 0.2203 | 0.2147 | 0.1729 | 0.1931 | 0.2100 | 0.2326 | 0.2570 | 0.2445 | 0.2365 | 0.2500 |

| 93 | 0.2298 | 0.2348 | 0.2194 | 0.1598 | 0.2035 | 0.2217 | 0.2504 | 0.2941 | 0.2733 | 0.2674 | 0.2781 |

| 94 | 0.2435 | 0.2497 | 0.2213 | 0.1342 | 0.2142 | 0.2335 | 0.2692 | 0.3403 | 0.3074 | 0.3059 | 0.3099 |

| 95 | 0.2574 | 0.2650 | 0.2195 | 0.0907 | 0.2252 | 0.2454 | 0.2889 | 0.3985 | 0.3481 | 0.3545 | 0.3460 |

| 96 | 0.2795 | 0.2863 | 0.2450 | 0.1279 | 0.2502 | 0.2685 | 0.3081 | 0.4077 | 0.3619 | 0.3677 | 0.3600 |

| 97 | 0.3015 | 0.3077 | 0.2705 | 0.1651 | 0.2752 | 0.2917 | 0.3273 | 0.4169 | 0.3757 | 0.3810 | 0.3740 |

| 98 | 0.3236 | 0.3291 | 0.2960 | 0.2024 | 0.3002 | 0.3148 | 0.3465 | 0.4262 | 0.3895 | 0.3942 | 0.3880 |

| 99 | 0.3456 | 0.3504 | 0.3215 | 0.2396 | 0.3251 | 0.3380 | 0.3657 | 0.4354 | 0.4033 | 0.4074 | 0.4020 |

| 100 | 0.3677 | 0.3718 | 0.3470 | 0.2768 | 0.3501 | 0.3611 | 0.3849 | 0.4446 | 0.4171 | 0.4206 | 0.4160 |

| 101 | 0.3897 | 0.3932 | 0.3725 | 0.3140 | 0.3751 | 0.3843 | 0.4040 | 0.4539 | 0.4309 | 0.4339 | 0.4300 |

| 102 | 0.4118 | 0.4145 | 0.3980 | 0.3512 | 0.4001 | 0.4074 | 0.4232 | 0.4631 | 0.4447 | 0.4471 | 0.4440 |

| 103 | 0.4338 | 0.4359 | 0.4235 | 0.3884 | 0.4251 | 0.4306 | 0.4424 | 0.4723 | 0.4586 | 0.4603 | 0.4580 |

| 104 | 0.4559 | 0.4573 | 0.4490 | 0.4256 | 0.4500 | 0.4537 | 0.4616 | 0.4815 | 0.4724 | 0.4735 | 0.4720 |

| 105 | 0.4779 | 0.4786 | 0.4745 | 0.4628 | 0.4750 | 0.4769 | 0.4808 | 0.4908 | 0.4862 | 0.4868 | 0.4860 |

| 106 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 |

| 107 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 |

| 108 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 |

| 109 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 |

| 110 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 |

| 111 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 |

| 112 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 |

| 113 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 |

| 114 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 |

| 115 | 1.0000 | 1.0000 | 1.0000 | 1.0000 | 1.0000 | 1.0000 | 1.0000 | 1.0000 | 1.0000 | 1.0000 | 1.0000 |

| Age | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 50 | 0.0072 | 0.0029 | 0.0036 | 0.0062 | 0.0034 | 0.0058 | 0.0059 | 0.0086 | 0.0081 | 0.0057 | 0.0061 |

| 51 | 0.0081 | 0.0054 | 0.0053 | 0.0068 | 0.0045 | 0.0064 | 0.0065 | 0.0088 | 0.0084 | 0.0067 | 0.0069 |

| 52 | 0.0089 | 0.0073 | 0.0069 | 0.0075 | 0.0056 | 0.0070 | 0.0071 | 0.0090 | 0.0088 | 0.0077 | 0.0077 |

| 53 | 0.0096 | 0.0088 | 0.0082 | 0.0082 | 0.0068 | 0.0077 | 0.0077 | 0.0092 | 0.0091 | 0.0085 | 0.0083 |

| 54 | 0.0103 | 0.0100 | 0.0093 | 0.0089 | 0.0080 | 0.0084 | 0.0083 | 0.0095 | 0.0094 | 0.0091 | 0.0089 |

| 55 | 0.0109 | 0.0109 | 0.0103 | 0.0096 | 0.0093 | 0.0091 | 0.0090 | 0.0096 | 0.0097 | 0.0097 | 0.0095 |

| 56 | 0.0114 | 0.0116 | 0.0112 | 0.0103 | 0.0105 | 0.0098 | 0.0098 | 0.0098 | 0.0101 | 0.0103 | 0.0099 |

| 57 | 0.0119 | 0.0122 | 0.0120 | 0.0110 | 0.0117 | 0.0106 | 0.0106 | 0.0101 | 0.0104 | 0.0108 | 0.0104 |

| 58 | 0.0124 | 0.0127 | 0.0127 | 0.0117 | 0.0128 | 0.0113 | 0.0114 | 0.0105 | 0.0109 | 0.0112 | 0.0109 |

| 59 | 0.0129 | 0.0132 | 0.0133 | 0.0124 | 0.0138 | 0.0121 | 0.0122 | 0.0111 | 0.0114 | 0.0117 | 0.0114 |

| 60 | 0.0133 | 0.0136 | 0.0139 | 0.0131 | 0.0148 | 0.0129 | 0.0131 | 0.0119 | 0.0121 | 0.0122 | 0.0119 |

| 61 | 0.0138 | 0.0140 | 0.0145 | 0.0137 | 0.0156 | 0.0137 | 0.0140 | 0.0128 | 0.0128 | 0.0128 | 0.0126 |

| 62 | 0.0143 | 0.0145 | 0.0151 | 0.0144 | 0.0163 | 0.0145 | 0.0151 | 0.0139 | 0.0137 | 0.0134 | 0.0133 |

| 63 | 0.0148 | 0.0150 | 0.0156 | 0.0150 | 0.0170 | 0.0153 | 0.0161 | 0.0151 | 0.0147 | 0.0142 | 0.0142 |

| 64 | 0.0154 | 0.0157 | 0.0162 | 0.0157 | 0.0176 | 0.0162 | 0.0173 | 0.0164 | 0.0159 | 0.0152 | 0.0152 |

| 65 | 0.0161 | 0.0164 | 0.0169 | 0.0164 | 0.0181 | 0.0172 | 0.0185 | 0.0179 | 0.0172 | 0.0163 | 0.0163 |

| 66 | 0.0170 | 0.0172 | 0.0176 | 0.0171 | 0.0187 | 0.0182 | 0.0198 | 0.0194 | 0.0187 | 0.0175 | 0.0176 |

| 67 | 0.0180 | 0.0181 | 0.0185 | 0.0180 | 0.0193 | 0.0192 | 0.0212 | 0.0211 | 0.0203 | 0.0190 | 0.0191 |

| 68 | 0.0192 | 0.0193 | 0.0195 | 0.0190 | 0.0201 | 0.0204 | 0.0227 | 0.0229 | 0.0221 | 0.0207 | 0.0208 |

| 69 | 0.0207 | 0.0206 | 0.0207 | 0.0202 | 0.0210 | 0.0217 | 0.0243 | 0.0248 | 0.0240 | 0.0225 | 0.0226 |

| 70 | 0.0223 | 0.0221 | 0.0222 | 0.0217 | 0.0221 | 0.0231 | 0.0259 | 0.0269 | 0.0262 | 0.0246 | 0.0245 |

| 71 | 0.0243 | 0.0238 | 0.0241 | 0.0235 | 0.0235 | 0.0248 | 0.0278 | 0.0291 | 0.0285 | 0.0269 | 0.0266 |

| 72 | 0.0265 | 0.0258 | 0.0263 | 0.0257 | 0.0252 | 0.0266 | 0.0297 | 0.0315 | 0.0310 | 0.0295 | 0.0288 |

| 73 | 0.0290 | 0.0281 | 0.0289 | 0.0284 | 0.0273 | 0.0287 | 0.0318 | 0.0341 | 0.0338 | 0.0322 | 0.0312 |

| 74 | 0.0318 | 0.0308 | 0.0320 | 0.0315 | 0.0298 | 0.0312 | 0.0341 | 0.0370 | 0.0368 | 0.0353 | 0.0337 |

| 75 | 0.0349 | 0.0338 | 0.0355 | 0.0352 | 0.0327 | 0.0340 | 0.0367 | 0.0402 | 0.0401 | 0.0385 | 0.0364 |

| 76 | 0.0383 | 0.0371 | 0.0395 | 0.0393 | 0.0361 | 0.0372 | 0.0396 | 0.0437 | 0.0437 | 0.0421 | 0.0393 |

| 77 | 0.0420 | 0.0409 | 0.0440 | 0.0440 | 0.0400 | 0.0409 | 0.0428 | 0.0477 | 0.0476 | 0.0460 | 0.0424 |

| 78 | 0.0460 | 0.0451 | 0.0490 | 0.0491 | 0.0443 | 0.0451 | 0.0464 | 0.0522 | 0.0519 | 0.0502 | 0.0458 |

| 79 | 0.0503 | 0.0497 | 0.0544 | 0.0547 | 0.0491 | 0.0499 | 0.0505 | 0.0572 | 0.0566 | 0.0549 | 0.0496 |

| 80 | 0.0548 | 0.0548 | 0.0602 | 0.0608 | 0.0542 | 0.0552 | 0.0550 | 0.0628 | 0.0618 | 0.0600 | 0.0538 |

| 81 | 0.0596 | 0.0604 | 0.0665 | 0.0672 | 0.0598 | 0.0611 | 0.0600 | 0.0690 | 0.0675 | 0.0657 | 0.0586 |

| 82 | 0.0648 | 0.0665 | 0.0730 | 0.0740 | 0.0657 | 0.0676 | 0.0656 | 0.0758 | 0.0738 | 0.0720 | 0.0641 |

| 83 | 0.0702 | 0.0733 | 0.0799 | 0.0811 | 0.0720 | 0.0746 | 0.0718 | 0.0834 | 0.0808 | 0.0792 | 0.0706 |

| 84 | 0.0761 | 0.0807 | 0.0870 | 0.0885 | 0.0786 | 0.0820 | 0.0786 | 0.0917 | 0.0885 | 0.0872 | 0.0782 |

| 85 | 0.0825 | 0.0889 | 0.0944 | 0.0962 | 0.0854 | 0.0900 | 0.0860 | 0.1008 | 0.0972 | 0.0963 | 0.0872 |

| 86 | 0.0896 | 0.0981 | 0.1021 | 0.1041 | 0.0925 | 0.0984 | 0.0942 | 0.1106 | 0.1068 | 0.1066 | 0.0979 |

| 87 | 0.0978 | 0.1082 | 0.1099 | 0.1123 | 0.0999 | 0.1071 | 0.1030 | 0.1213 | 0.1175 | 0.1183 | 0.1108 |

| 88 | 0.1076 | 0.1195 | 0.1179 | 0.1207 | 0.1075 | 0.1162 | 0.1126 | 0.1328 | 0.1294 | 0.1316 | 0.1264 |

| 89 | 0.1198 | 0.1321 | 0.1260 | 0.1293 | 0.1154 | 0.1256 | 0.1230 | 0.1452 | 0.1427 | 0.1467 | 0.1453 |

| 90 | 0.1357 | 0.1460 | 0.1343 | 0.1382 | 0.1236 | 0.1352 | 0.1343 | 0.1585 | 0.1575 | 0.1638 | 0.1683 |

| 91 | 0.1573 | 0.1614 | 0.1426 | 0.1473 | 0.1320 | 0.1450 | 0.1465 | 0.1728 | 0.1740 | 0.1833 | 0.1963 |

| 92 | 0.1878 | 0.1784 | 0.1511 | 0.1567 | 0.1408 | 0.1550 | 0.1597 | 0.1880 | 0.1923 | 0.2055 | 0.2308 |

| 93 | 0.2322 | 0.1972 | 0.1597 | 0.1663 | 0.1499 | 0.1651 | 0.1740 | 0.2042 | 0.2126 | 0.2307 | 0.2731 |

| 94 | 0.2985 | 0.2177 | 0.1684 | 0.1762 | 0.1593 | 0.1753 | 0.1894 | 0.2215 | 0.2352 | 0.2595 | 0.3253 |

| 95 | 0.3990 | 0.2401 | 0.1771 | 0.1865 | 0.1691 | 0.1855 | 0.2060 | 0.2398 | 0.2603 | 0.2922 | 0.3899 |

| 96 | 0.4082 | 0.2637 | 0.2064 | 0.2150 | 0.1992 | 0.2141 | 0.2327 | 0.2635 | 0.2821 | 0.3111 | 0.3999 |

| 97 | 0.4173 | 0.2873 | 0.2358 | 0.2435 | 0.2293 | 0.2427 | 0.2595 | 0.2871 | 0.3039 | 0.3300 | 0.4099 |

| 98 | 0.4265 | 0.3110 | 0.2651 | 0.2720 | 0.2593 | 0.2713 | 0.2862 | 0.3108 | 0.3257 | 0.3489 | 0.4199 |

| 99 | 0.4357 | 0.3346 | 0.2945 | 0.3005 | 0.2894 | 0.2999 | 0.3129 | 0.3344 | 0.3475 | 0.3678 | 0.4299 |

| 100 | 0.4449 | 0.3582 | 0.3239 | 0.3290 | 0.3195 | 0.3285 | 0.3396 | 0.3581 | 0.3693 | 0.3867 | 0.4399 |

| 101 | 0.4541 | 0.3818 | 0.3532 | 0.3575 | 0.3496 | 0.3571 | 0.3664 | 0.3817 | 0.3911 | 0.4056 | 0.4500 |

| 102 | 0.4633 | 0.4055 | 0.3826 | 0.3860 | 0.3797 | 0.3856 | 0.3931 | 0.4054 | 0.4129 | 0.4245 | 0.4600 |

| 103 | 0.4724 | 0.4291 | 0.4119 | 0.4145 | 0.4098 | 0.4142 | 0.4198 | 0.4290 | 0.4346 | 0.4433 | 0.4700 |

| 104 | 0.4816 | 0.4527 | 0.4413 | 0.4430 | 0.4398 | 0.4428 | 0.4465 | 0.4527 | 0.4564 | 0.4622 | 0.4800 |

| 105 | 0.4908 | 0.4764 | 0.4706 | 0.4715 | 0.4699 | 0.4714 | 0.4733 | 0.4763 | 0.4782 | 0.4811 | 0.4900 |

| 106 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 |

| 107 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 |

| 108 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 |

| 109 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 |

| 110 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 |

| 111 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 |

| 112 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 |

| 113 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 |

| 114 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 |

| 115 | 1.0000 | 1.0000 | 1.0000 | 1.0000 | 1.0000 | 1.0000 | 1.0000 | 1.0000 | 1.0000 | 1.0000 | 1.0000 |

| Age | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 50 | 0.0018 | 0.0017 | 0.0015 | 0.0013 | 0.0012 | 0.0011 | 0.0010 | 0.0012 | 0.0014 | 0.0014 | 0.0014 |

| 51 | 0.0025 | 0.0027 | 0.0025 | 0.0024 | 0.0022 | 0.0022 | 0.0018 | 0.0018 | 0.0019 | 0.0020 | 0.0020 |

| 52 | 0.0033 | 0.0037 | 0.0034 | 0.0035 | 0.0033 | 0.0033 | 0.0025 | 0.0025 | 0.0024 | 0.0026 | 0.0027 |

| 53 | 0.0040 | 0.0048 | 0.0043 | 0.0045 | 0.0044 | 0.0044 | 0.0033 | 0.0032 | 0.0029 | 0.0032 | 0.0033 |

| 54 | 0.0048 | 0.0058 | 0.0053 | 0.0056 | 0.0054 | 0.0055 | 0.0040 | 0.0039 | 0.0034 | 0.0038 | 0.0040 |

| 55 | 0.0055 | 0.0068 | 0.0062 | 0.0067 | 0.0065 | 0.0066 | 0.0048 | 0.0045 | 0.0039 | 0.0043 | 0.0047 |

| 56 | 0.0063 | 0.0079 | 0.0071 | 0.0077 | 0.0076 | 0.0077 | 0.0055 | 0.0052 | 0.0044 | 0.0049 | 0.0053 |

| 57 | 0.0070 | 0.0089 | 0.0080 | 0.0088 | 0.0086 | 0.0088 | 0.0062 | 0.0059 | 0.0049 | 0.0055 | 0.0060 |

| 58 | 0.0077 | 0.0099 | 0.0090 | 0.0099 | 0.0097 | 0.0099 | 0.0070 | 0.0065 | 0.0053 | 0.0061 | 0.0067 |

| 59 | 0.0085 | 0.0109 | 0.0099 | 0.0109 | 0.0108 | 0.0110 | 0.0077 | 0.0072 | 0.0058 | 0.0067 | 0.0073 |

| 60 | 0.0092 | 0.0120 | 0.0108 | 0.0120 | 0.0118 | 0.0121 | 0.0085 | 0.0079 | 0.0063 | 0.0073 | 0.0080 |

| 61 | 0.0104 | 0.0131 | 0.0115 | 0.0121 | 0.0121 | 0.0125 | 0.0090 | 0.0085 | 0.0071 | 0.0083 | 0.0088 |